Starting a business is an exciting process, especially for first-time founders. From building a product to finding customers, most of the focus is on growth and innovation. However, one critical area is often underestimated: insurance.

For startups, insurance is not just a formality — it is a key part of risk management. Without the right coverage, a single unexpected event could disrupt operations or create financial strain.

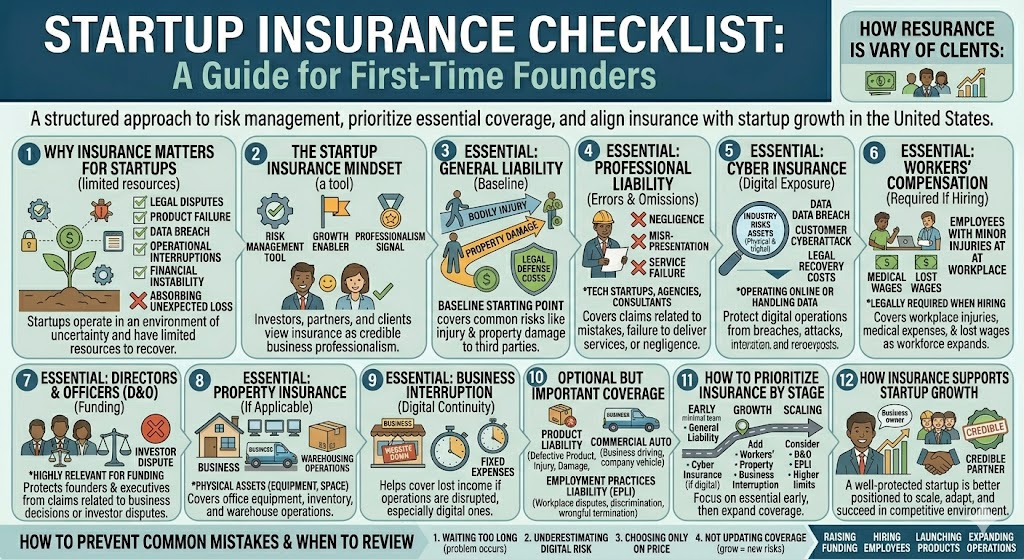

This startup insurance checklist is designed to help first-time founders understand what coverage they may need, how to prioritize it, and how to align insurance with business growth.

This article is for informational purposes only and does not constitute legal or insurance advice.

Why Insurance Matters for Startups

Startups operate in an environment of uncertainty.

Common risks include:

- Legal disputes

- Product or service failures

- Data breaches

- Operational interruptions

- Financial instability

Unlike established businesses, startups often have limited resources to absorb unexpected losses.

Insurance helps reduce that uncertainty.

The Startup Insurance Mindset

Before choosing policies, founders should shift how they think about insurance.

It is not just:

- A cost

- A requirement

It is:

- A risk management tool

- A growth enabler

- A signal of professionalism

Investors, partners, and clients may view insurance as part of business credibility.

The Essential Startup Insurance Checklist

1. General Liability Insurance

This is often the starting point for most businesses.

It may cover:

- Third-party bodily injury

- Property damage

- Legal defense costs

Even early-stage startups can face liability risks.

2. Professional Liability (Errors & Omissions)

Critical for startups offering services or digital products.

It covers claims related to:

- Mistakes

- Failure to deliver services

- Negligence

For tech startups, agencies, and consultants, this is often essential.

3. Cyber Insurance

For startups operating online or handling data, this is one of the most important coverages.

It may include:

- Data breach response

- Cyberattack recovery

- Business interruption

- Legal costs

As digital operations grow, so does exposure.

4. Workers’ Compensation (If Hiring Employees)

Once a startup hires employees, this is often legally required.

It covers:

- Workplace injuries

- Medical expenses

- Lost wages

Requirements vary by state.

5. Directors and Officers (D&O) Insurance

Highly relevant for startups seeking funding.

It protects founders and executives from claims related to:

- Business decisions

- Investor disputes

- Regulatory issues

Investors may require this before funding.

6. Property Insurance (If Applicable)

If the startup owns or leases physical assets:

- Equipment

- Office space

- Inventory

Property insurance helps protect against loss or damage.

7. Business Interruption Insurance

Startups often rely on continuous operations.

This coverage may help if:

- Operations are disrupted

- Revenue is temporarily lost

Particularly relevant for digital businesses.

Optional but Important Coverage

1. Product Liability Insurance

For startups selling physical products.

Covers claims related to:

- Defective products

- Injury or damage caused by products

2. Commercial Auto Insurance

If vehicles are used for business purposes.

3. Employment Practices Liability Insurance (EPLI)

Covers claims related to:

- Wrongful termination

- Discrimination

- Workplace disputes

As teams grow, this becomes more relevant.

How to Prioritize Insurance as a Founder

Not every startup needs every policy immediately.

Prioritization depends on:

- Business model

- Industry

- Stage of growth

- Risk exposure

Early Stage (Pre-Revenue or Small Teams)

Focus on:

- General liability

- Professional liability (if applicable)

- Cyber insurance (for digital startups)

Growth Stage

Add:

- Workers’ compensation

- Property insurance

- Business interruption

Scaling Stage

Consider:

- D&O insurance

- EPLI

- Higher coverage limits

Common Mistakes First-Time Founders Make

1. Waiting Too Long

Many founders delay insurance until a problem occurs.

2. Underestimating Digital Risk

Cyber threats are often overlooked early on.

3. Choosing Coverage Based Only on Price

Lower premiums may mean reduced protection.

4. Not Updating Coverage

As startups grow, their risk profile changes.

Real-World Example

A startup launches a SaaS platform.

Initially:

- It operates with minimal coverage

As it grows:

- It stores customer data → cyber risk increases

- It signs contracts → liability exposure increases

- It raises funding → D&O becomes relevant

Without updating insurance, the startup may face significant gaps.

How Insurance Supports Startup Growth

Insurance is not just about protection.

It also helps:

- Build trust with clients

- Meet contractual requirements

- Attract investors

- Reduce uncertainty

For startups, this can be a competitive advantage.

The Role of Technology in Startup Insurance

Modern insurance solutions are evolving to support startups.

These may include:

- Flexible, on-demand coverage

- Digital policy management

- Data-driven risk assessment

- Scalable pricing models

This aligns well with the fast-paced nature of startups.

When to Review Your Insurance

Startups should review coverage:

- After raising funding

- When hiring employees

- When launching new products

- When expanding operations

Regular review helps ensure alignment with growth.

Final Thoughts

For first-time founders, insurance may not seem like a priority compared to product development or growth.

However, it plays a critical role in protecting the business from unexpected risks.

Using a structured checklist helps ensure that essential coverage is in place and evolves alongside the startup.

Insurance is not just about avoiding problems — it is about building a foundation for sustainable growth.

A well-protected startup is better positioned to scale, adapt, and succeed in a competitive environment.