Insurance policies are designed to provide continuous protection, but that protection depends on one key condition: keeping the policy active through regular payments.

Missing an insurance payment may seem like a small issue at first, but it can lead to serious consequences — including loss of coverage, policy cancellation, and financial exposure.

Understanding what happens if you miss an insurance payment can help you avoid gaps in protection and make better decisions when managing your policies.

This guide explains how missed payments are handled in the United States and what steps you can take if it happens.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

What Is Considered a Missed Insurance Payment?

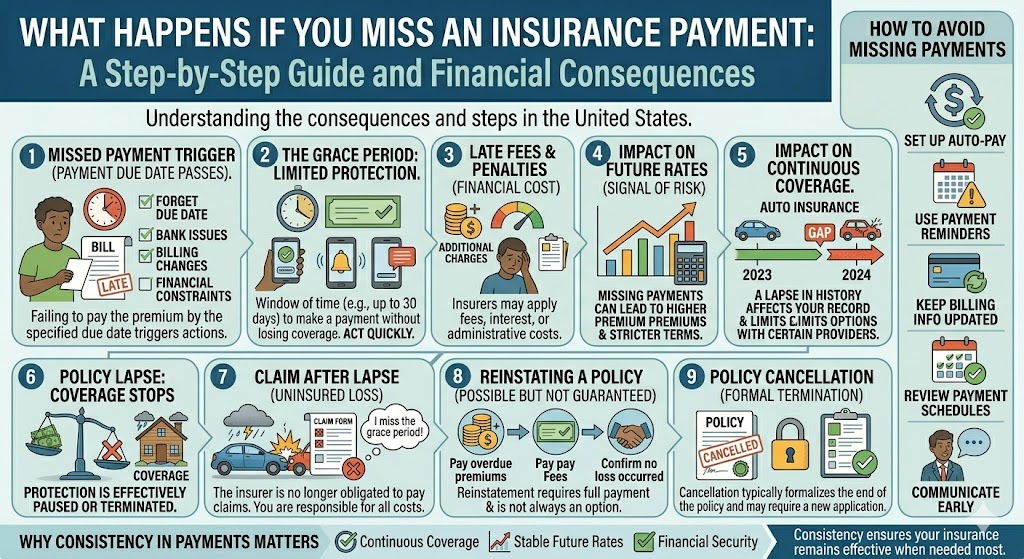

A missed payment occurs when a policyholder fails to pay the premium by the due date specified in the policy.

Depending on the insurer and policy type, payments may be:

- Monthly

- Quarterly

- Semi-annual

- Annual

Even a short delay can trigger specific actions under the policy terms.

The Grace Period: Your First Line of Protection

Most insurance policies include a grace period.

This is a limited window of time after the due date during which you can make a payment without immediately losing coverage.

Typical grace periods may range from:

- A few days

- Up to 30 days (depending on the policy and insurer)

During this period:

- Coverage may remain active

- Late fees may apply

- The insurer may send reminders

However, grace periods are not guaranteed for all policies and should not be relied upon as a long-term solution.

What Happens During the Grace Period?

If you miss a payment but are still within the grace period:

- Your policy is usually still in force

- Claims may still be processed (depending on terms)

- The insurer may notify you of the overdue balance

It is important to act quickly during this time to avoid further consequences.

Policy Lapse: When Coverage Stops

If payment is not made within the grace period, the policy may lapse.

A lapse means:

- Coverage is no longer active

- The insurer is no longer obligated to pay claims

- Protection is effectively paused or terminated

This is one of the most significant risks of missing a payment.

What Happens If You File a Claim After a Lapse?

If an incident occurs after your policy has lapsed:

- The claim may be denied

- You may be fully responsible for the costs

Even if the missed payment was recent, coverage may not apply once the policy is inactive.

Timing is critical.

Policy Cancellation vs Policy Lapse

While often used interchangeably, these terms can differ.

Policy Lapse

- Occurs due to non-payment

- May be reversible in some cases

Policy Cancellation

- May occur after a lapse or for other reasons

- Typically ends the policy formally

- May require a new application for future coverage

Understanding this distinction is important for next steps.

Reinstating a Policy

In some cases, insurers allow policies to be reinstated after a missed payment.

This may require:

- Paying overdue premiums

- Paying additional fees

- Confirming no losses occurred during the lapse

Reinstatement is not guaranteed and depends on the insurer and timing.

Impact on Future Insurance Rates

Missing payments can have long-term effects.

These may include:

- Higher premiums in the future

- Stricter payment terms

- Reduced eligibility with certain insurers

A lapse in coverage can signal higher risk to insurers.

Impact on Continuous Coverage

Some types of insurance — especially auto insurance — place importance on continuous coverage.

A lapse may:

- Affect your insurance history

- Increase future rates

- Limit options with certain providers

Maintaining continuous coverage is often beneficial.

Late Fees and Financial Penalties

Missing a payment may also result in:

- Late fees

- Interest charges

- Administrative costs

These costs may vary depending on the insurer and policy.

Real-World Example

Consider a driver who misses an auto insurance payment.

- Day 1: Payment due date passes

- Day 10: Grace period still active

- Day 20: No payment made → policy lapses

- Day 25: Accident occurs

In this scenario:

- The policy may no longer be active

- The claim may be denied

- The driver may be responsible for all damages

This illustrates how timing can significantly impact outcomes.

Common Reasons Payments Are Missed

Missing a payment is not always intentional.

Common reasons include:

- Forgetting the due date

- Bank or payment processing issues

- Changes in billing information

- Financial constraints

Understanding the cause can help prevent future issues.

How to Avoid Missing Insurance Payments

1. Set Up Automatic Payments

Auto-pay can help ensure payments are made on time.

2. Use Payment Reminders

Calendar alerts or notifications can reduce the risk of missed deadlines.

3. Keep Billing Information Updated

Ensure your payment method and contact details are current.

4. Review Payment Schedules

Understanding when payments are due helps avoid confusion.

5. Communicate with Your Insurer

If you anticipate a delay, contacting your insurer early may provide options.

What to Do If You Miss a Payment

If you realize you missed a payment:

- Check whether you are still within the grace period

- Make the payment as soon as possible

- Contact your insurer for confirmation

- Ask about reinstatement if the policy has lapsed

- Review your policy terms to understand next steps

Acting quickly can reduce potential consequences.

When Missing a Payment Becomes a Bigger Risk

Repeated missed payments may indicate:

- Financial strain

- Misalignment between coverage and budget

- Need for policy adjustment

In these cases, reviewing your coverage structure may be helpful.

Why This Matters More Than It Seems

Missing a single payment may appear minor, but the consequences can extend beyond the immediate situation.

It can affect:

- Your current protection

- Your ability to file claims

- Your future insurance options

- Your overall financial stability

Insurance works best when coverage remains uninterrupted.

Final Thoughts

Missing an insurance payment can lead to a chain of consequences, from late fees to policy lapse and loss of coverage.

While many policies offer a grace period, relying on it can be risky. Acting quickly after a missed payment is essential to maintaining protection.

Understanding how your policy handles missed payments — and taking steps to prevent them — helps ensure that your insurance remains effective when you need it most.

Consistency in payments is not just about compliance. It is a key part of maintaining financial security.