The insurance industry has always depended on data. At its core, insurance is built on probability, statistics, and risk modeling. However, the scale and sophistication of data usage today are transforming the industry in unprecedented ways.

Modern insurance now relies heavily on data analytics, artificial intelligence (AI), and automation to enhance underwriting accuracy, improve claims efficiency, reduce fraud, and deliver more personalized customer experiences.

These technologies are not replacing insurance fundamentals. Instead, they are amplifying the industry’s ability to measure, predict, and manage risk in a more dynamic and precise manner.

The Expanding Role of Data in Insurance

Historically, insurers relied on relatively limited datasets, such as:

- Age

- Geographic location

- Claims history

- Industry classification

- Property characteristics

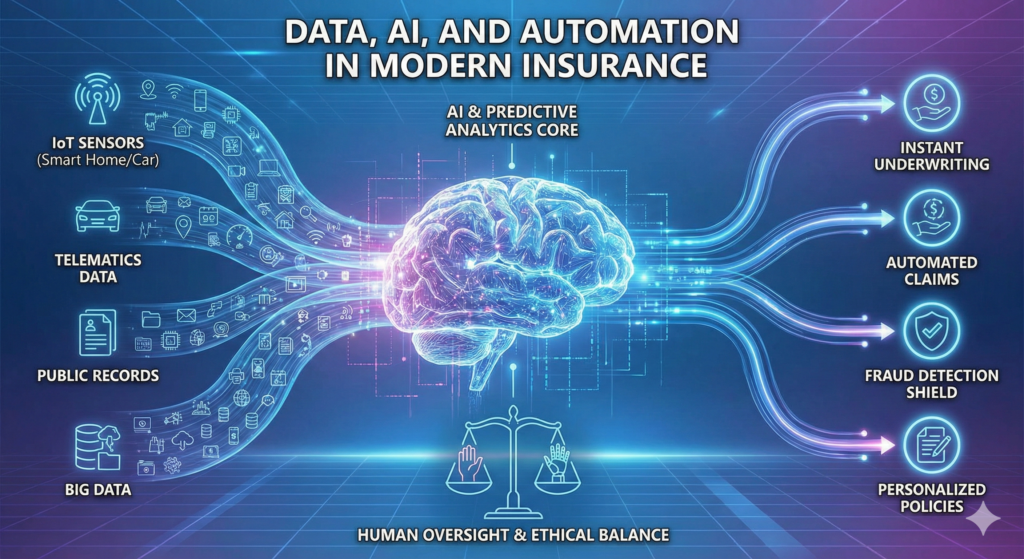

While these variables remain relevant, modern insurers now analyze vastly larger and more complex data sources.

Examples include:

- Driving behavior through telematics

- Smart home sensor data

- Cybersecurity posture assessments

- Public records and environmental risk databases

- Business operational metrics

The growth of big data has allowed insurers to refine pricing models and better segment risk categories.

More granular data leads to more precise risk evaluation.

Artificial Intelligence in Underwriting

Underwriting is one of the most significant areas influenced by AI.

Artificial intelligence systems can:

- Analyze large datasets in real time

- Identify patterns and correlations

- Flag anomalies or inconsistencies

- Predict potential loss frequency

AI-powered underwriting models help insurers evaluate applications faster and with greater consistency.

For example, rather than relying solely on broad demographic indicators, machine learning algorithms may incorporate behavioral data and risk trends to create more individualized pricing structures.

However, human oversight remains essential to ensure fairness, transparency, and regulatory compliance.

Predictive Analytics and Risk Modeling

Predictive analytics uses historical data and statistical modeling to forecast potential future events.

In modern insurance, predictive models may estimate:

- The likelihood of claims

- The severity of potential losses

- Fraud risk indicators

- Catastrophic event exposure

By forecasting potential risk patterns, insurers can allocate reserves more effectively and price policies more accurately.

Predictive analytics also enables insurers to identify emerging risk trends, such as evolving cyber threats or climate-related exposures.

Automation in Claims Processing

Claims management has traditionally been time-intensive and documentation-heavy.

Automation tools now streamline this process.

Examples include:

- Automated claims intake systems

- Optical character recognition (OCR) for document processing

- AI-based image analysis for property damage

- Automated workflow routing

These systems reduce processing delays and improve operational efficiency.

For simple claims, automation may enable near real-time decisions.

For complex claims, automation assists adjusters by organizing data and identifying relevant information.

Automation enhances speed while preserving human review for nuanced cases.

Fraud Detection and Risk Prevention

Insurance fraud presents financial challenges for both insurers and policyholders.

AI-powered systems analyze patterns across millions of transactions to detect potential fraud indicators.

Machine learning models can identify:

- Unusual claim timing

- Repeated patterns across accounts

- Inconsistent documentation

- Behavioral anomalies

Early detection improves claims integrity and reduces unnecessary costs.

Technology also supports preventive risk management, such as monitoring property sensors to detect water leaks before significant damage occurs.

Personalization Through Data Analytics

Modern consumers increasingly expect personalized experiences.

Data analytics enables insurers to tailor policies based on individual risk characteristics.

For example:

- Safe driving behavior may influence auto insurance pricing.

- Smart home devices may support property risk mitigation.

- Businesses with strong cybersecurity protocols may qualify for specific coverage terms.

Personalization enhances fairness by aligning premiums more closely with individual behavior rather than generalized categories.

However, transparency in pricing models remains essential.

Real-Time Risk Monitoring

Internet of Things (IoT) devices allow real-time monitoring of certain risks.

Examples include:

- Commercial building sensors detecting temperature fluctuations

- Fleet management systems monitoring driver behavior

- Health monitoring devices supporting wellness initiatives

Real-time data can support early intervention, potentially reducing the severity of losses.

This represents a shift from reactive claims payment to proactive risk management.

Insurance increasingly involves preventing losses, not just compensating for them.

Automation and Operational Efficiency

Automation extends beyond underwriting and claims.

Insurers now use automation for:

- Policy issuance

- Document generation

- Customer service chatbots

- Payment processing

- Renewal notifications

Reducing administrative workload improves efficiency and scalability.

Digital workflows eliminate paper-based processes and manual data entry.

Operational efficiency may reduce costs and improve consistency.

Ethical and Regulatory Considerations

As insurers rely more heavily on data and AI, ethical and regulatory considerations become increasingly important.

Key concerns include:

- Data privacy

- Algorithmic bias

- Transparency in decision-making

- Consumer protection

Regulators closely monitor how data is used in underwriting and pricing.

Insurers must ensure compliance with federal and state laws governing data protection and fair practices.

Balancing innovation with responsibility is central to sustainable technological advancement.

The Human Role in an Automated Industry

Despite increasing automation, human expertise remains essential.

Insurance decisions often involve:

- Complex liability analysis

- Disputed claims

- Legal interpretation

- Client advisory services

AI and automation enhance efficiency, but they do not replace professional judgment.

Human oversight ensures context, fairness, and ethical consideration.

The most effective insurance models combine technological tools with experienced professionals.

Impact on Businesses and Consumers

For businesses, data-driven insurance models may offer:

- More accurate pricing

- Faster claims processing

- Tailored coverage options

- Enhanced risk prevention strategies

For consumers, digital systems may provide:

- Simplified applications

- Instant policy access

- Real-time claim tracking

- Greater transparency

The integration of data, AI, and automation enhances accessibility and responsiveness.

Future Trends in Modern Insurance Technology

Looking ahead, technological integration may expand to include:

- Advanced predictive modeling using AI

- Greater integration of IoT devices

- Enhanced fraud detection algorithms

- Increased automation of policy adjustments

- Broader use of blockchain for secure data exchange

Insurance technology continues to evolve alongside broader digital transformation across industries.

The emphasis will likely remain on precision, transparency, and operational efficiency.

Conclusion

Data, artificial intelligence, and automation are reshaping modern insurance by enhancing underwriting precision, improving claims efficiency, strengthening fraud detection, and enabling personalized coverage structures.

These technologies do not change the fundamental purpose of insurance — managing financial risk — but they significantly improve how that purpose is executed.

As digital innovation advances, insurers must balance efficiency with ethical responsibility, ensuring transparency and compliance while embracing technological progress.

Modern insurance is increasingly defined by its ability to combine structured risk management with intelligent, data-driven systems.