Filing an insurance claim is often associated with the expectation of financial support during difficult situations. However, not all claims are approved. In some cases, policyholders receive a denial — which can be confusing and frustrating.

Understanding what to do if your insurance claim is denied is essential. A denial does not always mean the process is over. There are steps you can take to review, respond, and potentially resolve the situation.

This guide explains why claims may be denied and what actions you can take next in the United States.

This article is for informational purposes only and does not constitute legal or insurance advice.

What Does It Mean When a Claim Is Denied?

A claim denial occurs when an insurance company determines that it will not pay for a submitted claim.

This decision is typically based on:

- Policy terms and conditions

- Coverage limitations

- Exclusions

- Documentation provided

A denial is not always final. It reflects the insurer’s evaluation based on available information at that time.

Common Reasons Insurance Claims Are Denied

Understanding why claims are denied is the first step toward responding effectively.

1. The Loss Is Not Covered

One of the most common reasons is that the cause of loss is not included in the policy.

Examples:

- Flood damage under a standard homeowners policy

- Business-related claims under personal coverage

If the event is excluded, the insurer may deny the claim.

2. Policy Exclusions Apply

Even if the type of loss seems covered, exclusions may limit or eliminate coverage.

Examples include:

- Wear and tear

- Intentional damage

- Certain high-risk activities

Exclusions are a key factor in many denials.

3. Missed Deadlines or Policy Conditions

Insurance policies often include strict requirements.

Denials may occur if:

- The claim is reported too late

- Required documentation is not provided

- Policy conditions are not followed

Timeliness and compliance are essential.

4. Insufficient Documentation

A lack of supporting evidence can affect claim outcomes.

Examples:

- Missing photos

- Incomplete reports

- Lack of proof of ownership

Without sufficient documentation, insurers may be unable to validate the claim.

5. Disputes Over Cause of Damage

In some cases, the insurer and policyholder may disagree on what caused the damage.

For example:

- Sudden water damage (covered) vs gradual leakage (often excluded)

These distinctions can impact whether a claim is approved.

6. Lapsed or Inactive Policy

If the policy was not active at the time of the incident — due to missed payments or cancellation — coverage may not apply.

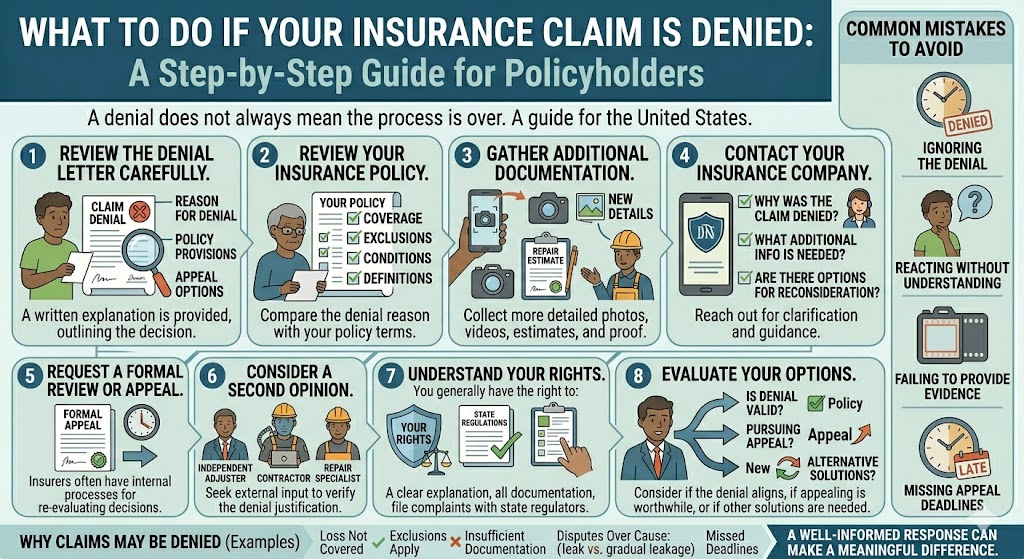

Step 1: Review the Denial Letter Carefully

When a claim is denied, the insurer provides a written explanation.

This document typically outlines:

- The reason for denial

- Relevant policy provisions

- Next steps or appeal options

Reading this carefully is critical. It provides the foundation for your response.

Step 2: Review Your Insurance Policy

Compare the denial reason with your policy.

Focus on:

- Coverage sections

- Exclusions

- Conditions

- Definitions

This helps you determine whether the denial aligns with the policy terms.

Step 3: Gather Additional Documentation

If you believe the denial may be incomplete or incorrect, collect supporting evidence.

This may include:

- Additional photos or videos

- Repair estimates

- Receipts

- Expert opinions (contractors, mechanics, etc.)

- Police or incident reports

More detailed documentation can strengthen your case.

Step 4: Contact Your Insurance Company

Reach out to your insurer for clarification.

Ask:

- Why was the claim denied?

- What additional information could change the outcome?

- Are there options for reconsideration?

Clear communication can sometimes resolve misunderstandings.

Step 5: Request a Formal Review or Appeal

Many insurers have internal processes for reviewing denied claims.

This may involve:

- Submitting additional evidence

- Requesting reassessment

- Providing written explanations

The appeal process varies by insurer but is often the next logical step.

Step 6: Consider a Second Opinion

In more complex cases, you may seek external input.

This could include:

- Independent adjusters

- Contractors or repair specialists

- Legal professionals (if necessary)

A second perspective can help clarify whether the denial is justified.

Step 7: Understand Your Rights

Insurance is regulated at the state level in the United States.

Policyholders generally have the right to:

- Receive a clear explanation of denial

- Request documentation

- File complaints with state regulators

Understanding your rights helps you navigate the process more confidently.

Step 8: Evaluate Your Options

After reviewing the situation, consider:

- Whether the denial is valid under the policy

- Whether pursuing an appeal is worthwhile

- Whether alternative solutions are needed

Not all denials can be reversed, but some can be reconsidered with additional information.

Real-World Example

Imagine a homeowner files a claim for water damage.

The insurer denies the claim, stating that the damage was caused by long-term leakage rather than a sudden event.

The policyholder then:

- Reviews the policy

- Provides additional evidence showing the damage occurred suddenly

- Requests a reassessment

In some cases, additional documentation can change how the claim is evaluated.

Common Mistakes to Avoid

1. Ignoring the Denial

A denial should not be dismissed without review.

2. Reacting Without Understanding the Policy

Decisions should be based on policy terms, not assumptions.

3. Failing to Provide Additional Evidence

Strong documentation can make a difference.

4. Missing Appeal Deadlines

Appeals often have time limits.

How to Reduce the Risk of Future Denials

While not all denials can be avoided, certain practices may help:

- Understand your policy before filing a claim

- Keep detailed records of assets and property

- Document incidents thoroughly

- Report claims promptly

- Review coverage regularly

Preparation improves outcomes.

When a Denial May Be Final

In some situations, a denial may be upheld.

This may occur when:

- The loss is clearly excluded

- Coverage limits do not apply

- Policy conditions were not met

Understanding when to move forward is part of the process.

The Bigger Perspective

Insurance claims are evaluated based on contracts, not assumptions.

A denial reflects how the insurer interprets the policy in relation to the claim.

While this can be frustrating, understanding the process allows policyholders to respond more effectively.

Final Thoughts

Having an insurance claim denied can be a challenging experience, but it does not necessarily mean the end of the process.

By reviewing the denial carefully, understanding your policy, gathering documentation, and exploring available options, you can approach the situation with clarity and structure.

Insurance is most effective when policyholders understand both their coverage and their rights.

A well-informed response can make a meaningful difference in how a denied claim is handled.