Car accidents are stressful and often unexpected. In the moments following a collision, it can be difficult to know what to do — especially when it comes to insurance.

Understanding what happens after a car accident, step by step, can help reduce confusion and ensure that you handle the situation correctly. It also increases the likelihood that your insurance claim is processed smoothly.

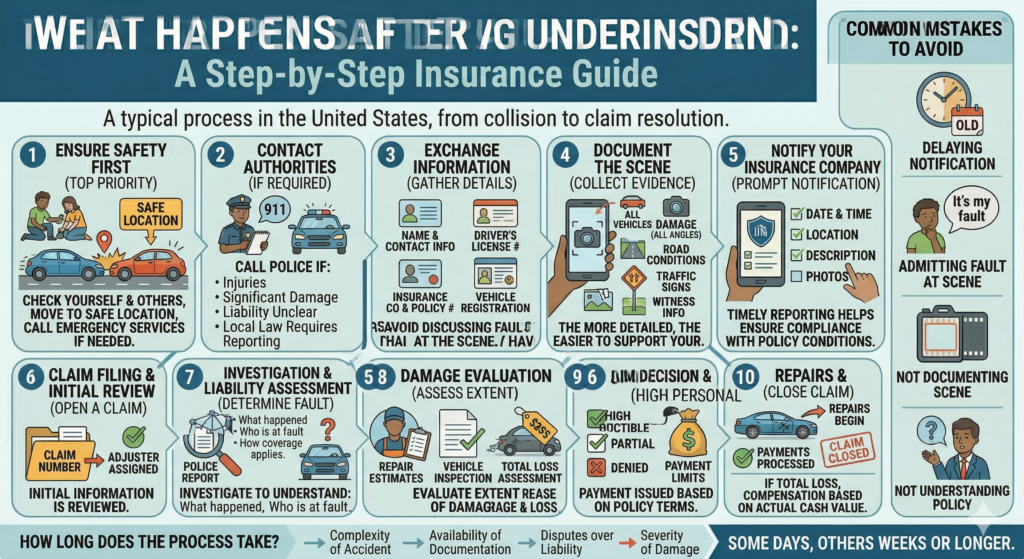

This guide explains the typical process in the United States, from the moment the accident occurs to the resolution of an insurance claim.

This article is for informational purposes only and does not constitute legal or insurance advice.

Step 1: Ensure Safety First

Immediately after an accident, safety is the top priority.

You should:

- Check yourself and others for injuries

- Move vehicles to a safe location if possible

- Turn on hazard lights

- Call emergency services if needed

Even in minor accidents, staying calm and focused is essential.

Step 2: Contact Authorities (If Required)

In many situations, calling the police is recommended or required.

This is especially important if:

- There are injuries

- There is significant vehicle damage

- Liability is unclear

- Local laws require reporting

A police report can serve as an official record, which may be important during the insurance process.

Step 3: Exchange Information

You should exchange information with all involved parties.

This typically includes:

- Full name and contact details

- Driver’s license number

- Insurance company and policy number

- Vehicle registration details

Avoid discussing fault at the scene. The goal is to gather accurate information, not assign responsibility.

Step 4: Document the Scene

Proper documentation can significantly impact your insurance claim.

Consider collecting:

- Photos of all vehicles involved

- Images of damage from multiple angles

- Road conditions and surroundings

- Traffic signs or signals

- Witness contact information (if available)

The more detailed your documentation, the easier it is to support your claim.

Step 5: Notify Your Insurance Company

Most insurance policies require prompt notification after an accident.

When contacting your insurer, be prepared to provide:

- Date, time, and location of the accident

- Description of what happened

- Information about other parties involved

- Photos or documentation

Timely reporting helps ensure compliance with policy conditions.

Step 6: Claim Filing and Initial Review

After notification, the insurance company will open a claim.

At this stage:

- A claim number is assigned

- An adjuster may be assigned to your case

- Initial information is reviewed

The insurer may request additional documentation or clarification.

Step 7: Investigation and Liability Assessment

The insurance company will investigate the accident to determine:

- What happened

- Who may be at fault

- How coverage applies

This process may involve:

- Reviewing police reports

- Examining photos and evidence

- Speaking with drivers and witnesses

- Analyzing damage patterns

Liability determination can affect how claims are handled and paid.

Step 8: Damage Evaluation

Next, the insurer evaluates the extent of damage.

This may include:

- Vehicle inspection

- Repair estimates

- Assessment of total loss (if applicable)

In some cases, policyholders may choose repair shops, while in others the insurer may recommend options.

Step 9: Claim Decision and Payment

Once the evaluation is complete, the insurer makes a decision.

Possible outcomes include:

- Approval of the claim

- Partial coverage based on policy terms

- Denial if exclusions apply

If approved, payment is issued according to:

- Coverage limits

- Deductible amounts

- Policy conditions

Step 10: Repairs and Resolution

After claim approval:

- Repairs may begin

- Payments are processed

- The claim is eventually closed

If the vehicle is declared a total loss, compensation may be based on its actual cash value.

Understanding Deductibles

Most auto insurance policies include a deductible.

This is the amount you pay out of pocket before insurance coverage applies.

For example:

- If repairs cost $3,000 and your deductible is $500

- You may pay $500, and insurance may cover the remaining amount (subject to policy terms)

Understanding your deductible is essential before filing a claim.

What If the Other Driver Is at Fault?

If another driver is determined to be at fault:

- Their insurance may cover damages

- Your insurer may coordinate the process

- You may still need to pay your deductible initially (depending on the situation)

Processes vary depending on state laws and policy structure.

What If the Other Driver Is Uninsured?

If the other driver does not have insurance, coverage may depend on your policy.

Some policies include:

- Uninsured motorist coverage

- Underinsured motorist protection

These coverages may help in situations where the at-fault driver lacks sufficient insurance.

How Long Does the Process Take?

The timeline for resolving a claim varies.

Factors include:

- Complexity of the accident

- Availability of documentation

- Disputes over liability

- Severity of damage

Some claims may be resolved in days, while others may take weeks or longer.

Common Mistakes to Avoid After an Accident

1. Delaying Notification

Failing to report the accident promptly may affect your claim.

2. Admitting Fault at the Scene

Determining fault is part of the investigation process.

Avoid making statements that could complicate the claim.

3. Not Documenting the Scene

Lack of evidence can make claims more difficult to process.

4. Not Understanding Your Policy

Coverage limits, deductibles, and exclusions all affect outcomes.

Why Understanding the Process Matters

Knowing what happens after a car accident helps you:

- Respond calmly in stressful situations

- Avoid common mistakes

- Meet policy requirements

- Improve claim outcomes

Insurance is not just about having coverage — it is about understanding how it works when needed.

Final Thoughts

Car accidents can be overwhelming, but the insurance process follows a structured sequence.

From ensuring safety to filing a claim and completing repairs, each step plays a role in how the situation is resolved.

By understanding the process in advance, you can approach it with greater clarity and confidence.

Preparation and awareness are key to navigating insurance effectively after an accident.