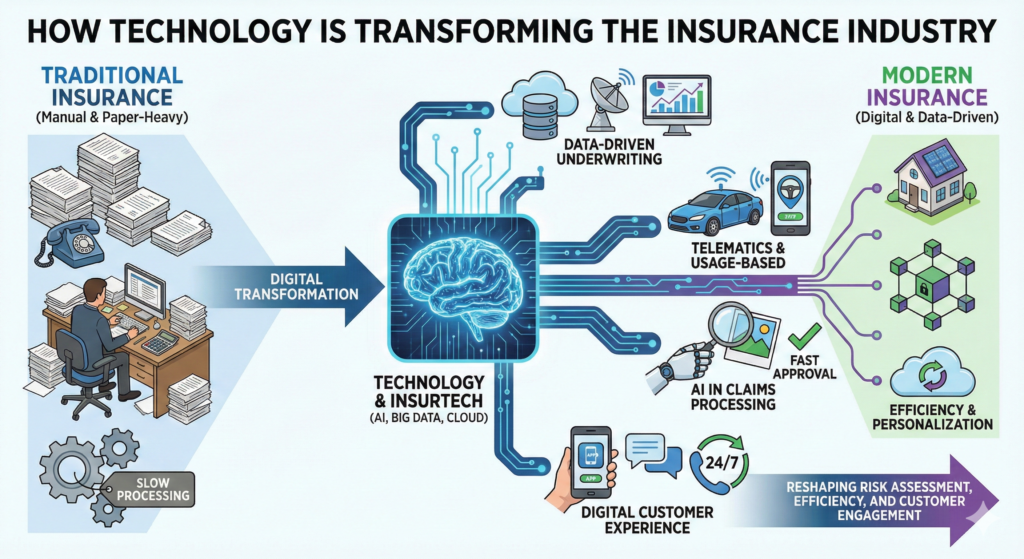

The insurance industry has traditionally been perceived as conservative, paperwork-heavy, and slow to adapt. For decades, processes relied on manual underwriting, in-person agents, and lengthy claims procedures. Today, that perception is changing rapidly.

Technology is fundamentally transforming how insurance is priced, sold, managed, and delivered. From artificial intelligence and big data analytics to telematics and cybersecurity solutions, digital innovation is reshaping risk assessment and customer experience.

Understanding how technology is transforming the insurance industry reveals not only operational changes but also strategic shifts in how risk is evaluated and managed.

The Rise of Insurtech

One of the most visible developments in the insurance sector is the rise of insurtech — technology-driven companies focused on improving insurance processes.

Insurtech startups and established insurers alike are leveraging:

- Artificial intelligence (AI)

- Machine learning

- Cloud computing

- Blockchain

- Mobile applications

These tools aim to streamline underwriting, enhance customer engagement, and increase efficiency.

While traditional insurers once relied heavily on legacy systems, many are now investing in digital transformation to remain competitive.

Data-Driven Underwriting

Underwriting — the process of evaluating risk — has evolved significantly with technological advancement.

Historically, underwriting relied on limited data points such as age, location, claims history, and general industry classifications.

Today, insurers can analyze vast datasets, including:

- Driving behavior through telematics

- Real-time health data (where permitted)

- Cybersecurity posture assessments

- Property condition data via remote sensing

Advanced analytics allows insurers to price policies more precisely based on actual risk behavior rather than broad demographic categories.

This shift toward data-driven underwriting improves risk segmentation and pricing accuracy.

Telematics and Usage-Based Insurance

In auto insurance, telematics devices and mobile applications track driving behavior.

Metrics such as:

- Speed patterns

- Braking habits

- Acceleration

- Time of travel

are used to assess individual risk profiles.

Usage-based insurance models allow premiums to reflect driving behavior rather than relying solely on traditional rating factors.

For responsible drivers, this can create more personalized pricing structures.

Telematics demonstrates how technology connects real-world behavior to insurance pricing.

Artificial Intelligence in Claims Processing

Claims management is another area undergoing transformation.

Artificial intelligence and automation tools can:

- Analyze claim documentation

- Detect potential fraud indicators

- Assess damage through image recognition

- Accelerate approval workflows

For example, property claims may be evaluated using photo submissions analyzed by AI-powered systems.

Automation reduces processing time and improves operational efficiency.

However, human oversight remains essential, particularly in complex or disputed claims.

Digital Customer Experience

Consumers increasingly expect seamless digital interactions.

Insurance providers now offer:

- Online quoting tools

- Mobile policy management apps

- Digital document storage

- Real-time chat support

Customers can compare coverage, adjust limits, and file claims through digital platforms.

This shift enhances accessibility and transparency, particularly for younger, tech-savvy consumers.

Technology reduces friction in policy management.

Cyber Insurance and Emerging Risks

As businesses digitize operations, new risk categories emerge.

Cyber threats, data breaches, and ransomware incidents have become major concerns.

Technology has both created new risks and enabled new insurance products.

Cyber insurance policies now often require:

- Security audits

- Multi-factor authentication protocols

- Data protection standards

Insurers assess cybersecurity infrastructure before issuing coverage.

The intersection of technology and insurance is now bidirectional — technology introduces risks while also providing mitigation tools.

Blockchain and Smart Contracts

Blockchain technology is being explored for its potential to increase transparency and reduce fraud.

Smart contracts — self-executing agreements triggered by predefined conditions — may streamline claims payments.

For example, parametric insurance products can automatically trigger payouts when specific criteria are met, such as weather data thresholds.

While still evolving, blockchain applications may enhance trust and operational efficiency.

Predictive Analytics and Risk Prevention

Technology allows insurers to move beyond reactive models.

Predictive analytics can identify patterns that indicate higher risk exposure.

For example:

- Sensors in commercial buildings can detect water leaks early.

- IoT devices can monitor equipment performance.

- Health tracking devices may encourage preventive care behaviors.

Rather than simply paying claims after losses occur, insurers are increasingly focused on loss prevention.

This proactive model represents a strategic shift in the industry.

Automation and Cost Efficiency

Automation reduces administrative burdens.

Digital document processing, electronic signatures, and cloud-based platforms eliminate manual paperwork.

Operational efficiency may reduce processing delays and improve consistency.

For insurers, automation can lower overhead costs. For policyholders, it can improve service speed.

However, maintaining data security and privacy remains critical.

Regulatory and Ethical Considerations

As insurers collect more data, regulatory and ethical considerations become increasingly important.

Questions arise around:

- Data privacy

- Algorithmic transparency

- Fair pricing models

- Consumer protection

Regulators monitor how data is used in underwriting and pricing decisions.

Balancing innovation with compliance is a central challenge for the modern insurance industry.

The Shift Toward Personalization

Technology enables more personalized insurance solutions.

Rather than offering uniform products, insurers can tailor policies based on behavior, industry, and specific risk exposure.

Personalization may include:

- Adjustable coverage options

- Real-time policy modifications

- Risk-based discounts

While personalization increases flexibility, it also requires careful oversight to ensure fairness and clarity.

The Future of Insurance and Technology

The transformation of insurance is ongoing.

Future developments may include:

- Greater integration of artificial intelligence

- Enhanced real-time risk monitoring

- Expanded use of automation in claims

- Increased digital transparency

As risk environments evolve — particularly in technology-driven sectors — insurance products must adapt accordingly.

Innovation will likely continue to redefine underwriting, distribution, and claims management.

Technology Does Not Eliminate Risk

Despite technological advancement, insurance remains fundamentally about managing uncertainty.

Technology enhances risk assessment and operational efficiency, but it does not eliminate the need for structured protection.

Unexpected events, liability exposure, and operational disruptions will continue to require financial safeguards.

Digital transformation improves the system — it does not replace the core purpose of insurance.

Conclusion

Technology is transforming the insurance industry by reshaping underwriting, claims processing, customer engagement, and product development. From artificial intelligence and telematics to blockchain and predictive analytics, innovation is driving efficiency and personalization.

At the same time, regulatory oversight and ethical considerations remain essential to ensure transparency and fairness.

As digital tools evolve, insurance is becoming more data-driven, responsive, and integrated with real-world behavior.

The future of insurance will likely be defined by its ability to combine technological innovation with structured risk management — creating systems that are both efficient and resilient.