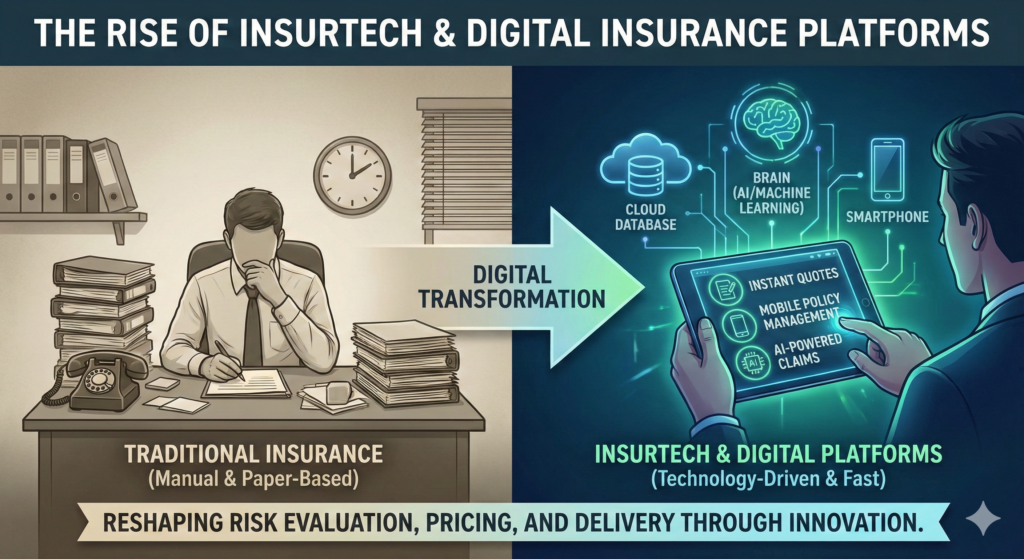

For decades, the insurance industry was defined by paperwork, in-person meetings, and lengthy approval processes. Buying a policy often required phone calls, physical signatures, and extended waiting periods. Today, that landscape is changing rapidly.

The rise of insurtech and digital insurance platforms is reshaping how insurance products are designed, distributed, and managed. Technology-driven companies are introducing faster underwriting, mobile-first experiences, and data-powered pricing models that are transforming traditional insurance structures.

This shift is not simply about convenience — it reflects a broader evolution in how risk is evaluated, priced, and delivered to consumers and businesses.

What Is Insurtech?

Insurtech — short for “insurance technology” — refers to companies and platforms that use digital tools to improve insurance processes.

These improvements may involve:

- Automated underwriting

- Artificial intelligence for claims analysis

- Real-time risk monitoring

- Digital policy management

- Embedded insurance within digital ecosystems

Insurtech firms range from startups focused exclusively on technology-driven policies to traditional insurers modernizing their infrastructure.

The goal is typically the same: reduce friction, increase efficiency, and enhance personalization.

Why Insurtech Is Growing

Several factors have accelerated the rise of insurtech:

1. Changing Consumer Expectations

Modern consumers expect:

- Instant quotes

- Transparent pricing

- Mobile access

- Digital documentation

- Simplified user experiences

Traditional insurance models often struggled to meet these expectations.

Digital platforms are designed with user experience at the forefront, aligning insurance services with broader digital trends.

2. Data Availability

The availability of large datasets has transformed underwriting.

Data sources may include:

- Telematics for driving behavior

- Smart home sensors

- Business cybersecurity metrics

- Public risk databases

Advanced analytics allows insurers to evaluate risk more precisely than traditional models.

3. Technological Infrastructure

Cloud computing, machine learning, and API integrations enable scalable and flexible insurance systems.

Digital platforms can process applications, update policies, and manage claims more efficiently than legacy systems.

Digital Insurance Platforms Explained

Digital insurance platforms allow consumers and businesses to:

- Obtain quotes online

- Customize coverage

- Adjust limits and deductibles

- File claims digitally

- Access policy documents instantly

These platforms may operate independently or in partnership with established insurers.

Some focus exclusively on personal lines such as auto or renters insurance. Others specialize in commercial or niche markets.

The core feature is end-to-end digital interaction.

Embedded Insurance

One of the most significant developments within insurtech is embedded insurance.

Embedded insurance integrates coverage directly into another product or service.

Examples include:

- Travel insurance offered during flight booking

- Device protection included in electronics purchases

- Rental coverage added during car reservations

This model reduces friction by integrating insurance at the point of need.

Embedded insurance demonstrates how digital ecosystems are reshaping distribution channels.

AI and Automated Underwriting

Artificial intelligence has significantly influenced underwriting processes.

AI-powered systems can:

- Analyze application data instantly

- Identify risk indicators

- Cross-reference external datasets

- Flag inconsistencies

Automated underwriting reduces processing time and may increase pricing precision.

However, human oversight remains essential, particularly for complex or high-value policies.

Digital Claims Processing

Claims management is another area where insurtech innovation is visible.

Digital claims systems may include:

- Mobile photo submissions

- AI-based damage estimation

- Automated payout workflows

- Real-time claim tracking

These advancements aim to reduce delays and improve transparency.

While automation increases efficiency, complex claims still require professional evaluation.

The Role of Blockchain

Blockchain technology is being explored to enhance transparency and reduce fraud.

Smart contracts may automate payouts when predefined conditions are met.

For example, parametric insurance products may trigger automatic payments based on verified weather data.

Although still developing, blockchain applications may streamline certain insurance processes.

Cybersecurity and Digital Risk

As insurance becomes more digital, cybersecurity risk becomes more relevant.

Digital insurance platforms must protect:

- Personal data

- Financial information

- Claims documentation

- Behavioral analytics

Regulatory compliance and data privacy standards are critical components of digital transformation.

Technology enhances efficiency but also introduces new risk categories.

Advantages of Insurtech Platforms

Digital insurance platforms offer several advantages:

Speed

Online quoting and automated underwriting reduce waiting times.

Accessibility

Consumers can manage policies from mobile devices.

Transparency

Digital dashboards provide clearer visibility into coverage details.

Customization

Policies can often be adjusted in real time.

These features align insurance with modern digital habits.

Challenges and Considerations

Despite rapid growth, insurtech faces challenges.

Regulatory Compliance

Insurance remains a highly regulated industry. Digital innovation must comply with state and federal requirements.

Data Ethics

Algorithmic pricing raises questions about fairness and transparency.

Human Interaction

Some consumers still prefer personal guidance, particularly for complex coverage needs.

Digital transformation must balance efficiency with clarity and trust.

The Impact on Traditional Insurers

Traditional insurers are not being replaced — they are evolving.

Many established carriers are:

- Investing in digital infrastructure

- Partnering with insurtech startups

- Launching mobile-first products

- Integrating AI-driven underwriting tools

The distinction between insurtech and traditional insurance is increasingly blurred.

Digital transformation is becoming industry-wide.

Insurtech in Commercial Insurance

While personal insurance often receives attention, insurtech is also expanding in commercial lines.

Digital platforms now support:

- Small business insurance

- Professional liability coverage

- Cyber insurance policies

- On-demand coverage for freelancers

Technology enables flexible policy structures suited to modern business models.

This is particularly relevant for startups and tech-driven enterprises.

The Future of Digital Insurance

The rise of insurtech is unlikely to slow.

Future developments may include:

- Greater personalization through predictive analytics

- Real-time risk monitoring via IoT devices

- Increased automation in claims adjudication

- Integration with financial planning tools

As risk environments evolve — particularly in digital industries — insurance platforms must adapt accordingly.

The industry’s transformation reflects broader technological change across sectors.

Conclusion

The rise of insurtech and digital insurance platforms marks a significant evolution in how insurance is delivered and managed. By leveraging artificial intelligence, big data, automation, and digital interfaces, insurers are creating faster, more accessible, and more personalized experiences.

At the same time, regulatory oversight, data privacy, and ethical considerations remain essential to maintain trust and transparency.

Technology is not replacing insurance — it is redefining how protection is structured and delivered in a digital world.

Understanding this transformation allows individuals and businesses to navigate insurance decisions with greater clarity and awareness.