Insurance is essential for financial protection, but it can also represent a significant ongoing expense. For individuals and businesses alike, the challenge is not just finding coverage — it is finding the right balance between cost and protection.

Many people assume that lowering insurance costs means sacrificing coverage. In reality, there are strategic ways to reduce premiums while maintaining — or even improving — your level of protection.

Understanding how to lower insurance costs without reducing protection allows you to optimize your policies and make smarter financial decisions.

This article is for informational purposes only and does not constitute financial or insurance advice.

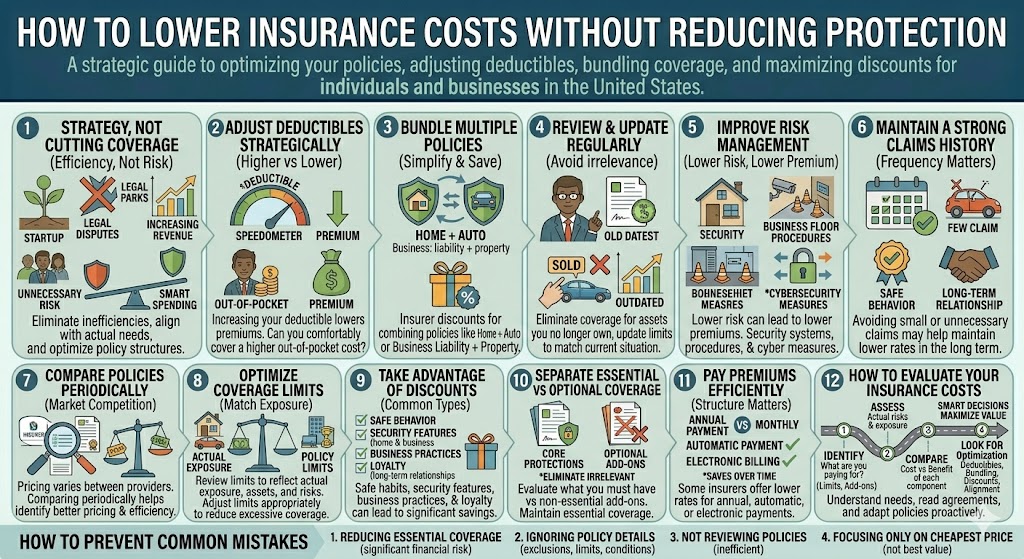

Why Lowering Insurance Costs Is About Strategy, Not Cutting Coverage

Reducing insurance costs should not mean exposing yourself to unnecessary risk.

Instead, the goal is to:

- Eliminate inefficiencies

- Align coverage with actual needs

- Avoid overpaying for unnecessary features

- Optimize how policies are structured

In many cases, people pay more than necessary simply because they have not reviewed their policies.

The Most Effective Ways to Lower Insurance Costs

1. Adjust Your Deductible Strategically

One of the most effective ways to reduce premiums is by increasing your deductible.

- Higher deductible → lower premium

- Lower deductible → higher premium

If you can comfortably cover a higher out-of-pocket cost in case of a claim, this adjustment can significantly reduce ongoing expenses.

However, this should be done carefully to avoid financial strain during unexpected events.

2. Bundle Multiple Policies

Many insurers offer discounts when you combine policies.

Examples include:

- Home + auto insurance

- Business liability + property coverage

Bundling can simplify management and reduce overall costs without changing coverage levels.

3. Review and Update Your Coverage Regularly

Outdated policies often include:

- Coverage for assets you no longer own

- Limits that no longer match your situation

- Unnecessary add-ons

A regular review helps ensure that you are not paying for irrelevant coverage.

4. Improve Risk Management

Lower risk can lead to lower premiums.

Examples include:

- Installing security systems

- Implementing safety procedures in a business

- Using cybersecurity measures

Insurers may offer better pricing for lower-risk profiles.

5. Maintain a Strong Claims History

Frequent claims can increase premiums over time.

While insurance should be used when needed, avoiding small or unnecessary claims may help maintain lower rates in the long term.

6. Compare Policies Periodically

Insurance pricing can vary between providers.

Comparing options allows you to:

- Identify better pricing

- Find more efficient coverage structures

- Adjust policies based on current market conditions

This does not mean switching frequently, but periodic comparison is valuable.

7. Optimize Coverage Limits

Having insufficient coverage is risky — but excessive coverage can be inefficient.

Review whether your policy limits:

- Reflect your actual exposure

- Align with your assets and risks

Adjusting limits appropriately can reduce costs without reducing meaningful protection.

8. Take Advantage of Discounts

Many insurers offer discounts based on:

- Safe behavior (e.g., driving history)

- Security features

- Business practices

- Loyalty or long-term relationships

Understanding available discounts can help reduce premiums.

9. Separate Essential vs Optional Coverage

Not all policy features are equally important.

Evaluate:

- Core protections you must have

- Optional add-ons that may not be necessary

This helps eliminate unnecessary costs while maintaining essential coverage.

10. Pay Premiums Efficiently

Payment structure can affect cost.

Some insurers offer lower rates for:

- Annual payments vs monthly

- Automatic payments

- Electronic billing

While the difference may seem small, it can add up over time.

Real-World Example

Consider a homeowner with a long-standing insurance policy.

Over time:

- The value of certain assets decreases

- Security improvements are made

- Risk exposure changes

By reviewing the policy:

- Deductible is adjusted

- Unnecessary coverage is removed

- Discounts are applied

The result:

- Lower premium

- Same (or better) effective protection

This demonstrates how optimization — not reduction — leads to savings.

Common Mistakes to Avoid

1. Reducing Coverage to Save Money

Cutting essential coverage may create significant financial risk.

2. Ignoring Policy Details

Not understanding exclusions, limits, or conditions can lead to poor decisions.

3. Not Reviewing Policies Over Time

Static policies often become inefficient.

4. Focusing Only on Price

The cheapest policy is not always the best value.

How to Evaluate Your Current Insurance Costs

1. Identify What You Are Paying For

Break down:

- Coverage types

- Limits

- Add-ons

2. Assess Your Actual Risk

Ask:

- What risks do I realistically face?

3. Compare Cost vs Benefit

Evaluate whether each component of your policy provides meaningful value.

4. Look for Optimization Opportunities

Focus on:

- Deductibles

- Bundling

- Discounts

- Coverage alignment

The Strategic Perspective

Lowering insurance costs is not about spending less — it is about spending smarter.

Efficient insurance structures:

- Reduce unnecessary expenses

- Maintain strong protection

- Adapt to changing circumstances

For businesses, this can improve profitability. For individuals, it can support long-term financial stability.

Final Thoughts

Insurance is a critical part of financial protection, but it does not have to be inefficient or overly expensive.

By taking a strategic approach — adjusting deductibles, reviewing coverage, improving risk management, and exploring discounts — it is possible to lower costs without reducing protection.

The key is understanding your needs and aligning your policies accordingly.

Smart insurance decisions are not about minimizing cost at all costs, but about maximizing value.