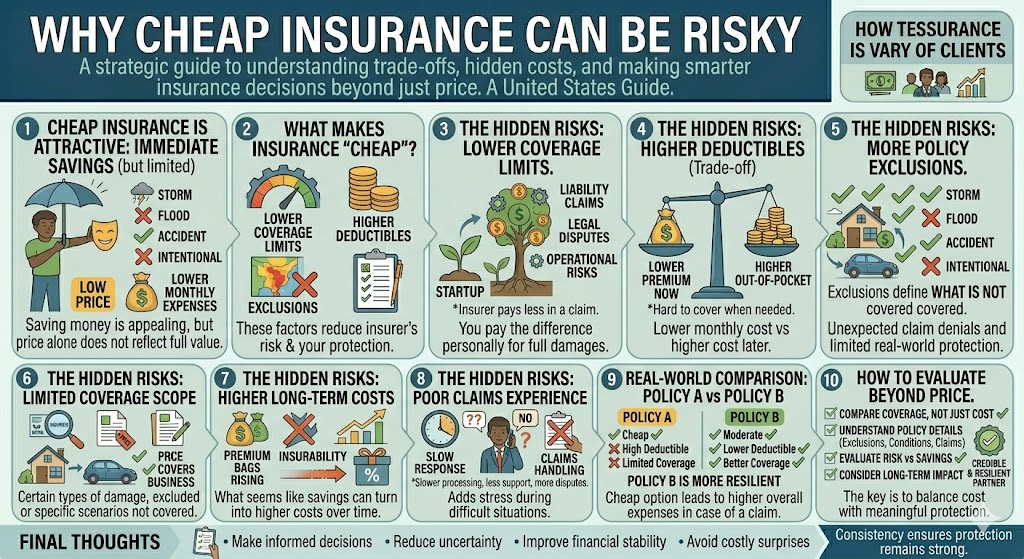

When choosing insurance, it is natural to look for the lowest price. Saving money is a priority for most individuals and businesses, and insurance premiums can feel like an expense you want to minimize.

However, cheap insurance is not always a good deal.

In many cases, lower premiums come with trade-offs that may not be obvious at first. These trade-offs can lead to insufficient protection, higher out-of-pocket costs, or unexpected issues when filing a claim.

Understanding why cheap insurance can be risky helps you make better decisions and avoid costly mistakes.

This article is for informational purposes only and does not constitute financial or insurance advice.

Why Cheap Insurance Is So Attractive

Low-cost policies are appealing for several reasons:

- Immediate savings

- Lower monthly expenses

- Simple comparison (price is easy to evaluate)

However, price alone does not reflect the full value of an insurance policy.

Insurance is not a standard product — it varies significantly in terms of coverage and conditions.

What Makes Insurance “Cheap”?

A policy may be cheaper for several reasons:

- Lower coverage limits

- Higher deductibles

- More exclusions

- Fewer included benefits

- Stricter claim conditions

These factors reduce the insurer’s risk — and your protection.

The Hidden Risks of Cheap Insurance

1. Lower Coverage Limits

Cheap policies often have lower limits on payouts.

This means:

- The insurer pays less in a claim

- You may need to cover the remaining costs

In serious situations, this can result in significant financial loss.

2. Higher Deductibles

Many low-cost policies come with high deductibles.

This creates a trade-off:

- Lower premium now

- Higher out-of-pocket cost later

If the deductible is too high, you may struggle to cover it when needed.

3. More Policy Exclusions

Exclusions define what is not covered — and cheaper policies often include more of them.

This can lead to:

- Unexpected claim denials

- Limited real-world protection

Understanding exclusions is critical.

4. Limited Coverage Scope

Some policies appear complete but actually cover fewer risks.

For example:

- Certain types of damage may be excluded

- Specific scenarios may not be covered

This reduces the effectiveness of the policy.

5. Higher Long-Term Costs

Cheap insurance may save money upfront, but cost more over time.

This can happen if:

- Claims are partially covered

- Out-of-pocket expenses increase

- Additional coverage becomes necessary

What seems like savings can become more expensive.

6. Poor Claims Experience

Lower-cost providers or policies may offer:

- Slower claim processing

- Less support

- More disputes

This can add stress during already difficult situations.

7. Insufficient Liability Protection

Liability claims can be expensive.

Cheap policies often have:

- Lower liability limits

- Less comprehensive protection

This can expose you to significant financial risk.

Real-World Example

Consider two insurance policies:

Policy A (Cheap):

- Low premium

- High deductible

- Limited coverage

Policy B (Moderate Cost):

- Slightly higher premium

- Lower deductible

- Better coverage limits

At first, Policy A seems more attractive.

However, in the event of a claim:

- Out-of-pocket costs are higher

- Coverage may not be sufficient

In this case, the “cheap” option may lead to higher overall expenses.

When Cheap Insurance Might Be Acceptable

Cheap insurance is not always a bad choice.

It may work if:

- Your risk exposure is low

- You can afford higher out-of-pocket costs

- You fully understand the limitations

The key is awareness — not assumption.

How to Evaluate Insurance Beyond Price

1. Compare Coverage, Not Just Cost

Ensure policies have:

- Similar limits

- Similar deductibles

- Comparable coverage scope

2. Understand Policy Details

Review:

- Exclusions

- Conditions

- Claim processes

3. Evaluate Risk vs Savings

Ask:

- What am I giving up for a lower price?

- Is the risk worth the savings?

4. Consider Long-Term Impact

Think beyond the premium:

- What happens during a claim?

Common Mistakes Related to Cheap Insurance

1. Choosing Based Only on Price

This is the most common mistake.

2. Ignoring Fine Print

Important details are often overlooked.

3. Underestimating Risk

Low probability does not mean low impact.

4. Not Reviewing Policies

Cheap policies may become inefficient over time.

The Strategic Perspective

Insurance should be viewed as a balance between cost and protection.

Cheap insurance shifts that balance toward lower cost — but often at the expense of protection.

A strategic approach focuses on:

- Value

- Adequate coverage

- Financial resilience

For businesses, this is especially important, as insufficient coverage can affect operations and growth.

Final Thoughts

Cheap insurance may seem like a smart financial decision, but it often comes with hidden risks.

Lower premiums can mean reduced protection, higher out-of-pocket costs, and potential gaps in coverage.

The goal is not to find the cheapest policy, but the most efficient one — a policy that balances cost with meaningful protection.

Understanding what you are paying for is essential to making informed decisions and avoiding costly surprises.