Insurance is often viewed as something you set up once and forget. However, as your life, finances, or business evolve, your insurance coverage may need to change as well.

One of the most important — and often overlooked — decisions is knowing when it makes sense to increase your insurance coverage. Increasing coverage can provide greater protection, but it also comes with higher costs.

Understanding when and why to adjust your coverage helps ensure that your protection remains aligned with your real-world risks.

This guide explains when it is worth increasing your insurance coverage and how to approach that decision strategically.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

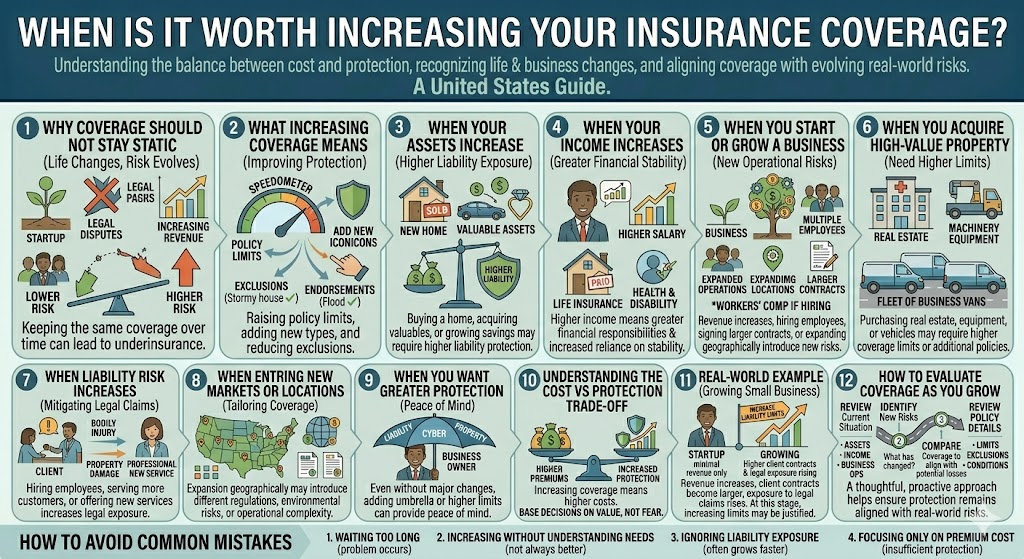

Why Insurance Coverage Should Not Stay Static

Life changes — and so does risk.

Situations that may require more coverage include:

- Increased income or assets

- Business growth

- Major purchases

- Changes in family structure

- Expansion into new markets

Keeping the same coverage over time can lead to underinsurance.

What Does Increasing Coverage Actually Mean?

Increasing insurance coverage can involve:

- Raising policy limits

- Adding new types of coverage

- Expanding existing protections

- Reducing exclusions through endorsements

It is not just about paying more — it is about improving protection.

Key Situations Where Increasing Coverage Makes Sense

1. When Your Assets Increase

As your wealth grows, so does your exposure.

Examples include:

- Buying a home

- Acquiring valuable assets

- Growing savings or investments

Higher assets may require higher liability protection.

2. When Your Income Increases

Higher income often means:

- Greater financial responsibilities

- More complex financial planning

- Increased reliance on stability

In this case, increasing coverage — especially for life or disability insurance — may be worth considering.

3. When You Start or Grow a Business

Business growth introduces new risks.

You may need to increase coverage if:

- Revenue increases

- You hire employees

- You expand operations

- You sign larger contracts

Coverage limits should reflect the scale of the business.

4. When You Acquire High-Value Property

Purchasing high-value items such as:

- Real estate

- Equipment

- Vehicles

May require higher coverage limits or additional policies.

5. When Liability Risk Increases

Certain situations increase exposure to legal claims.

Examples include:

- Hiring employees

- Serving more customers

- Offering new services

Increasing liability coverage can help mitigate these risks.

6. When You Enter New Markets or Locations

Expanding geographically may introduce:

- Different regulations

- New environmental risks

- Additional operational complexity

Coverage should reflect these changes.

7. When You Want Greater Financial Protection

Even without major changes, some individuals and businesses choose to increase coverage for peace of mind.

This may include:

- Adding umbrella insurance

- Increasing liability limits

- Expanding coverage scope

When Increasing Coverage May Not Be Necessary

Increasing coverage is not always the right decision.

It may not be necessary if:

- Your risk level has not changed

- Existing coverage is sufficient

- Costs outweigh potential benefits

The goal is balance — not maximum coverage.

Understanding the Cost vs Protection Trade-Off

Increasing coverage typically means higher premiums.

Before making a decision, consider:

- How much additional protection you gain

- Whether the risk justifies the cost

- Your ability to absorb potential losses

Insurance decisions should be based on value, not fear.

The Role of Deductibles

Adjusting deductibles can affect coverage decisions.

For example:

- Higher deductible → lower premium

- Lower deductible → higher premium

Sometimes increasing coverage while adjusting deductibles can create a better balance.

Real-World Example

Consider a small business owner who initially purchases basic liability coverage.

As the business grows:

- Revenue increases

- Client contracts become larger

- Exposure to legal claims rises

At this stage, increasing liability limits may be justified.

Without adjustment, the original coverage may no longer reflect the business’s risk profile.

Common Mistakes to Avoid

1. Waiting Too Long to Adjust Coverage

Delaying changes can create gaps in protection.

2. Increasing Coverage Without Understanding Needs

More coverage is not always better if it does not match actual risk.

3. Ignoring Liability Exposure

Liability risks often grow faster than expected.

4. Focusing Only on Premium Cost

Lower cost may result in insufficient protection.

How to Evaluate Whether to Increase Coverage

1. Review Your Current Situation

Consider:

- Assets

- Income

- Business operations

2. Identify New Risks

Ask:

- What has changed since I last reviewed my policy?

3. Compare Coverage to Exposure

Ensure your policy limits align with potential losses.

4. Review Policy Details

Look at:

- Limits

- Exclusions

- Conditions

How Often Should You Review Coverage?

A general guideline is to review insurance:

- Annually

- After major life or business changes

- After significant purchases or growth

Regular reviews help ensure alignment with your current situation.

The Strategic Perspective

Increasing insurance coverage is not just about protection — it is about managing risk strategically.

Well-structured coverage can:

- Protect assets

- Support financial stability

- Reduce uncertainty

- Enable growth

For businesses, it can also improve credibility with clients and partners.

Final Thoughts

Knowing when to increase your insurance coverage is a key part of managing risk effectively.

As your life or business evolves, your insurance should evolve with it. Increasing coverage at the right time can help prevent gaps that may lead to significant financial exposure.

The goal is not to have the most coverage possible, but to have the right coverage for your situation.

A thoughtful, proactive approach to insurance helps ensure that protection remains aligned with real-world needs.