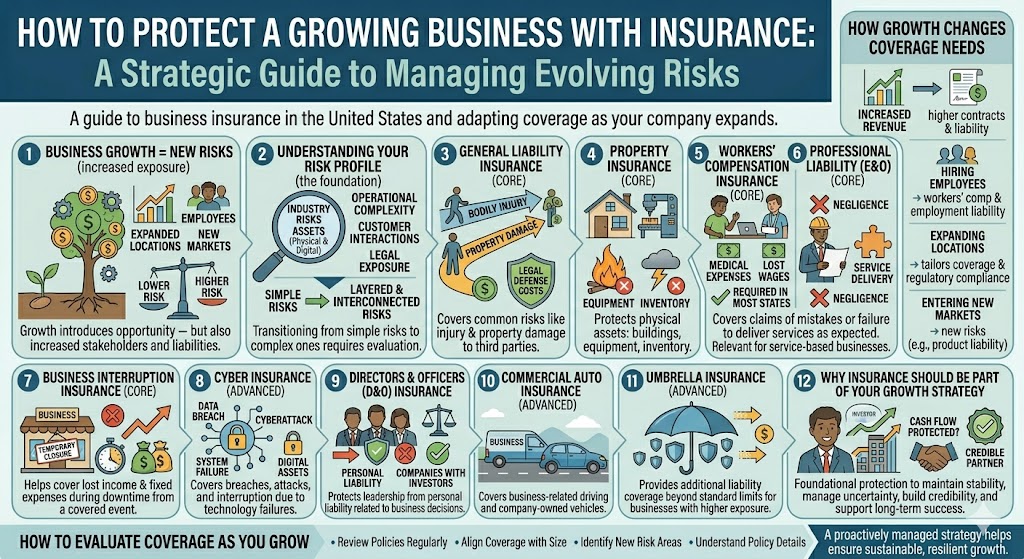

As a business grows, its risks evolve. What may have started as a small operation with limited exposure can quickly expand into a more complex structure with financial, legal, and operational risks.

Insurance plays a critical role in protecting that growth. However, many business owners underestimate how their coverage needs change over time.

Understanding how to protect a growing business with insurance is essential for maintaining stability, managing risk, and supporting long-term success.

This guide explains the key considerations for business insurance in the United States and how coverage should adapt as your company expands.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

Why Growing Businesses Face New Risks

Growth introduces opportunity — but also increased exposure.

As a business expands, it may face:

- Higher revenue and financial stakes

- More employees

- Expanded operations

- New locations or markets

- Increased customer interactions

- Greater legal and regulatory responsibilities

Each of these factors can increase risk in different ways.

Insurance must evolve alongside the business.

The Foundation: Understanding Your Risk Profile

Before choosing or updating insurance, it is important to understand your business risk profile.

This includes evaluating:

- Industry-specific risks

- Operational complexity

- Physical and digital assets

- Customer interactions

- Legal exposure

A growing business typically transitions from simple risks to more layered and interconnected ones.

Core Insurance Types for Growing Businesses

While needs vary by industry, several types of insurance form the foundation of business protection.

1. General Liability Insurance

This covers common risks such as:

- Bodily injury claims

- Property damage to third parties

- Legal defense costs

As your business grows and interacts with more customers, exposure increases.

2. Property Insurance

Protects physical assets such as:

- Buildings

- Equipment

- Inventory

Growth often means more assets — and therefore greater potential loss.

3. Workers’ Compensation Insurance

Required in most states for businesses with employees.

Covers:

- Workplace injuries

- Medical expenses

- Lost wages

As your workforce expands, this becomes increasingly important.

4. Professional Liability Insurance

Also known as errors and omissions (E&O) insurance.

Covers:

- Claims of negligence

- Professional mistakes

- Failure to deliver services as expected

Particularly relevant for service-based businesses.

5. Business Interruption Insurance

Helps cover lost income if operations are disrupted due to a covered event.

This may include:

- Temporary closure

- Reduced operations

- Fixed expenses during downtime

For growing businesses, interruptions can have a larger financial impact.

Advanced Coverage for Expanding Businesses

As your business becomes more complex, additional coverage types may be necessary.

1. Cyber Insurance

With increased reliance on technology, businesses face digital risks.

Cyber insurance may cover:

- Data breaches

- Cyberattacks

- Business interruption due to system failures

This is especially relevant for tech-driven or online businesses.

2. Directors and Officers (D&O) Insurance

Protects company leadership from personal liability related to business decisions.

Important for:

- Companies with investors

- Rapidly scaling startups

- Businesses with formal governance structures

3. Commercial Auto Insurance

If your business uses vehicles for operations, personal auto policies may not apply.

Commercial policies cover:

- Business-related driving

- Company-owned vehicles

4. Umbrella Insurance

Provides additional liability coverage beyond standard policy limits.

Useful for businesses with:

- Higher exposure

- Larger contracts

- Increased legal risk

How Growth Changes Insurance Needs

1. Increased Revenue = Increased Risk

Higher revenue often means:

- Larger contracts

- Greater liability

- Higher expectations

Coverage limits should reflect this.

2. Hiring Employees

Expanding your team introduces:

- Workplace injury risk

- Employment-related liability

- Compliance requirements

Insurance must adapt accordingly.

3. Expanding Locations

Operating in multiple locations may introduce:

- Different regulatory requirements

- New environmental risks

- Additional property exposure

Each location may require tailored coverage.

4. Entering New Markets

New products or services can create new types of risk.

Examples:

- Product liability

- Professional liability

- Regulatory compliance

Coverage should reflect these changes.

Common Mistakes Growing Businesses Make

1. Keeping the Same Coverage as When Starting

Many businesses fail to update policies as they grow.

This can lead to underinsurance.

2. Underestimating Liability Risk

As visibility increases, so does exposure to legal claims.

3. Ignoring Digital Risks

Cyber threats are often overlooked until an incident occurs.

4. Focusing Only on Cost

Choosing lower premiums may reduce protection.

Balance is essential.

How to Evaluate Your Coverage as You Grow

1. Review Policies Regularly

Coverage should be reviewed at least annually or after major changes.

2. Align Coverage with Business Size

Ensure policy limits reflect current operations and revenue.

3. Identify New Risk Areas

Growth often introduces risks that were not present before.

4. Understand Policy Details

Review:

- Exclusions

- Limits

- Conditions

These details affect real-world outcomes.

Real-World Example

Consider a small online business that expands into a larger e-commerce operation.

Initially, it may only require basic liability coverage.

As it grows:

- It stores customer data → cyber risk increases

- It ships products → product liability becomes relevant

- Revenue increases → higher financial exposure

Without updated coverage, the business may face significant risk gaps.

The Role of Technology in Business Insurance

Modern insurance solutions are evolving alongside business growth.

Many insurers now offer:

- Digital policy management

- Real-time risk assessment

- Usage-based pricing models

- Data-driven insights

These tools can help businesses adapt coverage more efficiently.

Why Insurance Should Be Part of Your Growth Strategy

Insurance is often seen as a cost, but it also serves as a strategic asset.

It helps:

- Protect cash flow

- Reduce uncertainty

- Support long-term planning

- Build credibility with partners and investors

For growing businesses, protection is not optional — it is foundational.

Final Thoughts

Protecting a growing business with insurance requires more than simply maintaining existing policies.

As your business evolves, so do your risks. Coverage must adapt to reflect changes in operations, revenue, workforce, and market exposure.

A proactive approach to insurance helps ensure that growth is supported by adequate protection — not undermined by unseen risks.

Understanding your coverage and reviewing it regularly is key to building a resilient and sustainable business.