The insurance industry is undergoing a significant transformation. With the rise of technology, digital insurance has emerged as an alternative to traditional insurance models.

While both aim to provide financial protection, they differ in how they operate, how policies are managed, and how customers interact with providers.

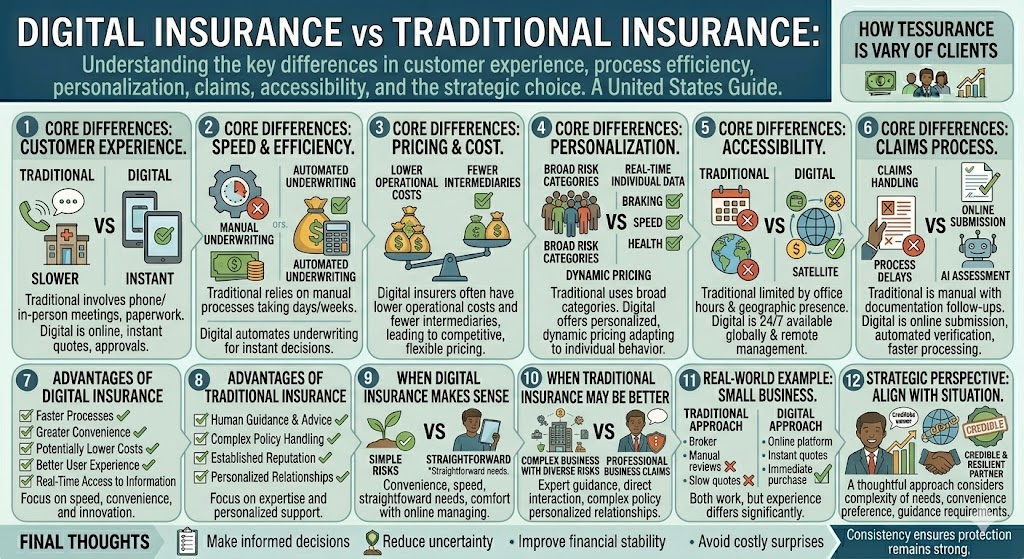

Understanding the key differences between digital insurance and traditional insurance can help you make better decisions when choosing coverage.

This article is for informational purposes only and does not constitute financial or insurance advice.

What Is Traditional Insurance?

Traditional insurance refers to the conventional model where policies are:

- Sold through agents or brokers

- Managed through physical offices or call centers

- Based on standardized processes

- Often reliant on manual underwriting

This model has been used for decades and remains widely adopted.

What Is Digital Insurance?

Digital insurance uses technology to streamline and automate insurance processes.

This includes:

- Online policy purchase

- Automated underwriting

- Mobile apps and digital dashboards

- AI-driven risk assessment

Digital insurance platforms are often associated with “insurtech” companies.

Core Differences Between Digital and Traditional Insurance

1. Customer Experience

Traditional Insurance:

- Requires phone calls or in-person meetings

- Slower response times

- More paperwork

Digital Insurance:

- Fully online experience

- Instant quotes and approvals

- Easy policy management through apps

Digital platforms prioritize convenience and speed.

2. Speed and Efficiency

Traditional processes can take:

- Days or weeks for approval

- Manual review of applications

Digital insurance can:

- Provide instant quotes

- Automate underwriting

- Reduce processing time significantly

3. Pricing and Cost Structure

Digital insurers often have:

- Lower operational costs

- Fewer intermediaries

This can lead to:

- More competitive pricing

- More flexible pricing models

However, pricing still depends on risk assessment.

4. Personalization

Traditional insurance:

- Uses broader risk categories

- Less dynamic pricing

Digital insurance:

- Uses real-time data

- Offers personalized pricing

- Adapts to individual behavior

This is especially visible in areas like auto or health insurance.

5. Accessibility

Traditional insurance may be limited by:

- Office hours

- Geographic presence

Digital insurance:

- Available 24/7

- Accessible from anywhere

- Easy to manage remotely

6. Claims Process

Traditional Insurance:

- Often manual

- Requires documentation and follow-ups

- Slower processing

Digital Insurance:

- Online claims submission

- Automated verification

- Faster processing times

Some platforms even use AI to assess claims.

7. Transparency

Digital platforms often provide:

- Clear dashboards

- Easy access to policy details

- Real-time updates

Traditional models may rely more on:

- Documents

- Customer service interactions

8. Human Interaction

Traditional insurance offers:

- Direct contact with agents

- Personalized advice

Digital insurance:

- Limited human interaction

- More self-service tools

This can be a benefit or drawback depending on user preference.

Advantages of Digital Insurance

- Faster processes

- Greater convenience

- Potentially lower costs

- Better user experience

- Real-time access to information

Advantages of Traditional Insurance

- Human guidance and advice

- More complex policy handling

- Established reputation

- Personalized relationships

When Digital Insurance Makes More Sense

Digital insurance may be ideal if:

- You prefer convenience and speed

- Your insurance needs are straightforward

- You are comfortable managing policies online

When Traditional Insurance May Be Better

Traditional insurance may be preferable if:

- Your situation is complex

- You need expert guidance

- You value personal interaction

Real-World Example

Consider a small business owner looking for liability insurance.

Traditional approach:

- Contact broker

- Review options manually

- Wait for quotes

Digital approach:

- Use online platform

- Get instant quotes

- Purchase coverage immediately

Both approaches work — but the experience differs significantly.

Challenges of Digital Insurance

Despite its advantages, digital insurance has limitations.

1. Limited Human Support

Not all situations can be easily handled without expert advice.

2. Complexity in Advanced Cases

Complex policies may still require traditional expertise.

3. Data Privacy Concerns

Digital platforms rely heavily on data, raising privacy considerations.

4. Trust and Familiarity

Some users may prefer established, traditional providers.

The Future: A Hybrid Model

The future of insurance is likely a combination of both models.

We are already seeing:

- Traditional insurers adopting digital tools

- Digital platforms adding human support

This hybrid approach aims to combine:

- Efficiency of technology

- Value of human expertise

The Strategic Perspective

Choosing between digital and traditional insurance is not about which is better — it is about which is more appropriate for your situation.

A strategic approach considers:

- Complexity of your needs

- Preference for convenience vs guidance

- Risk profile

- Level of involvement you want

Final Thoughts

Digital insurance and traditional insurance serve the same purpose but operate in very different ways.

Digital insurance offers speed, convenience, and innovation, while traditional insurance provides human expertise and personalized support.

Understanding these differences helps you choose the approach that best fits your needs.

As technology continues to evolve, the gap between the two models will likely narrow — creating more flexible and efficient insurance solutions.