Disability and income protection insurance are designed to safeguard one of the most valuable assets an individual has: the ability to earn income. While many people insure their homes, vehicles, and belongings, income is often overlooked — even though it funds nearly every other financial obligation.

An unexpected illness or injury can temporarily or permanently prevent someone from working. Without a structured protection plan, this loss of income can create financial instability. Disability and income protection insurance address that risk by providing partial income replacement during periods when work is not possible due to medical reasons.

Understanding how disability coverage works, what it includes, and when it may be appropriate is essential for responsible financial planning.

What Is Disability Insurance?

Disability insurance provides income replacement if an individual becomes unable to work due to a qualifying medical condition. Unlike health insurance, which covers medical bills, disability insurance focuses specifically on lost earnings.

If an injury or illness prevents someone from performing their job duties, disability insurance can help replace a portion of their income until recovery or until policy limits are reached.

This type of insurance is structured around defined policy terms and medical evaluations.

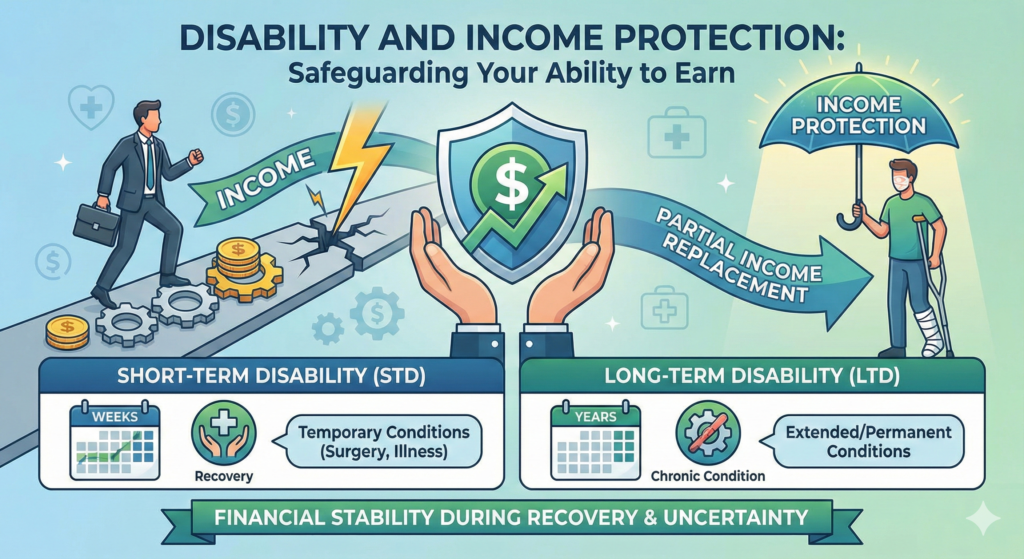

Short-Term vs. Long-Term Disability Insurance

Disability insurance is typically divided into two main categories.

Short-Term Disability Insurance

Short-term disability (STD) insurance provides income replacement for a limited period, often ranging from a few weeks to several months.

It is commonly used for:

- Recovery from surgery

- Temporary medical conditions

- Pregnancy-related leave (depending on policy terms)

Short-term policies generally begin paying benefits after a brief waiting period.

Long-Term Disability Insurance

Long-term disability (LTD) insurance provides benefits for extended periods — sometimes several years or until retirement age.

It is designed for serious or chronic conditions that significantly limit a person’s ability to work.

Long-term policies often have longer waiting periods before benefits begin but offer more extended coverage durations.

How Disability Insurance Benefits Are Calculated

Disability insurance does not typically replace 100% of income. Instead, policies often provide a percentage of pre-disability earnings, commonly ranging between 50% and 70%.

The purpose is to maintain financial stability while preserving incentives to return to work when possible.

Benefit amounts are determined at the time of policy issuance and are subject to maximum limits defined in the policy.

Key Policy Components

Understanding the structure of disability insurance requires familiarity with several important terms.

Elimination Period

The elimination period is the waiting period between the onset of disability and the start of benefit payments. It can range from a few weeks to several months.

Longer elimination periods generally result in lower premiums.

Benefit Period

The benefit period defines how long payments will continue once eligibility is established.

Short-term policies have shorter benefit periods, while long-term policies may extend for years.

Definition of Disability

Policies vary in how they define “disability.” Some policies define disability as the inability to perform one’s specific occupation. Others define it as the inability to perform any occupation for which the insured is reasonably qualified.

Understanding this distinction is essential, as it significantly affects eligibility for benefits.

Employer-Sponsored Disability Insurance

Many employers offer disability insurance as part of employee benefits packages.

Employer-sponsored plans may:

- Cover a percentage of salary

- Be partially or fully employer-paid

- Have standardized coverage limits

While employer plans provide valuable protection, coverage limits may not always fully align with personal financial obligations.

Individuals sometimes supplement employer coverage with private policies.

Individual Disability Insurance Policies

Individual disability insurance policies are purchased directly from insurance providers.

These policies can offer:

- Customizable coverage amounts

- Flexible benefit periods

- Portable coverage (independent of employment status)

Individual policies may be particularly valuable for self-employed individuals or professionals without employer-sponsored benefits.

Income Protection Beyond Disability Insurance

Income protection may also involve additional strategies beyond traditional disability insurance.

Examples include:

- Emergency savings funds

- Supplemental insurance riders

- Business overhead expense insurance (for business owners)

For entrepreneurs and self-employed individuals, protecting income may involve protecting both personal earnings and business continuity.

Who Should Consider Disability and Income Protection?

Disability insurance may be appropriate for individuals who:

- Rely on earned income to meet financial obligations

- Have dependents

- Have limited savings

- Work in physically demanding or specialized professions

- Are self-employed

Because income supports housing, food, healthcare, and long-term savings, its protection can be a critical component of financial resilience.

Factors That Affect Disability Insurance Premiums

Insurance providers evaluate several factors when determining premiums:

- Age

- Occupation

- Health status

- Income level

- Benefit amount selected

- Elimination and benefit periods

Higher-risk occupations may result in higher premiums due to increased likelihood of claims.

Maintaining accurate application information is essential to ensure coverage validity.

Common Exclusions and Limitations

Disability insurance policies may exclude:

- Pre-existing conditions (depending on policy terms)

- Self-inflicted injuries

- Disabilities resulting from criminal activity

Policies may also include partial disability provisions, which provide reduced benefits if an individual can work part-time but not at full capacity.

Careful review of policy language helps prevent misunderstandings during the claims process.

The Claims Process

If a disability occurs, the insured typically must:

- Provide medical documentation

- Submit a formal claim

- Demonstrate inability to work according to policy definition

The insurer reviews medical records and may require ongoing documentation.

Timely and accurate reporting supports smoother claim evaluation.

Disability Insurance in a Changing Workforce

Modern workforce trends — including remote work, freelancing, and entrepreneurship — have increased awareness of income protection needs.

Self-employed individuals may not have access to employer-sponsored benefits, making personal disability insurance more relevant.

As work structures evolve, income protection remains a consistent financial priority.

Disability Insurance as Part of Financial Planning

Disability and income protection insurance complement other financial planning tools such as:

- Health insurance

- Life insurance

- Retirement savings

- Emergency funds

While no single policy eliminates all financial risk, disability insurance addresses a specific and potentially disruptive exposure: the inability to earn income.

Financial stability often depends not only on asset protection, but also on income continuity.

Conclusion

Disability and income protection insurance provide structured financial support when illness or injury prevents someone from working. By replacing a portion of lost income, these policies help individuals maintain financial stability during challenging periods.

Understanding elimination periods, benefit durations, policy definitions, and coverage limits allows for informed decision-making. Whether obtained through an employer or purchased individually, disability insurance can play an important role in long-term financial planning.

Income is often a person’s most consistent financial resource. Protecting it ensures that temporary setbacks do not become long-term financial crises.