When people think about insurance, the focus is often on reducing premiums and saving money. While cost management is important, there is another side of the equation that is frequently overlooked: the cost of being underinsured.

Being underinsured does not mean having no insurance at all. It means having coverage that is insufficient to fully protect against potential financial loss.

In many real-world situations, the financial consequences of underinsurance can be far more significant than the cost of higher premiums.

This guide explains the hidden costs of being underinsured, why it happens, and how to evaluate coverage more effectively.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

What Does It Mean to Be Underinsured?

Underinsurance occurs when the coverage limits, structure, or scope of an insurance policy are not enough to fully cover a loss.

This can happen in several ways:

- Coverage limits are too low

- Key risks are excluded

- Deductibles are too high relative to available funds

- Certain assets or activities are not included in the policy

In these cases, the insurance policy exists — but it may not provide adequate financial protection when it is needed most.

Why Underinsurance Happens

Underinsurance is more common than many people realize.

Several factors contribute to it.

1. Focus on Lower Premiums

Many policyholders prioritize lower monthly costs without fully evaluating coverage.

Choosing lower premiums often involves:

- Higher deductibles

- Lower coverage limits

- Fewer protections

While this reduces short-term cost, it may increase long-term financial exposure.

2. Misunderstanding Coverage

Insurance policies can be complex.

Without a clear understanding of:

- What is covered

- What is excluded

- How limits apply

Policyholders may assume they have more protection than they actually do.

3. Outdated Policies

Coverage that was appropriate in the past may not reflect current needs.

Examples:

- Property values increase over time

- Businesses expand operations

- New risks emerge

If policies are not updated, gaps may develop.

4. Ignoring Specific Risks

Some risks require additional coverage.

Examples include:

- Flood or earthquake insurance

- Cyber liability for digital businesses

- Professional liability for service providers

Without these, exposure may remain unprotected.

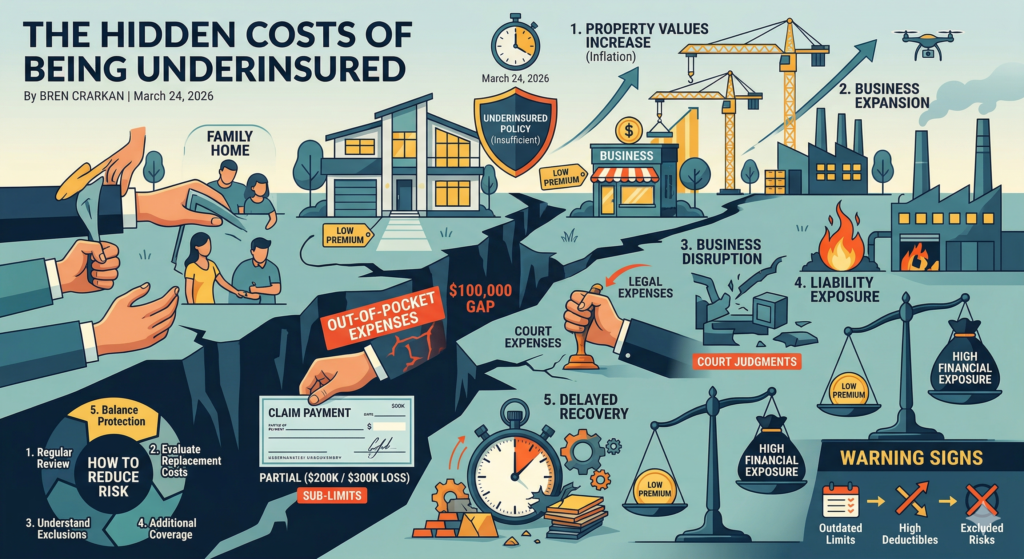

The Financial Impact of Underinsurance

The cost of underinsurance is often not visible until a claim occurs.

At that point, the financial gap becomes clear.

1. Out-of-Pocket Expenses

If a loss exceeds coverage limits, the policyholder is responsible for the remaining cost.

For example:

- A property loss of $300,000 with a policy limit of $200,000

- The remaining $100,000 may need to be covered personally

This gap can be financially significant.

2. Partial Claim Payments

Even when a claim is approved, it may not cover the full loss.

This can occur due to:

- Policy limits

- Sub-limits for specific categories

- Deductibles

Partial coverage can still result in substantial financial burden.

3. Business Disruption

For business owners, underinsurance can affect operational continuity.

Examples:

- Insufficient business interruption coverage

- Limited property protection

- Lack of liability coverage

These gaps can impact revenue, reputation, and long-term viability.

4. Liability Exposure

If liability coverage is insufficient, policyholders may be personally responsible for additional costs.

This can include:

- Legal expenses

- Settlement amounts

- Court judgments

Liability-related gaps can have long-term financial consequences.

5. Delayed Recovery

Underinsurance may slow down recovery after a loss.

Without adequate coverage:

- Repairs may be delayed

- Assets may not be fully replaced

- Operations may take longer to resume

Time is often a hidden cost.

Real-World Example

Consider a homeowner with property insurance that does not reflect current replacement costs.

If construction costs have increased over time, the policy limit may no longer be sufficient.

In the event of a major loss:

- Insurance may cover only part of the rebuilding cost

- The homeowner may need to cover the difference

This situation illustrates how underinsurance can develop gradually without obvious warning.

The Role of Inflation and Market Changes

Economic factors can increase the risk of underinsurance.

Examples include:

- Rising construction costs

- Increased labor expenses

- Higher medical costs

- Supply chain disruptions

Even if coverage was adequate initially, changing conditions may reduce its effectiveness over time.

How Deductibles Contribute to Underinsurance

High deductibles can also create financial gaps.

While they reduce premiums, they increase out-of-pocket responsibility.

If a deductible is set too high:

- It may be difficult to cover in an emergency

- Smaller claims may effectively go uninsured

Balancing deductibles with financial capacity is essential.

Underinsurance in Business Contexts

For businesses, underinsurance can take multiple forms.

1. Inadequate Liability Coverage

Businesses facing lawsuits may find that policy limits do not cover legal costs or settlements.

2. Insufficient Property Coverage

Equipment, inventory, and physical assets may be undervalued or incompletely insured.

3. Missing Coverage Types

Some businesses lack:

- Cyber insurance

- Professional liability coverage

- Business interruption protection

These gaps can expose the business to unexpected financial risk.

Warning Signs You May Be Underinsured

While underinsurance is not always obvious, some indicators include:

- Coverage limits that have not been updated in years

- Rapid increase in asset value or business growth

- Lack of coverage for specific risks

- Deductibles that exceed available emergency funds

- Policies that have not been reviewed recently

Regular review helps identify these gaps early.

How to Reduce the Risk of Underinsurance

1. Review Policies Regularly

Insurance should be reviewed periodically, especially after major changes.

2. Evaluate Replacement Costs

Ensure coverage reflects current market values, not outdated estimates.

3. Understand Exclusions and Limits

Knowing what is not covered is as important as knowing what is covered.

4. Consider Additional Coverage

Some risks require specialized policies or endorsements.

5. Balance Premiums and Protection

Lower cost should not come at the expense of essential coverage.

The Bigger Perspective

Insurance is not just about meeting minimum requirements.

It is about ensuring that protection aligns with real-world risks.

Underinsurance often results from focusing on short-term savings rather than long-term resilience.

A structured approach to coverage helps reduce financial uncertainty.

Final Thoughts

The hidden costs of being underinsured are often revealed only after a loss occurs.

At that point, gaps in coverage can lead to significant financial strain, delayed recovery, and increased personal responsibility.

Understanding the limitations of your policy — including coverage limits, exclusions, and deductibles — is essential for avoiding these risks.

Insurance works best when it is aligned with actual exposure, not just optimized for lower cost.

A well-informed approach helps ensure that protection is not only present, but also sufficient.