Insurance policies are designed to provide financial protection against specific risks. However, every policy also includes exclusions — situations, events, or conditions that are not covered.

For many policyholders, exclusions are one of the least understood aspects of insurance. Yet they are just as important as coverage itself. Misunderstanding exclusions can lead to unexpected out-of-pocket costs and denied claims.

This guide explains insurance policy exclusions in detail, how they work, and why they are a critical part of every insurance contract in the United States.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

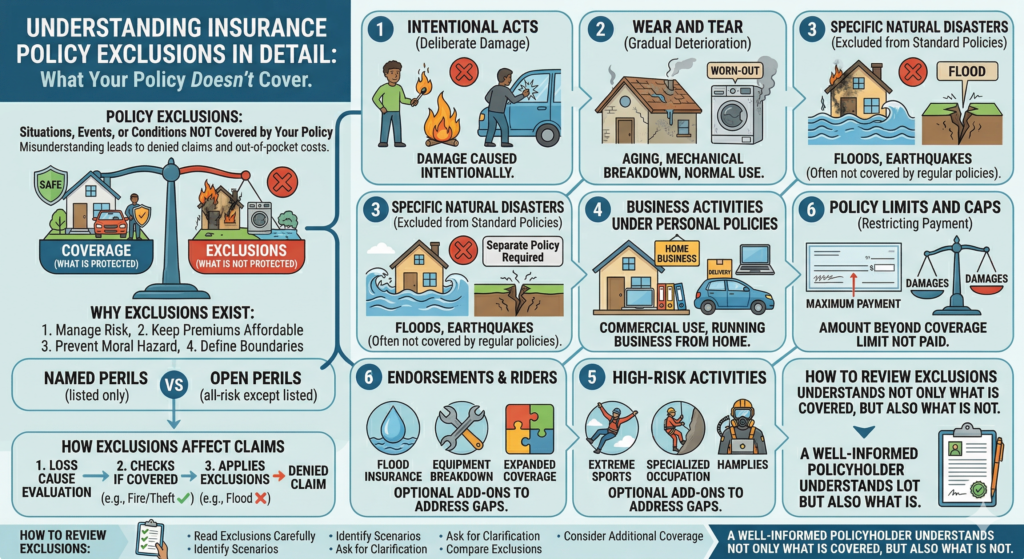

What Are Insurance Policy Exclusions?

An exclusion is a specific condition or type of loss that an insurance policy does not cover.

In simple terms:

- Coverage defines what is protected

- Exclusions define what is not protected

Every insurance policy includes exclusions to clearly outline the limits of protection.

These exclusions are not hidden — they are written into the policy contract. However, they are often overlooked because policy documents can be complex.

Why Do Insurance Policies Include Exclusions?

Exclusions exist for several important reasons.

1. To Manage Risk

Insurance companies cannot cover every possible risk. Some risks are too unpredictable, too frequent, or too costly to insure under standard policies.

Excluding certain events allows insurers to maintain financial stability.

2. To Keep Premiums Affordable

If policies covered every possible scenario, premiums would be significantly higher.

By limiting coverage through exclusions, insurers can offer more affordable pricing for standard risks.

3. To Prevent Moral Hazard

Moral hazard refers to situations where individuals take greater risks because they are insured.

Exclusions help reduce this by removing coverage for intentional or preventable actions.

4. To Define Clear Boundaries

Exclusions create clarity.

They establish what the policy is designed to cover — and what falls outside its scope.

This reduces ambiguity during claims evaluation.

Common Types of Insurance Exclusions

Exclusions vary depending on the type of insurance, but several categories appear frequently across policies.

1. Intentional Acts

Most policies exclude damage or loss caused intentionally by the policyholder.

For example:

- Deliberate property damage

- Fraudulent claims

- Intentional injury

Insurance is designed to cover unexpected events — not deliberate actions.

2. Wear and Tear

Insurance typically does not cover gradual deterioration.

Examples include:

- Aging roofs

- Worn-out appliances

- Normal mechanical breakdown

Maintenance and upkeep are considered the responsibility of the policyholder.

3. Specific Natural Disasters

Some natural disasters are excluded from standard policies.

For example:

- Flood damage is usually excluded from standard homeowners insurance

- Earthquake coverage often requires a separate policy or endorsement

These risks may require specialized coverage.

4. Business Activities Under Personal Policies

Personal insurance policies often exclude business-related risks.

Examples:

- Running a business from home

- Using a personal vehicle for commercial purposes

Separate business insurance may be required to cover these exposures.

5. High-Risk Activities

Certain high-risk activities may be excluded or limited.

Examples may include:

- Extreme sports

- Hazardous occupations

- Specialized operations

Coverage for these risks may require additional endorsements or specialized policies.

6. Policy Limits and Caps

While not always labeled as exclusions, coverage limits effectively restrict how much the insurer will pay.

If damages exceed the limit, the remaining amount is not covered.

Understanding limits is essential when evaluating overall protection.

Named Perils vs Open Perils Policies

How exclusions work can depend on the type of policy structure.

Named Perils Policies

These policies cover only the risks specifically listed.

Anything not listed is effectively excluded.

Open Perils (All-Risk) Policies

These policies cover all risks except those specifically excluded.

This structure provides broader protection but still includes defined exclusions.

Understanding which type of policy you have is critical.

How Exclusions Affect Claims

Exclusions play a central role in claims decisions.

When a claim is filed, insurers evaluate:

- What caused the loss

- Whether the cause is covered

- Whether any exclusions apply

If the cause of loss falls under an exclusion, the claim may be denied.

This is why understanding exclusions before a claim occurs is essential.

Real-World Example

Consider a homeowner with standard property insurance.

If damage occurs due to:

- Fire → typically covered

- Theft → typically covered

- Flood → often excluded

Even though the homeowner has insurance, certain types of damage may not be covered without additional policies.

Endorsements and Riders: Expanding Coverage

In many cases, exclusions can be addressed through endorsements (also called riders).

These are optional additions to a policy that modify coverage.

Examples:

- Flood insurance endorsements

- Earthquake coverage add-ons

- Equipment breakdown coverage

Endorsements allow policyholders to tailor coverage based on specific needs.

Common Mistakes Related to Exclusions

Mistake 1: Not Reading the Policy

Many policyholders focus only on premiums and coverage limits.

Ignoring exclusions can lead to misunderstandings.

Mistake 2: Assuming “Full Coverage” Exists

There is no universal policy that covers everything.

Every policy includes limitations and exclusions.

Mistake 3: Not Updating Coverage

As life or business circumstances change, exclusions that once seemed irrelevant may become important.

Regular reviews help ensure coverage remains appropriate.

How to Review Exclusions Effectively

When evaluating an insurance policy:

- Read the exclusions section carefully

- Identify scenarios that may apply to your situation

- Ask for clarification if terms are unclear

- Consider whether additional coverage is needed

- Compare exclusions across different insurers

Understanding exclusions is as important as understanding what is covered.

The Role of Regulation

Insurance policies in the United States are regulated at the state level.

Regulators require insurers to:

- Clearly disclose exclusions

- Use standardized language in some cases

- Follow consumer protection guidelines

However, responsibility still lies with the policyholder to review the policy.

Why Exclusions Matter More Than You Think

Many insurance decisions focus on:

- Premium cost

- Coverage limits

But exclusions often determine whether a claim is approved or denied.

In real-world scenarios, exclusions can have a greater financial impact than small differences in premium.

Understanding them provides a more complete view of your protection.

Final Thoughts

Insurance policy exclusions are not a minor detail — they are a fundamental part of how insurance works.

They define the boundaries of coverage, help manage risk, and influence how claims are evaluated.

For individuals and business owners alike, reviewing exclusions carefully is essential to avoiding unexpected gaps in protection.

A well-informed policyholder understands not only what is covered, but also what is not.

That knowledge is key to making better insurance decisions.