When investors evaluate a startup, they are not only looking at growth potential, product innovation, or market size. One of the most critical — and often overlooked — factors is risk.

Startups operate in uncertain environments, and investors are fully aware that risk is unavoidable. What they care about is how well that risk is understood, managed, and mitigated.

Insurance plays a key role in this evaluation. While it is not always the first topic discussed in pitch meetings, it becomes increasingly important during due diligence and scaling stages.

Understanding how investors evaluate risk and insurance in startups can help founders build stronger, more resilient companies — and improve their chances of securing funding.

This article is for informational purposes only and does not constitute financial, legal, or investment advice.

Why Risk Matters More Than Growth for Investors

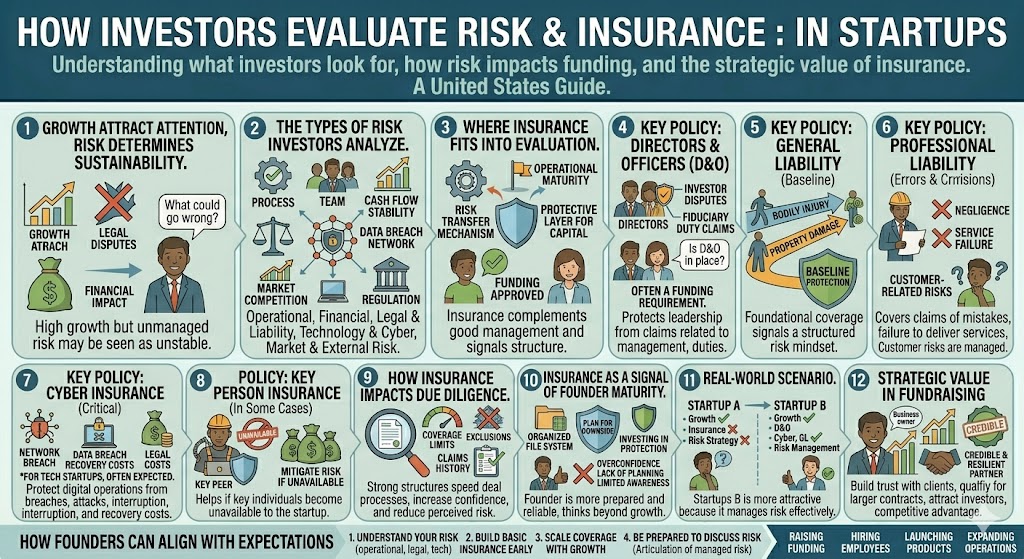

Growth attracts attention, but risk determines sustainability.

Investors typically ask:

- What could go wrong?

- How likely is it?

- What is the financial impact?

- How is the company prepared to handle it?

A startup with high growth but unmanaged risk may be seen as unstable.

Insurance is one of the tools that signals structured risk management.

The Types of Risk Investors Analyze

1. Operational Risk

This includes:

- Internal processes

- Team structure

- Execution capability

Investors assess whether the startup can operate reliably as it grows.

2. Financial Risk

Concerns include:

- Cash flow stability

- Burn rate

- Exposure to unexpected costs

Insurance can help reduce certain financial shocks.

3. Legal and Liability Risk

This is one of the most critical areas.

It includes:

- Lawsuits

- Contract disputes

- Regulatory compliance

Without proper protection, legal issues can severely impact a startup.

4. Technology and Cyber Risk

For tech-driven startups, this is a major focus.

Risks include:

- Data breaches

- System failures

- Security vulnerabilities

Investors expect startups to address these risks proactively.

5. Market and External Risk

These include:

- Competition

- Economic conditions

- Regulatory changes

While not all of these can be insured, they are part of the broader risk picture.

Where Insurance Fits Into Investor Evaluation

Insurance is not a replacement for good management — but it complements it.

Investors view insurance as:

- A risk transfer mechanism

- A sign of operational maturity

- A protective layer for capital

It shows that founders are thinking beyond growth and considering downside scenarios.

Key Insurance Policies Investors Look For

1. Directors and Officers (D&O) Insurance

This is one of the most important policies from an investor perspective.

It protects:

- Founders

- Executives

- Board members

From claims related to:

- Mismanagement

- Fiduciary duties

- Investor disputes

Many investors require D&O coverage before finalizing funding.

2. General Liability Insurance

Provides baseline protection against common risks.

While basic, it signals that the startup has foundational coverage.

3. Professional Liability (Errors & Omissions)

Important for startups providing services or technology.

Covers:

- Product or service failures

- Negligence claims

Investors want to know that customer-related risks are managed.

4. Cyber Insurance

For tech startups, this is increasingly critical.

It may cover:

- Data breaches

- Cyberattacks

- Recovery costs

Given the importance of data, this is often expected rather than optional.

5. Key Person Insurance (In Some Cases)

Startups often depend heavily on founders.

This type of insurance helps mitigate risk if a key individual becomes unavailable.

How Insurance Impacts Due Diligence

During due diligence, investors take a deeper look at risk management.

They may review:

- Existing insurance policies

- Coverage limits

- Exclusions

- Claims history

Gaps in coverage can raise concerns.

Strong insurance structures can:

- Increase confidence

- Speed up deal processes

- Reduce perceived risk

Insurance as a Signal of Founder Maturity

Investors often interpret insurance decisions as a reflection of the founder’s mindset.

A founder who:

- Understands risk

- Plans for downside scenarios

- Invests in protection

Is often seen as more prepared and reliable.

On the other hand, ignoring insurance may signal:

- Overconfidence

- Lack of planning

- Limited operational awareness

Real-World Scenario

Imagine two similar startups:

Startup A:

- Strong growth

- No insurance

- No formal risk strategy

Startup B:

- Similar growth

- Has D&O, cyber, and liability coverage

- Demonstrates structured risk management

From an investor perspective, Startup B may be more attractive — not because it has less risk, but because it manages risk more effectively.

Common Mistakes Founders Make

1. Thinking Insurance Is Only for Later Stages

Many founders delay insurance until after funding.

However, investors may expect it earlier.

2. Underestimating Legal Risk

Even early-stage startups can face legal challenges.

3. Ignoring Cyber Exposure

Digital risk is one of the most critical areas for modern startups.

4. Treating Insurance as a Formality

Insurance should be part of a broader risk strategy.

How Founders Can Align with Investor Expectations

1. Understand Your Risk Profile

Identify:

- Operational risks

- Legal exposure

- Technology risks

2. Build a Basic Insurance Structure Early

Even minimal coverage can signal preparedness.

3. Scale Coverage with Growth

As the startup evolves, coverage should expand accordingly.

4. Be Prepared to Discuss Risk

Investors expect founders to articulate:

- What risks exist

- How they are managed

- Where insurance fits

The Strategic Value of Insurance in Fundraising

Insurance is not just protection — it can support fundraising efforts.

It helps:

- Reduce perceived risk

- Increase investor confidence

- Support negotiations

- Protect valuation

In some cases, it may even be a requirement for closing deals.

The Role of Technology in Modern Risk Evaluation

Investors increasingly rely on data-driven insights.

This includes:

- Risk analytics

- Cybersecurity assessments

- Operational metrics

Insurance is evolving alongside these tools, offering more tailored solutions for startups.

Final Thoughts

Investors do not expect startups to eliminate risk — that is impossible.

What they expect is awareness, preparation, and structured management.

Insurance plays a key role in this process by providing a layer of financial protection and signaling operational maturity.

For founders, understanding how investors evaluate risk and insurance is not just about compliance. It is about positioning the company as resilient, credible, and ready to scale.

In the world of startups, managing risk effectively can be just as important as driving growth.