Insurance is one of the most important tools for financial protection — yet it is also one of the most misunderstood.

Many people make decisions based on assumptions, outdated advice, or common myths. These misunderstandings can lead to poor coverage choices, higher costs, or denied claims.

Believing the wrong information about insurance can be expensive.

This guide breaks down the most common insurance myths that can hurt you — and explains what you should know instead.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

Why Insurance Myths Are So Dangerous

Insurance is complex, and most people do not read policies in detail.

As a result:

- Misconceptions spread easily

- Advice is often oversimplified

- Important details are ignored

The problem is that these myths usually go unnoticed until something goes wrong.

At that point, the consequences can be costly.

The Most Common Insurance Myths (And the Truth Behind Them)

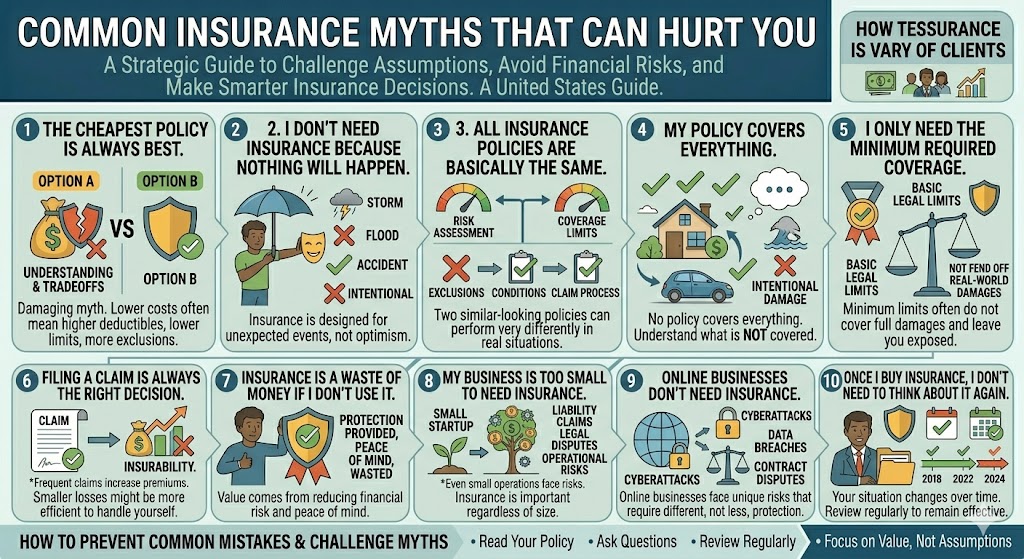

1. “The Cheapest Policy Is Always the Best Option”

This is one of the most damaging myths.

Reality:

Lower-cost policies often include:

- Higher deductibles

- Lower coverage limits

- More exclusions

Choosing based only on price can leave you underprotected.

2. “I Don’t Need Insurance Because Nothing Will Happen to Me”

This belief is based on optimism, not risk management.

Reality:

Insurance is designed for unexpected events.

Even low-probability situations can have high financial impact.

3. “All Insurance Policies Are Basically the Same”

Many people assume policies are interchangeable.

Reality:

Policies differ in:

- Coverage limits

- Exclusions

- Conditions

- Claim processes

Two similar-looking policies can perform very differently in real situations.

4. “My Policy Covers Everything”

No insurance policy covers everything.

Reality:

Every policy has exclusions.

Understanding what is NOT covered is just as important as knowing what is covered.

5. “I Only Need the Minimum Required Coverage”

Minimum coverage may meet legal requirements — but not real-world needs.

Reality:

Minimum limits often:

- Do not cover full damages

- Leave you financially exposed

Adequate coverage should reflect your actual risk.

6. “Filing a Claim Is Always the Right Decision”

Many people assume they should file a claim whenever something happens.

Reality:

Frequent claims can:

- Increase premiums

- Affect insurability

Sometimes, handling smaller losses yourself may be more efficient.

7. “Insurance Is a Waste of Money If I Don’t Use It”

This is a common misconception.

Reality:

Insurance is not an investment — it is protection.

Its value comes from:

- Reducing financial risk

- Providing peace of mind

Not using it does not mean it has no value.

8. “My Business Is Too Small to Need Insurance”

Small businesses often underestimate risk.

Reality:

Even small operations face:

- Liability claims

- Legal disputes

- Operational risks

Insurance is important regardless of size.

9. “Online Businesses Don’t Need Insurance”

This myth is increasingly common.

Reality:

Online businesses face risks such as:

- Cyberattacks

- Data breaches

- Contract disputes

Digital operations require different — not less — protection.

10. “Once I Buy Insurance, I Don’t Need to Think About It Again”

Many people treat insurance as a one-time decision.

Reality:

Your situation changes over time.

Policies should be reviewed regularly to remain effective.

Real-World Example

Consider a homeowner who believes their policy covers all types of damage.

After a specific incident:

- A claim is filed

- The insurer denies it due to an exclusion

The misunderstanding was not about having insurance — it was about not understanding it.

This type of situation is more common than many people realize.

Why These Myths Persist

Insurance myths continue because:

- Policies are complex

- People rely on informal advice

- Marketing messages simplify reality

- Few people review policy details

Without proper understanding, myths become accepted as truth.

How to Avoid Falling for Insurance Myths

1. Read and Understand Your Policy

Focus on:

- Coverage

- Exclusions

- Limits

2. Ask Questions

If something is unclear, clarify before making decisions.

3. Review Policies Regularly

Ensure your coverage reflects your current situation.

4. Focus on Value, Not Assumptions

Base decisions on facts, not common beliefs.

The Cost of Believing the Wrong Information

Insurance myths may seem harmless, but they can lead to:

- Financial losses

- Coverage gaps

- Claim denials

- Poor decision-making

Correct information leads to better protection.

The Strategic Perspective

Understanding insurance is not just about avoiding mistakes — it is about making informed decisions.

A clear and accurate view of insurance helps:

- Improve financial stability

- Reduce uncertainty

- Align coverage with real risks

For businesses, it also strengthens long-term resilience.

Final Thoughts

Insurance myths are common, but they can have serious consequences.

By challenging assumptions and understanding how insurance actually works, you can make better decisions and avoid costly mistakes.

The goal is not just to have insurance — but to have the right insurance, based on accurate information.

Taking the time to understand your coverage today can prevent major problems in the future.