Insurance policies are often filled with technical language, detailed clauses, and complex structures that can feel overwhelming. As a result, many policyholders rely on summaries or assumptions rather than fully understanding what their coverage actually includes.

However, learning how to read an insurance policy properly is one of the most important steps in making informed decisions. It helps you understand what is covered, what is excluded, and how your protection works in real-world situations.

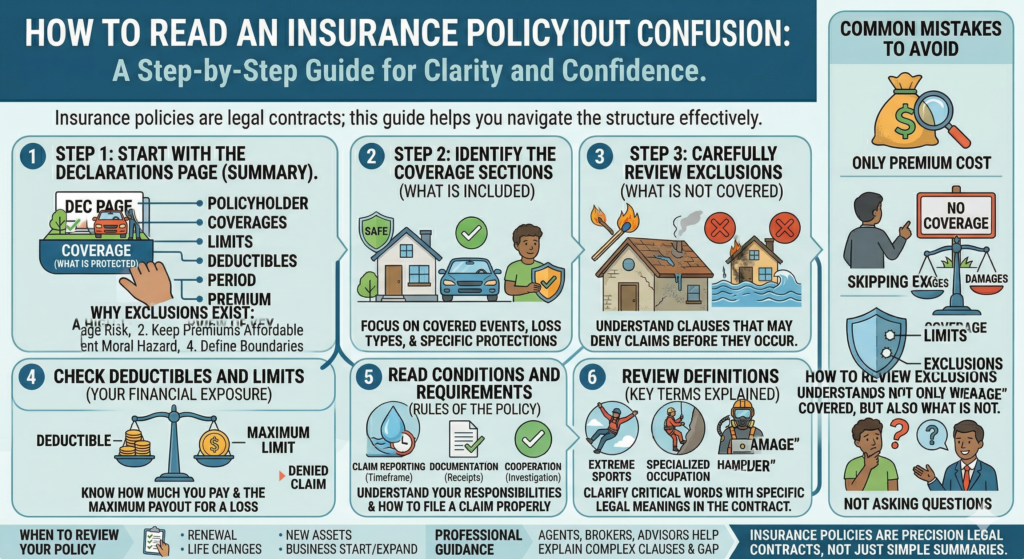

This guide breaks down the process step by step, so you can read an insurance policy with clarity and confidence.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

Why Insurance Policies Seem Confusing

Insurance policies are legal contracts. They are written to be precise, not necessarily simple.

Several factors contribute to their complexity:

- Technical terminology

- Legal definitions

- Detailed conditions and limitations

- Multiple sections with cross-references

While this structure ensures clarity from a legal perspective, it can make policies difficult to understand at first glance.

The goal is not to memorize everything — but to understand how to navigate the document effectively.

The Basic Structure of an Insurance Policy

Most insurance policies follow a similar structure. Understanding this structure makes the document much easier to read.

1. Declarations Page (Overview)

The declarations page — often called the “dec page” — provides a summary of the policy.

It typically includes:

- Policyholder name

- Coverage types

- Coverage limits

- Deductibles

- Policy period

- Premium amount

This section is a high-level overview, not the full contract.

2. Insuring Agreement (What Is Covered)

The insuring agreement explains what the insurance company agrees to cover.

It outlines:

- Types of risks included

- Scope of coverage

- Conditions under which claims may be paid

This is where you understand the core purpose of the policy.

3. Exclusions (What Is Not Covered)

The exclusions section defines what the policy does not cover.

This is one of the most important sections.

Common exclusions may include:

- Intentional damage

- Wear and tear

- Certain natural disasters

- Business activities under personal policies

Many claim denials occur because of exclusions — not because coverage doesn’t exist at all.

4. Conditions (Rules of the Policy)

Conditions explain the responsibilities of both the insurer and the policyholder.

They may include:

- How to file a claim

- Required documentation

- Payment obligations

- Time limits for reporting losses

Failing to meet policy conditions can affect claim outcomes.

5. Definitions (Key Terms Explained)

Insurance policies define specific terms in a dedicated section.

These definitions are critical because:

- Words may have meanings different from everyday use

- Coverage depends on how terms are defined in the policy

For example, the definition of “property damage” or “occurrence” can affect how coverage applies.

Step-by-Step: How to Read Your Policy Effectively

Instead of reading from beginning to end without direction, use a structured approach.

Step 1: Start with the Declarations Page

This gives you a snapshot of:

- What you are paying for

- How much coverage you have

- Key financial details

It helps frame the rest of the document.

Step 2: Identify the Coverage Sections

Focus on what the policy actually covers.

Look for:

- Covered events

- Types of losses

- Specific protections included

This helps you understand the intended purpose of the policy.

Step 3: Carefully Review Exclusions

This step is critical.

Ask yourself:

- What situations are not covered?

- Do any exclusions apply to my real-life risks?

Understanding exclusions prevents surprises during claims.

Step 4: Check Deductibles and Limits

Look at:

- How much you must pay before coverage applies

- Maximum payout limits

These numbers define your financial exposure.

Step 5: Read Conditions and Requirements

Policies often require specific actions.

Examples:

- Reporting claims within a certain timeframe

- Providing documentation

- Cooperating with investigations

Understanding these requirements helps avoid complications later.

Step 6: Review Definitions

If something is unclear, check the definitions section.

Small wording differences can significantly impact coverage interpretation.

Common Mistakes When Reading Insurance Policies

Mistake 1: Only Looking at the Premium

Focusing only on cost ignores how the policy actually works.

Mistake 2: Skipping the Exclusions Section

This is one of the most important parts of the policy.

Mistake 3: Assuming “Full Coverage” Exists

No insurance policy covers everything. Every policy has limits and exclusions.

Mistake 4: Not Asking Questions

If something is unclear, clarification is essential.

Policies are complex by nature, and questions are part of the process.

Real-World Example

Imagine reviewing a homeowners insurance policy.

You see coverage for:

- Fire damage

- Theft

- Vandalism

However, in the exclusions section, you find:

- Flood damage is excluded

Without reviewing exclusions, you might assume flood damage is covered — which could lead to unexpected financial risk.

Why Small Details Matter

In insurance, small details can have significant consequences.

Examples include:

- Definitions that limit coverage scope

- Exclusions that apply to specific scenarios

- Conditions that affect claim eligibility

Careful reading helps identify these details before they become issues.

When to Review Your Policy

Insurance policies should not be reviewed only once.

It is helpful to revisit your policy:

- When renewing coverage

- After major life changes

- When purchasing new assets

- When starting or expanding a business

Regular review ensures your coverage remains aligned with your needs.

The Role of Professional Guidance

While it is important to understand your policy, some situations may benefit from professional input.

Insurance agents, brokers, or advisors can help explain:

- Complex clauses

- Coverage gaps

- Policy comparisons

However, the final responsibility for understanding the policy remains with the policyholder.

Final Thoughts

Reading an insurance policy does not have to be overwhelming.

By understanding the structure and focusing on key sections — coverage, exclusions, limits, and conditions — you can gain a clear picture of how your protection works.

Insurance is not just about having a policy. It is about understanding what that policy actually does.

A well-informed approach helps reduce confusion, avoid unexpected gaps, and support better financial decisions.