Insurance pricing is often perceived as a simple calculation based on age, location, or type of coverage. However, behind every premium lies a complex system of risk evaluation, data analysis, and financial modeling.

Understanding how insurance pricing really works can help individuals and business owners make more informed decisions — not just about cost, but about the structure of their protection.

This guide explains the key mechanisms insurers use behind the scenes to determine pricing in the United States.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

The Core Principle: Risk Assessment

At its foundation, insurance pricing is based on one concept: risk.

Insurance companies evaluate:

- The probability of a claim occurring

- The potential cost of that claim

- The overall exposure across a group of policyholders

The goal is not to predict individual outcomes with certainty, but to estimate risk across large groups.

This process is known as risk pooling — where many policyholders share the financial impact of relatively few claims.

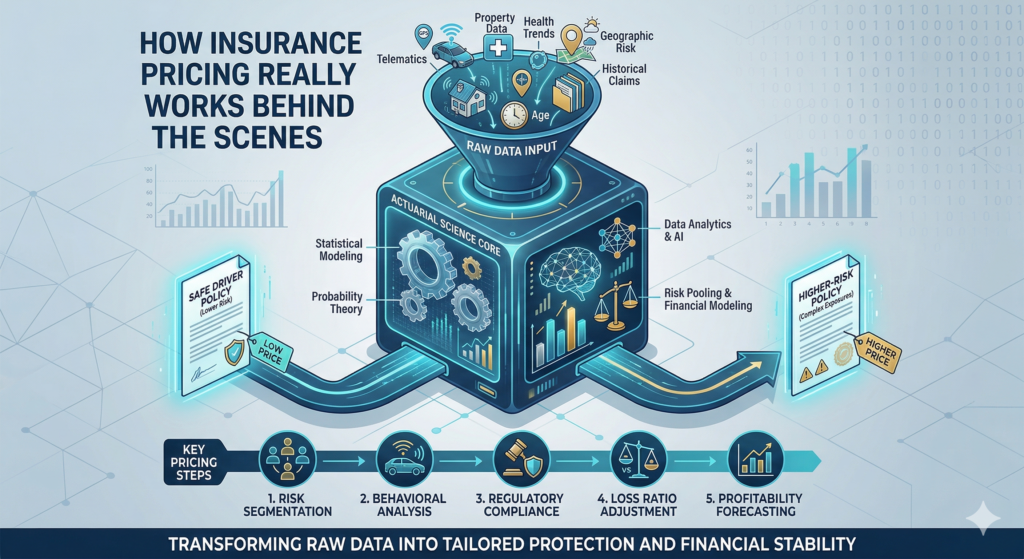

Actuarial Science: The Engine Behind Pricing

Insurance pricing relies heavily on actuarial science.

Actuaries use:

- Statistical models

- Historical data

- Probability theory

- Financial forecasting

They analyze patterns such as:

- Accident frequency

- Health trends

- Property damage rates

- Legal claim costs

These insights help insurers estimate expected losses and determine appropriate premium levels.

Actuarial models are continuously updated as new data becomes available.

Key Factors That Influence Insurance Pricing

While every policy is unique, most pricing models consider several core variables.

1. Personal and Demographic Factors

For individual policies, insurers may evaluate:

- Age

- Gender (where permitted by law)

- Location

- Occupation

- Lifestyle factors

These variables are used to estimate general risk patterns across populations.

2. Historical Data and Claims Experience

Past behavior is one of the strongest indicators used in pricing.

Insurers analyze:

- Previous claims history

- Frequency of claims

- Severity of past losses

For example, a history of frequent claims may increase perceived risk.

3. Type and Scope of Coverage

The structure of the policy directly affects pricing.

Important elements include:

- Coverage limits

- Deductibles

- Type of policy (auto, home, business, etc.)

- Optional endorsements

Higher coverage limits typically increase premiums, while higher deductibles may reduce them.

4. Geographic Risk

Location plays a significant role.

Examples:

- Areas with high accident rates may increase auto premiums

- Regions prone to natural disasters may affect property insurance

- Urban vs rural environments may impact risk exposure

Geographic data helps insurers adjust pricing based on environmental risk factors.

The Role of Data and Technology

Modern insurance pricing is increasingly driven by advanced data analytics.

Insurers may use:

- Machine learning models

- Real-time behavioral data

- Telematics (in auto insurance)

- Property sensors

- Credit-based insurance scores (where permitted)

For example, telematics programs can track driving behavior such as:

- Speed patterns

- Braking habits

- Mileage

This allows pricing to reflect actual behavior rather than general assumptions.

Loss Ratios and Profitability

Insurance companies must balance risk with financial sustainability.

One key metric is the loss ratio, which compares:

- Claims paid

- Premiums collected

If claims significantly exceed premiums, the insurer operates at a loss.

Pricing models aim to maintain balance by:

- Covering expected claims

- Supporting operational costs

- Maintaining financial reserves

This is why pricing may change over time — not just for individuals, but across entire markets.

Why Prices Change Over Time

Insurance premiums are not static.

They may change due to:

- Inflation and rising repair costs

- Increased frequency of claims

- Legal and regulatory changes

- Climate-related risks

- Market competition

Even if an individual’s profile remains the same, broader trends can influence pricing.

Risk Segmentation: Grouping Policyholders

Insurers do not price each policy entirely individually.

Instead, they group policyholders into categories based on shared characteristics.

This process is called risk segmentation.

Examples of segments:

- Safe vs high-risk drivers

- Low-risk vs high-risk properties

- Industry classifications for businesses

Segmenting allows insurers to price coverage more accurately across groups.

Behavioral Pricing and Usage-Based Models

In recent years, insurance pricing has become more personalized.

Usage-based insurance models allow pricing based on real-world behavior.

Examples include:

- Pay-per-mile auto insurance

- Driving behavior tracking

- On-demand coverage for short-term needs

These models may offer more flexibility but also rely on increased data collection.

The Impact of Regulation

Insurance pricing in the United States is regulated at the state level.

Regulators review pricing models to ensure they are:

- Not discriminatory

- Actuarially justified

- Transparent

- Compliant with consumer protection laws

This oversight helps maintain fairness while allowing insurers to manage risk.

Common Misunderstandings About Insurance Pricing

Misconception 1: “Prices Are Arbitrary”

Insurance pricing is data-driven and based on structured models, not random decisions.

Misconception 2: “Loyal Customers Always Get Better Rates”

In some cases, market conditions or updated risk models may result in pricing changes over time.

Misconception 3: “Cheaper Always Means Better”

Lower premiums may reflect reduced coverage, higher deductibles, or narrower protection.

Understanding policy structure is as important as comparing price.

How to Evaluate Insurance Pricing as a Consumer

Instead of focusing only on cost, consider:

- Coverage limits

- Deductible levels

- Policy exclusions

- Claim handling reputation

- Financial strength of the insurer

A lower premium may not always represent better value if coverage is insufficient.

Real-World Example

Two individuals may receive different auto insurance quotes for similar vehicles.

Why?

Because pricing may reflect:

- Driving history

- Location

- Credit-based factors (where allowed)

- Annual mileage

- Coverage choices

Even small differences can influence pricing outcomes.

The Bigger Picture: Insurance as a System

Insurance pricing is not just about individual policies.

It is part of a larger system that balances:

- Risk distribution

- Financial sustainability

- Consumer protection

- Market competition

Understanding this system helps explain why premiums vary and evolve.

Final Thoughts

Insurance pricing is a complex process driven by data, risk modeling, and financial strategy.

While premiums may seem simple on the surface, they reflect a combination of actuarial analysis, behavioral data, geographic risk, and regulatory oversight.

For consumers and business owners, the key is not just to find the lowest price — but to understand what that price represents.

A well-informed approach to insurance pricing supports better decisions, stronger protection, and long-term financial stability.