Comparing insurance quotes is one of the most important steps when choosing coverage. However, many people focus only on price — and that is where mistakes happen.

A lower premium does not always mean better value. In some cases, it may indicate less coverage, higher deductibles, or important exclusions that only become clear when a claim is filed.

Understanding how to compare insurance quotes the right way helps ensure that you are not just saving money, but also protecting yourself effectively.

This guide explains how to evaluate insurance quotes properly so you can make informed and confident decisions.

This article is for informational purposes only and does not constitute financial or insurance advice.

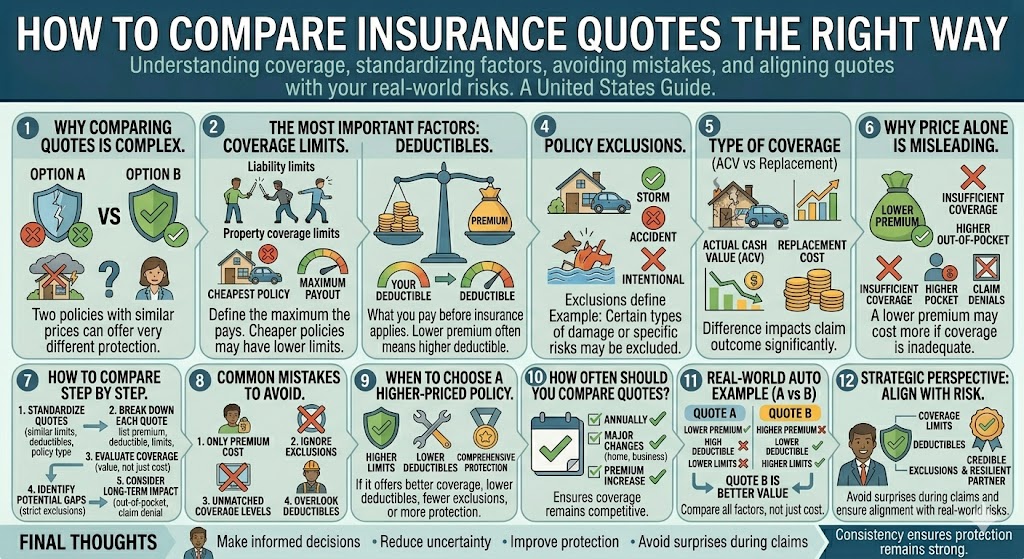

Why Comparing Insurance Quotes Is More Complex Than It Seems

At first glance, comparing quotes appears simple:

- Option A costs less

- Option B costs more

But insurance is not a standardized product.

Each quote may differ in:

- Coverage limits

- Deductibles

- Exclusions

- Policy conditions

Two policies with similar prices can offer very different levels of protection.

The Most Important Factors to Compare

1. Coverage Limits

Coverage limits define the maximum amount the insurer will pay.

When comparing quotes, check:

- Liability limits

- Property coverage limits

- Total maximum payouts

A cheaper policy may have lower limits, which could leave you exposed.

2. Deductibles

The deductible is what you pay out of pocket before insurance applies.

Compare:

- Deductible amounts

- How they affect premiums

A lower premium often comes with a higher deductible.

3. Policy Exclusions

Exclusions are one of the most overlooked aspects.

They define what is NOT covered.

Examples may include:

- Certain types of damage

- Specific risks

- Gradual vs sudden events

Always review exclusions carefully.

4. Type of Coverage (Actual Cash Value vs Replacement Cost)

Policies may differ in how they calculate payouts.

- Actual Cash Value (ACV): depreciated value

- Replacement Cost: cost to replace without depreciation

This difference can significantly impact claim outcomes.

5. Policy Conditions

Conditions define how the policy works.

This may include:

- Reporting requirements

- Claim procedures

- Maintenance responsibilities

Ignoring these details can lead to unexpected issues.

6. Additional Coverages and Endorsements

Some policies include optional add-ons.

These may cover:

- Specific risks

- Higher-value items

- Additional protection layers

Make sure you understand what is included — and what is not.

Why Price Alone Is Misleading

Choosing insurance based only on price can lead to:

- Insufficient coverage

- Higher out-of-pocket costs

- Claim denials due to exclusions

A lower premium may actually cost more in the long run if coverage is inadequate.

How to Compare Quotes Step by Step

Step 1: Standardize What You Are Comparing

Ensure that all quotes are based on:

- Similar coverage limits

- Similar deductibles

- Same type of policy

Without this, comparisons are not meaningful.

Step 2: Break Down Each Quote

List key elements for each option:

- Premium

- Deductible

- Coverage limits

- Exclusions

This helps identify differences clearly.

Step 3: Evaluate Coverage vs Cost

Ask:

- What am I getting for this price?

- Where are the differences?

Focus on value, not just cost.

Step 4: Identify Potential Gaps

Look for areas where coverage may be lacking.

Examples:

- Low liability limits

- Missing coverage types

- Strict exclusions

Step 5: Consider Long-Term Impact

Think beyond the premium:

- What happens if I file a claim?

- How much would I pay out of pocket?

This perspective is essential.

Real-World Example

Imagine two auto insurance quotes:

Quote A:

- Lower premium

- High deductible

- Lower liability limits

Quote B:

- Slightly higher premium

- Lower deductible

- Higher liability limits

At first glance, Quote A seems better.

However:

- In case of an accident, out-of-pocket costs may be higher

- Liability protection may be insufficient

In this scenario, Quote B may offer better overall value.

Common Mistakes When Comparing Insurance Quotes

1. Looking Only at the Premium

This is the most common mistake.

2. Ignoring Exclusions

Exclusions can significantly affect coverage.

3. Not Matching Coverage Levels

Comparing different levels of coverage leads to incorrect conclusions.

4. Overlooking Deductibles

Higher deductibles can offset lower premiums.

5. Not Reading Policy Details

Important differences are often found in the fine print.

When It Makes Sense to Choose a Higher-Priced Policy

A higher-priced policy may be justified if it offers:

- Better coverage limits

- Lower deductibles

- Fewer exclusions

- More comprehensive protection

The goal is not to choose the cheapest option, but the most efficient one.

How Often Should You Compare Insurance Quotes?

It is generally a good idea to compare quotes:

- Once a year

- After major life or business changes

- When premiums increase

Regular comparison helps ensure that your coverage remains competitive.

The Strategic Perspective

Comparing insurance quotes is not just about shopping — it is about decision-making.

A well-informed comparison helps:

- Optimize cost

- Improve protection

- Avoid surprises during claims

For businesses, it can also impact financial stability and risk management.

Final Thoughts

Insurance is not a one-size-fits-all product, and comparing quotes requires more than looking at price.

By evaluating coverage limits, deductibles, exclusions, and policy structure, you can make smarter decisions that balance cost and protection.

Taking the time to compare quotes the right way ensures that your insurance works when you need it — not just when you buy it.

In the long run, informed decisions lead to better protection and greater financial confidence.