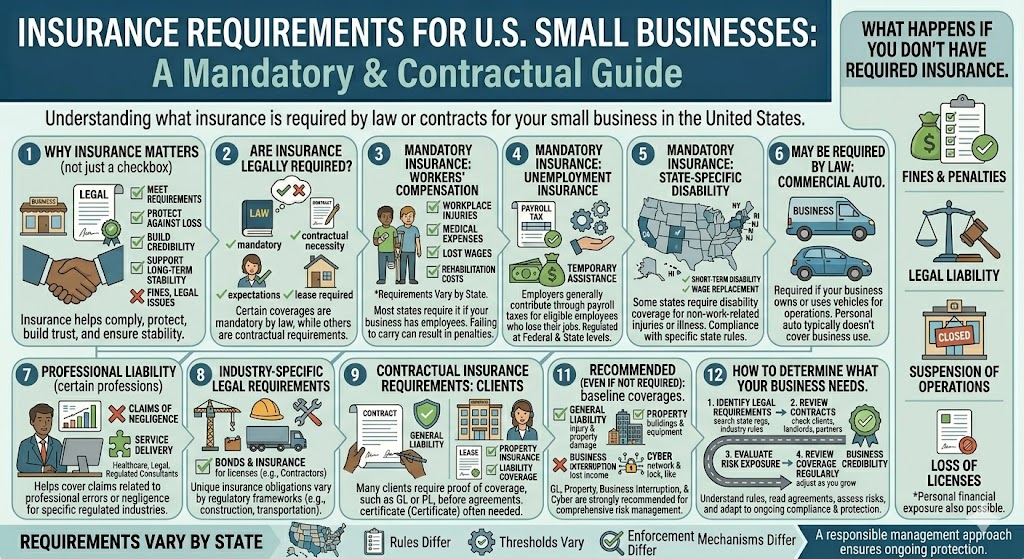

Starting and growing a small business in the United States involves more than developing products or services. One of the most important — and often overlooked — aspects is understanding insurance requirements.

Depending on the type of business, location, and operations, certain types of insurance may be legally required, while others are strongly recommended to manage risk.

This guide explains the insurance requirements for U.S. small businesses, including mandatory coverage, common expectations, and how to approach insurance from a compliance and protection perspective.

This article is for informational purposes only and does not constitute legal or insurance advice.

Why Insurance Matters for Small Businesses

Insurance is not just about protection — it is often a legal and contractual necessity.

For small businesses, insurance helps:

- Meet state and federal requirements

- Protect against financial loss

- Build credibility with clients and partners

- Support long-term stability

Failing to carry required insurance can lead to fines, legal issues, or operational restrictions.

Are Insurance Policies Legally Required?

Not all types of business insurance are mandatory.

However, certain coverages are required by law in most states, while others may be required by:

- Contracts

- Landlords

- Clients

- Industry regulations

Understanding the difference is essential.

Mandatory Insurance for Small Businesses

1. Workers’ Compensation Insurance

Workers’ compensation is one of the most commonly required types of business insurance.

Most states require it if your business has employees.

It typically covers:

- Workplace injuries

- Medical expenses

- Lost wages

- Rehabilitation costs

Requirements vary by state, including:

- Number of employees required before coverage is mandatory

- Industry-specific rules

Failing to carry workers’ compensation when required can result in significant penalties.

2. Unemployment Insurance

Employers are generally required to participate in unemployment insurance programs.

This system provides temporary financial assistance to eligible employees who lose their jobs.

Employers contribute through payroll taxes, and requirements are regulated at both federal and state levels.

3. Disability Insurance (State-Specific)

Some states require disability insurance coverage.

This may include:

- Short-term disability benefits

- Wage replacement for non-work-related injuries or illness

States with such requirements include:

- California

- New York

- New Jersey

- Rhode Island

- Hawaii

Businesses operating in these states must comply with specific rules.

Insurance That May Be Required by Law Depending on Your Business

1. Commercial Auto Insurance

If your business owns or uses vehicles for operations, commercial auto insurance may be required.

This applies to:

- Company-owned vehicles

- Vehicles used for business purposes

Personal auto policies typically do not cover business-related use.

2. Professional Liability Insurance (Certain Professions)

Some industries require professional liability coverage.

Examples include:

- Healthcare providers

- Legal professionals

- Financial advisors

- Consultants in regulated fields

This insurance helps cover claims related to professional errors or negligence.

3. Industry-Specific Requirements

Certain industries have unique insurance obligations.

Examples:

- Construction businesses may need specific liability coverage

- Contractors may need bonding and insurance to obtain licenses

- Transportation businesses may require higher liability limits

Requirements vary based on regulatory frameworks.

Contractual Insurance Requirements

Even when insurance is not legally required, it may still be mandatory through contracts.

1. Client Contracts

Many clients require businesses to carry insurance before entering into agreements.

This may include:

- General liability coverage

- Professional liability insurance

- Proof of insurance (certificate of insurance)

2. Commercial Leases

Landlords often require tenants to carry insurance.

This may include:

- Property insurance

- Liability coverage

Lease agreements may specify minimum coverage limits.

3. Vendor and Partnership Agreements

Businesses working with vendors or partners may need to meet insurance requirements as part of contractual obligations.

Commonly Recommended Insurance (Even If Not Required)

While not always mandatory, certain policies are widely considered essential.

1. General Liability Insurance

Covers:

- Bodily injury

- Property damage

- Legal defense costs

Often considered a baseline for most businesses.

2. Property Insurance

Protects:

- Buildings

- Equipment

- Inventory

Important for businesses with physical assets.

3. Business Interruption Insurance

Helps cover lost income if operations are disrupted due to a covered event.

4. Cyber Insurance

Increasingly relevant for businesses that:

- Store customer data

- Operate online

- Use digital systems

Covers risks such as data breaches and cyberattacks.

How Requirements Vary by State

Insurance requirements are regulated primarily at the state level.

This means:

- Rules differ depending on location

- Coverage thresholds may vary

- Enforcement mechanisms differ

Business owners should review state-specific regulations to ensure compliance.

What Happens If You Don’t Have Required Insurance?

Failure to carry required insurance can result in:

- Fines and penalties

- Legal liability

- Suspension of business operations

- Loss of licenses or permits

In some cases, business owners may also face personal financial exposure.

How to Determine What Your Business Needs

1. Identify Legal Requirements

Research:

- State regulations

- Industry-specific rules

- Licensing requirements

2. Review Contracts

Check agreements with:

- Clients

- Landlords

- Partners

3. Evaluate Risk Exposure

Consider:

- Type of business

- Number of employees

- Nature of operations

- Physical and digital assets

4. Review Coverage Regularly

As your business grows, requirements and risks may change.

Regular reviews help ensure ongoing compliance.

Real-World Example

A small consulting business may initially operate without employees.

At this stage:

- Workers’ compensation may not be required

- General liability may be optional

As the business grows and hires employees:

- Workers’ compensation becomes mandatory

- Client contracts may require liability coverage

This illustrates how insurance requirements evolve with business growth.

The Role of Insurance in Business Credibility

Insurance is not only about compliance.

It also signals professionalism and reliability.

Businesses with proper coverage may:

- Build stronger client trust

- Qualify for larger contracts

- Reduce perceived risk for partners

Insurance can support both protection and growth.

Final Thoughts

Insurance requirements for U.S. small businesses depend on a combination of legal obligations, contractual commitments, and operational risks.

While some types of insurance are mandatory, others play a critical role in protecting the business and supporting long-term success.

Understanding these requirements — and reviewing them regularly — helps ensure compliance, reduce risk, and build a more resilient business.

Insurance is not just a regulatory checkbox. It is a key part of responsible business management.