Auto insurance is one of the most common and essential types of insurance in the United States. For most drivers, it is not optional. Nearly every state requires a minimum level of coverage before a vehicle can be legally driven on public roads. However, beyond legal compliance, auto insurance serves a much broader purpose: it protects drivers from potentially significant financial and legal consequences.

Understanding how auto insurance works, what it covers, and how to choose appropriate coverage is critical for responsible vehicle ownership. Many drivers purchase policies without fully understanding the details, which can lead to unexpected gaps in protection when accidents occur.

This guide explains auto insurance clearly and thoroughly so drivers can make informed decisions.

Why Auto Insurance Is Required in Most States

Auto accidents can result in property damage, injuries, and legal claims. Without insurance, drivers would be personally responsible for paying all related costs out of pocket. In serious accidents, these costs can be substantial.

State laws require minimum liability insurance to ensure that drivers can compensate others if they cause harm. These laws are designed to promote financial responsibility and protect victims of accidents.

While minimum coverage satisfies legal requirements, it may not always provide adequate protection in severe situations.

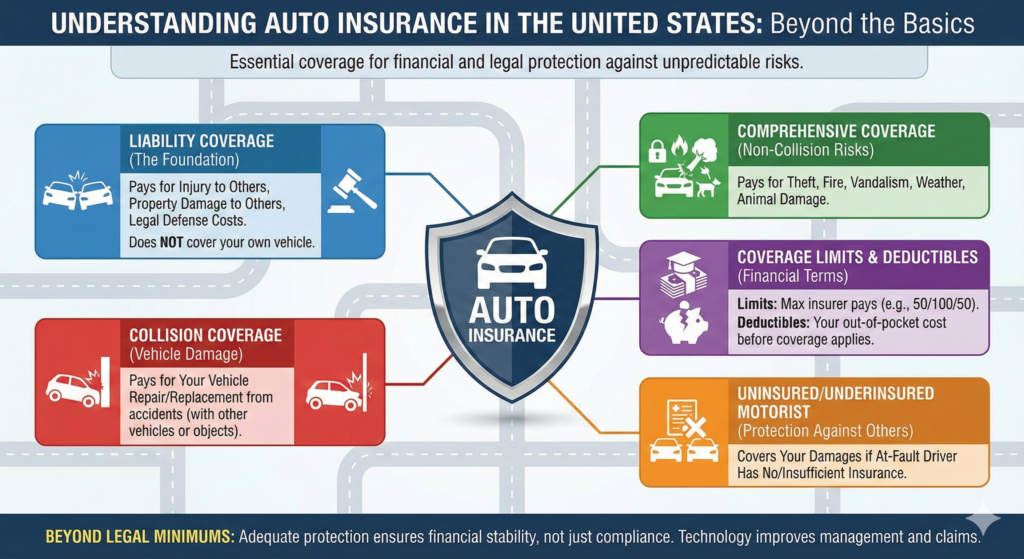

The Core Components of Auto Insurance

Auto insurance policies typically include several types of coverage. Each serves a different purpose.

Liability Coverage

Liability coverage is the foundation of most auto insurance policies. It pays for:

- Bodily injury to others

- Property damage to another person’s vehicle or property

- Legal defense costs related to covered accidents

Liability coverage does not pay for damage to your own vehicle. Instead, it protects you from financial responsibility if you are found at fault.

Collision Coverage

Collision coverage pays for damage to your own vehicle resulting from an accident, regardless of who is at fault. This includes collisions with other vehicles or objects such as trees, poles, or barriers.

Collision coverage is often required if a vehicle is financed or leased. It helps repair or replace the vehicle after an accident.

Comprehensive Coverage

Comprehensive coverage protects against non-collision-related damage. This includes:

- Theft

- Vandalism

- Fire

- Falling objects

- Natural disasters

- Animal-related damage

Comprehensive coverage provides broader protection beyond accidents involving other vehicles.

Uninsured and Underinsured Motorist Coverage

Not all drivers carry adequate insurance. Uninsured motorist coverage protects you if you are involved in an accident with someone who has no insurance. Underinsured motorist coverage applies when the other driver’s coverage is insufficient to cover damages.

This type of coverage is particularly important in areas where uninsured driving rates are higher.

Understanding Coverage Limits

Auto insurance policies include coverage limits that define the maximum amount the insurer will pay for a covered claim.

Liability limits are often expressed in three numbers, such as 50/100/50. These represent:

- The maximum payout per injured person

- The maximum payout per accident

- The maximum payout for property damage

Selecting appropriate limits is critical. Minimum state limits may not reflect the actual cost of medical treatment or vehicle repairs in serious accidents.

Deductibles in Auto Insurance

Collision and comprehensive coverage typically include deductibles. A deductible is the amount you must pay out of pocket before the insurer covers the remaining costs.

Higher deductibles generally result in lower premiums, while lower deductibles increase premium costs. Choosing a deductible requires balancing affordability with financial preparedness in case of an accident.

Factors That Affect Auto Insurance Premiums

Insurance companies evaluate risk when determining premiums. Several factors commonly influence pricing:

- Driving history

- Age and driving experience

- Location

- Type of vehicle

- Mileage and usage

- Claims history

Safe driving records and responsible behavior often result in lower premiums. Conversely, traffic violations or prior claims may increase costs.

Optional Add-Ons and Endorsements

Many insurers offer additional coverage options that can enhance protection.

Examples include:

- Rental car reimbursement

- Roadside assistance

- Gap insurance (for financed vehicles)

- Custom equipment coverage

These add-ons can provide convenience and additional financial security depending on individual needs.

The Claims Process

When an accident occurs, the claims process begins. Policyholders typically need to:

- Report the incident promptly

- Provide documentation and evidence

- Cooperate with the insurer’s investigation

The insurer evaluates coverage, determines fault where applicable, and processes payment according to policy terms.

Understanding the claims process in advance can reduce stress during difficult situations.

Minimum Coverage vs. Adequate Protection

While minimum state-required coverage allows drivers to operate legally, it may not fully protect against serious financial exposure.

Medical expenses, vehicle repair costs, and legal settlements can exceed minimum limits. Drivers should consider their financial situation and potential liability when choosing coverage levels.

Auto insurance should be viewed as protection against significant financial risk, not merely a legal obligation.

The Role of Technology in Auto Insurance

Technology has significantly influenced auto insurance. Many insurers now offer digital platforms for:

- Policy management

- Claims submission

- Coverage adjustments

Usage-based insurance programs use telematics to monitor driving behavior and adjust premiums accordingly. While these programs may offer cost benefits, they also involve data-sharing considerations.

Technology has improved efficiency and transparency, making auto insurance more accessible and easier to manage.

Why Auto Insurance Is a Long-Term Responsibility

Driving carries ongoing risk. Even experienced drivers can encounter unexpected situations due to weather, road conditions, or the behavior of others.

Auto insurance provides stability in an environment where accidents are unpredictable. Responsible coverage ensures that a single incident does not result in long-term financial hardship.

Conclusion

Auto insurance is a fundamental part of responsible vehicle ownership in the United States. It protects drivers from financial and legal consequences arising from accidents, theft, and other risks.

Understanding liability coverage, collision and comprehensive options, deductibles, and coverage limits allows drivers to make informed choices rather than focusing solely on price.

When chosen thoughtfully, auto insurance serves not just as a legal requirement, but as a critical tool for financial protection and peace of mind.