Insurance is not something you set once and forget. As your life, finances, or business evolve, your insurance policies should evolve as well.

However, many individuals and business owners fail to review their policies regularly. This can lead to outdated coverage, unnecessary costs, or gaps in protection that only become visible when a claim occurs.

Understanding how often you should review your insurance policies — and what to look for during that process — is essential for maintaining effective and efficient protection.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

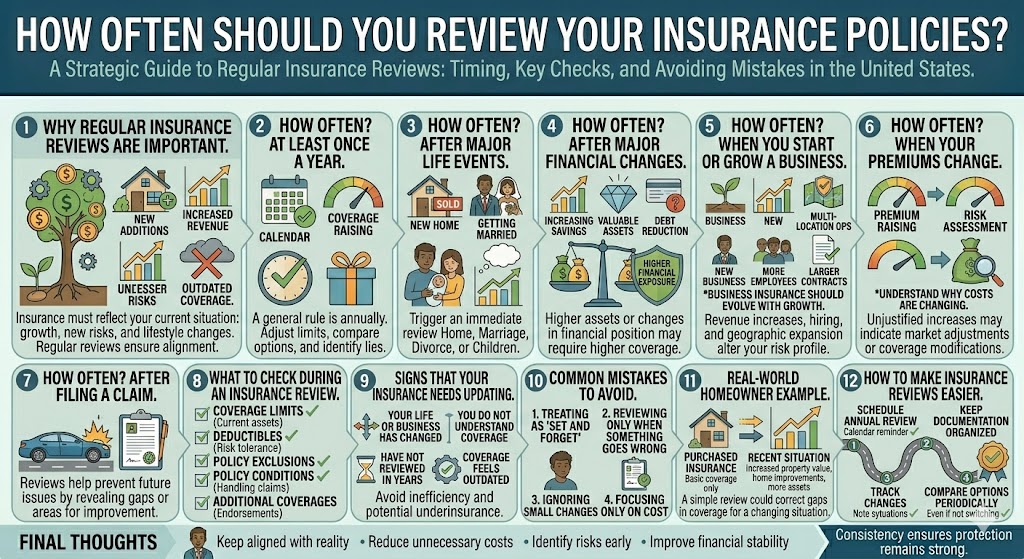

Why Regular Insurance Reviews Are Important

Insurance is designed to reflect your current situation.

Over time, changes may include:

- Increased income or assets

- Business growth

- New risks or exposures

- Changes in regulations

- Lifestyle changes

If your policy does not keep up with these changes, it may no longer provide adequate protection.

Regular reviews help ensure that your coverage stays aligned with reality.

How Often Should You Review Your Insurance Policies?

1. At Least Once a Year

A general rule is to review your policies annually.

This allows you to:

- Adjust coverage limits

- Identify unnecessary costs

- Compare with other options

- Ensure everything is up to date

Annual reviews provide a structured way to stay in control.

2. After Major Life Events

Certain life events should trigger an immediate review.

Examples include:

- Buying a home

- Getting married or divorced

- Having children

- Significant income changes

These events can significantly affect your insurance needs.

3. After Major Financial Changes

Changes in financial position often require adjustments.

This may include:

- Increased savings or investments

- New assets

- Debt changes

Higher financial exposure may require higher coverage.

4. When You Start or Grow a Business

Business-related changes can quickly alter your risk profile.

Review your insurance if:

- You launch a new business

- Revenue increases

- You hire employees

- You expand operations

Business insurance should evolve with growth.

5. When Your Premiums Change

A noticeable increase in premiums is a good reason to review your policy.

This may indicate:

- Changes in risk assessment

- Market adjustments

- Coverage modifications

It is important to understand why costs are changing.

6. After Filing a Claim

A claim can reveal:

- Coverage gaps

- Policy limitations

- Areas where protection can improve

Reviewing your policy after a claim helps prevent future issues.

What to Check During an Insurance Review

1. Coverage Limits

Ensure that your limits reflect:

- Current assets

- Income level

- Business exposure

Low limits may lead to underinsurance.

2. Deductibles

Evaluate whether your deductible:

- Matches your financial capacity

- Aligns with your risk tolerance

Adjusting deductibles can optimize cost vs protection.

3. Policy Exclusions

Exclusions define what is not covered.

Review them carefully to avoid surprises.

4. Policy Conditions

Conditions affect how claims are handled.

Check:

- Reporting requirements

- Documentation needs

- Compliance obligations

5. Additional Coverages

Consider whether you need:

- New endorsements

- Additional policies

- Expanded protection

Signs That Your Insurance Needs Updating

1. Your Life or Business Has Changed

Any major change may require a policy update.

2. You Do Not Fully Understand Your Coverage

If you are unsure what your policy includes, it may need review.

3. You Have Not Reviewed It in Years

Long periods without review often lead to inefficiencies.

4. Your Coverage Feels Outdated

Policies should reflect current risks, not past situations.

Real-World Example

Consider a homeowner who purchased insurance several years ago.

Since then:

- Property value increased

- Home improvements were made

- Personal assets grew

Without reviewing the policy:

- Coverage limits may be too low

- Certain improvements may not be covered

A simple review could correct these gaps.

Common Mistakes to Avoid

1. Treating Insurance as “Set and Forget”

This is one of the most common mistakes.

2. Reviewing Only When Something Goes Wrong

Waiting until a claim occurs is too late.

3. Ignoring Small Changes

Small changes over time can create significant mismatches.

4. Focusing Only on Cost

Reviews should consider both cost and protection.

The Strategic Perspective

Regular insurance reviews are not just about maintenance — they are about optimization.

They help:

- Keep coverage aligned with reality

- Reduce unnecessary costs

- Identify risks early

- Improve long-term financial stability

For businesses, regular reviews are also part of professional risk management.

How to Make Insurance Reviews Easier

1. Schedule Annual Reviews

Set a reminder once a year.

2. Keep Documentation Organized

Having all policies in one place simplifies the process.

3. Track Changes in Your Situation

Note any major changes that may affect coverage.

4. Compare Options Periodically

Even if you do not switch providers, comparing helps ensure competitiveness.

Final Thoughts

Insurance policies should evolve alongside your life and business.

Reviewing them regularly helps ensure that your coverage remains relevant, efficient, and effective.

A proactive approach to insurance reviews can prevent gaps, reduce unnecessary costs, and improve overall protection.

Rather than treating insurance as a static decision, it should be viewed as an ongoing process — one that supports your long-term financial and operational goals.