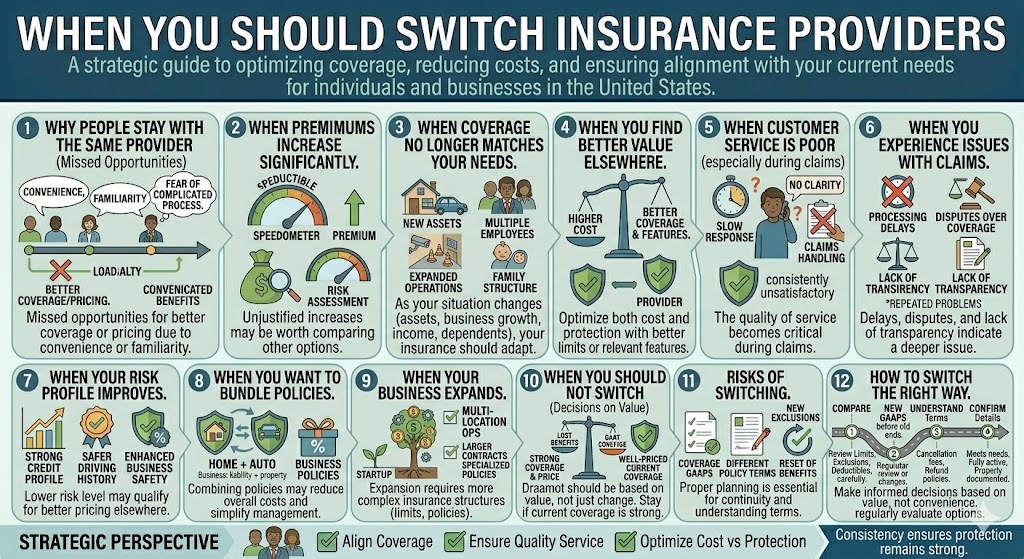

Choosing an insurance provider is not a one-time decision. Over time, your needs, financial situation, and risk profile may change — and so may the quality and pricing of your insurance coverage.

Many policyholders stay with the same provider for years without reconsidering their options. While loyalty can have benefits, it is not always the most efficient strategy.

Understanding when you should switch insurance providers can help you improve coverage, reduce costs, and ensure that your insurance aligns with your current situation.

This article is for informational purposes only and does not constitute financial, legal, or insurance advice.

Why People Stay With the Same Insurance Provider

Before discussing when to switch, it is important to understand why many people do not.

Common reasons include:

- Convenience

- Familiarity with the provider

- Fear of a complicated process

- Assumption that switching will not make a difference

While these reasons are understandable, they may lead to missed opportunities for better coverage or pricing.

When Switching Insurance Providers Makes Sense

1. When Your Premiums Increase Significantly

One of the most common reasons to consider switching is a noticeable increase in premiums.

This may happen due to:

- Changes in risk assessment

- Market conditions

- Claims history

If the increase is not clearly justified, it may be worth comparing other options.

2. When Your Coverage No Longer Matches Your Needs

As your situation changes, your insurance should adapt.

You may need different coverage if:

- You purchase new assets

- Your business grows

- Your income changes

- You add or remove dependents

If your current provider cannot offer the right structure, switching may be appropriate.

3. When You Find Better Value Elsewhere

Insurance is not just about price — it is about value.

A different provider may offer:

- Better coverage limits

- More relevant policy features

- Improved pricing for similar protection

Switching can help optimize both cost and protection.

4. When Customer Service Is Poor

The quality of service becomes especially important during claims.

Warning signs include:

- Slow response times

- Lack of clarity

- Difficulty reaching support

- Poor claims handling experience

If service is consistently unsatisfactory, switching may improve your overall experience.

5. When You Experience Issues With Claims

A negative claims experience can be a strong signal.

Examples include:

- Delays in processing

- Disputes over coverage

- Lack of transparency

While not every issue justifies switching, repeated problems may indicate a deeper issue.

6. When Your Risk Profile Improves

If your risk level decreases, you may qualify for better pricing elsewhere.

Examples include:

- Improved credit profile

- Safer driving history

- Enhanced business safety measures

Some providers may offer more competitive rates based on updated risk.

7. When You Want to Bundle Policies

Switching providers can make sense if bundling opportunities are available.

Combining policies may:

- Reduce overall costs

- Simplify management

- Improve consistency across coverage

8. When Your Business Expands

For businesses, growth often requires more complex insurance structures.

If your current provider cannot support:

- Higher coverage limits

- Specialized policies

- Multi-location operations

Switching may be necessary.

When You Should NOT Switch Providers

Switching is not always the best decision.

You may want to stay if:

- Your current coverage is strong and well-priced

- Switching would create gaps in coverage

- You would lose significant loyalty benefits

- The new policy does not offer meaningful improvements

Decisions should be based on value, not just change.

Risks of Switching Insurance Providers

While switching can be beneficial, it also involves potential risks.

1. Coverage Gaps

If policies are not properly aligned, there may be periods without coverage.

2. Differences in Policy Terms

New policies may include:

- Different exclusions

- Different conditions

- Different definitions

These details matter.

3. Reset of Benefits or Conditions

Some benefits may reset when switching providers.

4. Administrative Complexity

Switching requires:

- Reviewing policies

- Coordinating timelines

- Ensuring continuity

Proper planning is essential.

How to Switch Insurance Providers the Right Way

1. Compare Policies Carefully

Do not focus only on price.

Review:

- Coverage limits

- Exclusions

- Deductibles

- Policy conditions

2. Avoid Coverage Gaps

Ensure the new policy starts before the old one ends.

3. Understand Cancellation Terms

Check for:

- Cancellation fees

- Refund policies

- Required notice periods

4. Confirm All Details Before Switching

Make sure the new coverage:

- Meets your needs

- Is fully active

- Has been properly documented

Real-World Example

Consider a homeowner who has been with the same insurer for several years.

Over time:

- Premiums increase

- Property value changes

- Coverage remains unchanged

After comparing options:

- A new provider offers better coverage at a similar price

- Policy limits are better aligned with current needs

Switching in this case may improve both protection and efficiency.

How Often Should You Evaluate Your Provider?

A good practice is to review your insurance provider:

- Once a year

- After major life or business changes

- When premiums change significantly

Regular evaluation helps ensure your coverage remains competitive.

The Strategic Perspective

Switching insurance providers is not about chasing the lowest price.

It is about:

- Aligning coverage with your current situation

- Ensuring quality service

- Optimizing cost vs protection

A well-timed switch can improve both financial efficiency and risk management.

Final Thoughts

Insurance needs evolve over time, and staying with the same provider indefinitely may not always be the best strategy.

Knowing when to switch — and how to do it correctly — allows you to maintain strong protection while optimizing cost and service.

The key is to make informed decisions based on value, not convenience.

Regularly reviewing your insurance options ensures that your coverage continues to support your financial and operational goals.