Home insurance is designed to protect one of the most important assets people own — their home. However, many homeowners are unsure how the claims process actually works until they need to use it.

Filing a home insurance claim can feel complex, especially during stressful situations like property damage or loss. Understanding the process in advance helps reduce confusion and improves the chances of a smoother experience.

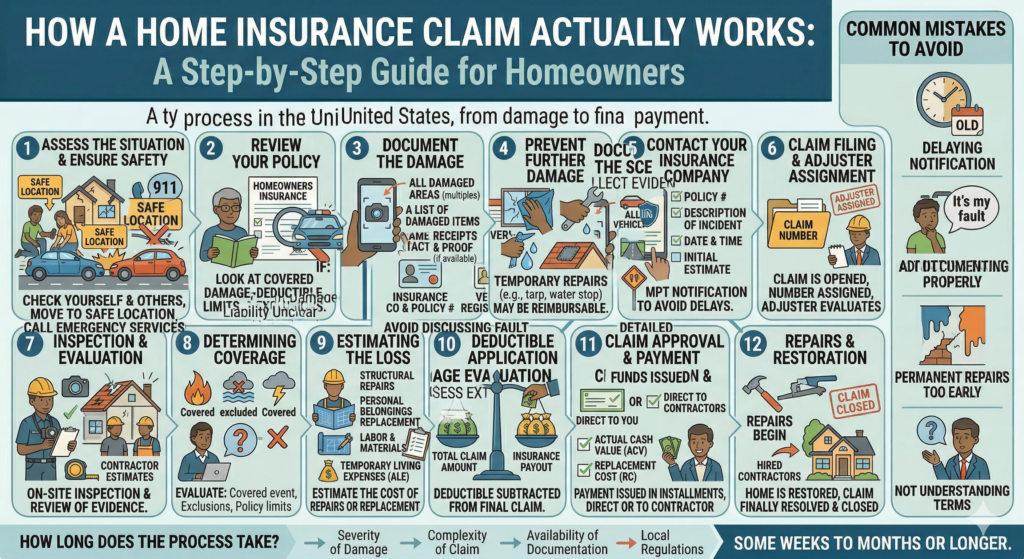

This guide explains how a home insurance claim actually works in the United States, step by step.

This article is for informational purposes only and does not constitute legal or insurance advice.

What Is a Home Insurance Claim?

A home insurance claim is a formal request made to your insurance company after a covered event causes damage or loss.

Common reasons for filing a claim include:

- Fire damage

- Water damage (depending on the cause)

- Theft or vandalism

- Storm-related damage

- Certain liability incidents

The purpose of a claim is to receive financial support according to the terms of your policy.

Step 1: Assess the Situation and Ensure Safety

Before thinking about insurance, safety comes first.

After an incident:

- Ensure everyone in the household is safe

- Address urgent hazards (fire, electrical issues, structural risks)

- Contact emergency services if needed

Only after immediate risks are under control should you begin the claims process.

Step 2: Review Your Policy

Before filing a claim, it is important to understand your coverage.

Look at:

- What types of damage are covered

- Your deductible

- Coverage limits

- Any exclusions that may apply

This helps you determine whether filing a claim is appropriate for your situation.

Step 3: Document the Damage

Proper documentation is essential.

You should gather:

- Photos of all damaged areas

- Videos if possible

- A list of damaged or lost items

- Receipts or proof of ownership (if available)

Avoid making permanent repairs before documentation, unless necessary to prevent further damage.

Step 4: Prevent Further Damage

Most policies require homeowners to take reasonable steps to prevent additional damage.

This may include:

- Covering broken windows

- Stopping water leaks

- Securing the property

Temporary repairs are usually acceptable and may be reimbursable depending on policy terms.

Step 5: Contact Your Insurance Company

Once you have documented the damage, notify your insurer.

You will typically need to provide:

- Policy number

- Description of the incident

- Date and time of loss

- Initial estimate of damage

Prompt reporting is important. Delays may affect claim processing.

Step 6: Claim Filing and Assignment

After you report the incident:

- A claim is opened

- A claim number is assigned

- An insurance adjuster may be assigned

The adjuster is responsible for evaluating the claim and determining how the policy applies.

Step 7: Inspection and Evaluation

The insurance company will assess the damage.

This may involve:

- On-site inspection by an adjuster

- Review of photos and documentation

- Contractor estimates

- Analysis of cause of damage

The insurer will determine whether the damage is covered under your policy.

Step 8: Determining Coverage

The insurer evaluates:

- Whether the cause of damage is covered

- Whether any exclusions apply

- How policy limits affect the claim

For example:

- Fire damage is typically covered

- Flood damage is often excluded unless additional coverage is in place

This step is critical in determining the outcome of the claim.

Step 9: Estimating the Loss

Once coverage is confirmed, the insurer estimates the cost of repairs or replacement.

This may include:

- Structural repairs

- Replacement of personal belongings

- Labor and materials

- Temporary living expenses (if applicable)

Estimates may vary depending on market conditions and contractor availability.

Step 10: Deductible Application

Your deductible is subtracted from the total claim amount.

For example:

- Total damage: $20,000

- Deductible: $1,000

- Insurance payout: $19,000 (subject to policy terms)

Understanding your deductible is important before filing a claim.

Step 11: Claim Approval and Payment

If the claim is approved:

- Payment may be issued in one or multiple installments

- Funds may be sent directly to you or to contractors

- Some payments may be based on actual cash value or replacement cost, depending on the policy

The payment structure depends on policy details.

Step 12: Repairs and Restoration

After receiving payment:

- Repairs can begin

- Contractors may be hired

- Property is restored

In some cases, insurers may provide recommendations, but homeowners typically have the option to choose their own contractors.

What If the Claim Is Partially Approved or Denied?

Not all claims are fully approved.

Possible outcomes include:

- Partial payment due to coverage limits

- Denial due to exclusions

- Disputes over damage valuation

If a claim is denied, policyholders may:

- Request clarification

- Provide additional documentation

- Review policy terms

Understanding the reason behind the decision is essential.

How Long Does the Process Take?

The timeline varies depending on:

- Severity of damage

- Complexity of the claim

- Availability of documentation

- Local regulations

Simple claims may be resolved in a few weeks, while larger claims may take longer.

Common Mistakes to Avoid

1. Waiting Too Long to File a Claim

Delays can complicate the process.

2. Not Documenting Damage Properly

Lack of evidence may affect claim evaluation.

3. Making Permanent Repairs Too Early

This can make it difficult to verify the extent of damage.

4. Not Understanding Policy Terms

Coverage, exclusions, and limits all affect the outcome.

When Filing a Claim May Not Be Ideal

Not every situation requires filing a claim.

Consider:

- Whether the damage exceeds your deductible

- Potential impact on future premiums

- Whether the issue can be handled out of pocket

Each situation should be evaluated carefully.

Why Understanding the Process Matters

Knowing how a home insurance claim works helps you:

- Act quickly and correctly

- Avoid common mistakes

- Meet policy requirements

- Reduce stress during difficult situations

Preparation can make a significant difference.

Final Thoughts

A home insurance claim is a structured process designed to evaluate damage, determine coverage, and provide financial support when appropriate.

While the process may seem complex, understanding each step — from documentation to final payment — helps homeowners navigate it more effectively.

Insurance is most valuable when you know how it works before you need it.

Taking the time to understand the claims process can help protect both your property and your financial stability.