The insurance industry is undergoing one of the most significant transformations in its history. What was once perceived as slow, paper-based, and reactive is rapidly becoming smarter, more transparent, and increasingly centered around customer needs.

Advancements in technology, data analytics, artificial intelligence, and digital communication are redefining how insurance is designed and delivered. At the same time, shifting consumer expectations and evolving regulatory standards are pushing insurers to adopt clearer, more accessible models.

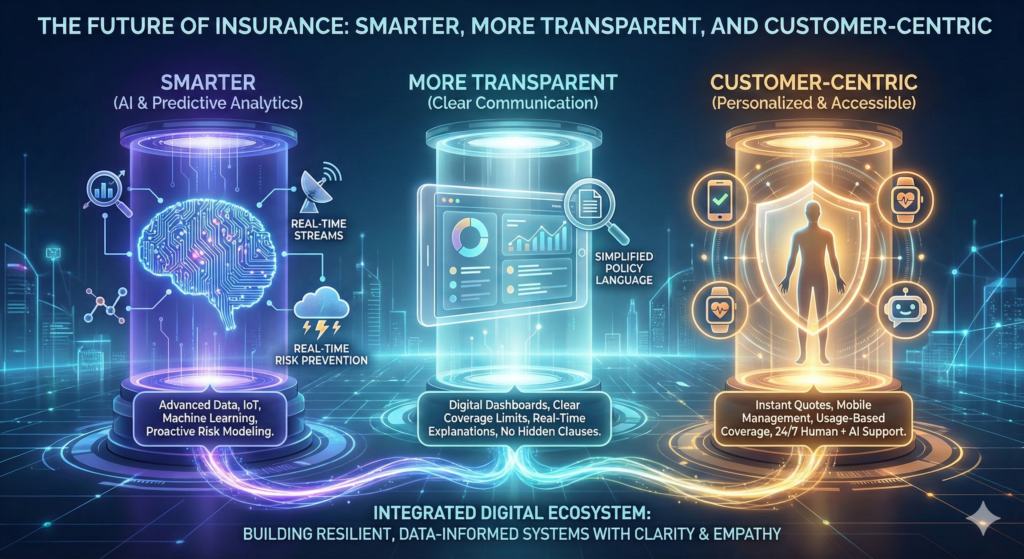

The future of insurance is not just about automation. It is about building systems that are intelligent, transparent, and aligned with real customer needs.

Smarter Insurance Through Advanced Data Analytics

Insurance has always relied on data. However, the scope and sophistication of data analysis are expanding dramatically.

In the future, insurers will increasingly use:

- Real-time behavioral data

- Predictive analytics

- Machine learning models

- Environmental and climate risk data

- Operational performance metrics

These tools allow for more precise risk assessment.

Rather than relying on broad demographic categories, insurers can refine pricing based on actual behavior and measurable risk indicators.

Smarter underwriting models may result in:

- Improved pricing accuracy

- Better risk segmentation

- More sustainable financial reserves

This evolution enhances stability across the insurance ecosystem.

Increased Transparency in Policy Structures

One of the most common frustrations customers express is confusion about policy language.

Insurance contracts are legally detailed, but future models aim to improve clarity through:

- Simplified digital policy summaries

- Interactive coverage dashboards

- Real-time explanations of coverage limits

- Clear breakdowns of deductibles and exclusions

Digital interfaces can translate complex policy terms into user-friendly summaries without sacrificing legal precision.

Greater transparency strengthens trust.

When customers understand what is covered — and what is not — expectations align more realistically with outcomes.

Customer-Centric Digital Platforms

The future of insurance emphasizes accessibility and convenience.

Customers increasingly expect:

- Instant quotes

- Mobile policy management

- Online claims tracking

- Real-time notifications

- Personalized coverage options

Digital platforms allow policyholders to interact with insurers at any time.

Self-service tools provide flexibility, while human representatives remain available for complex inquiries.

Customer-centric design prioritizes clarity, responsiveness, and ease of use.

Real-Time Risk Prevention

Insurance is gradually shifting from reactive claims payment to proactive risk prevention.

Emerging technologies such as IoT devices and connected sensors enable:

- Early detection of water leaks

- Monitoring of fire hazards

- Fleet management risk tracking

- Cyber threat detection

By identifying risks early, insurers can help reduce loss severity.

In the future, insurance may increasingly incorporate preventive services rather than focusing solely on post-loss compensation.

This proactive model benefits both insurers and policyholders.

Personalized and Usage-Based Coverage

Personalization is becoming a defining feature of modern insurance.

Usage-based insurance models may expand beyond auto coverage to include:

- On-demand business coverage

- Event-based insurance products

- Short-term specialty coverage

Customers may adjust coverage dynamically based on specific needs.

Flexible policy structures reflect the evolving nature of work, travel, and digital business operations.

Personalization aligns premiums more closely with actual exposure.

Artificial Intelligence and Automation

Artificial intelligence will continue to enhance underwriting and claims processing.

Future developments may include:

- Faster claims resolution through image analysis

- Predictive risk alerts

- Automated policy adjustments

- Enhanced fraud detection systems

Automation improves operational efficiency while reducing administrative delays.

However, the human element will remain essential for complex cases and nuanced decision-making.

A hybrid model combining AI efficiency with human oversight is likely to define the next generation of insurance services.

Stronger Regulatory and Ethical Frameworks

As insurance becomes more data-driven, regulatory oversight will remain central.

Future insurance models must address:

- Data privacy protections

- Algorithmic fairness

- Transparent pricing practices

- Consumer protection standards

Regulators will continue monitoring how insurers use data in underwriting and pricing.

Ethical implementation of AI systems will be critical to maintaining public trust.

Innovation must align with accountability.

Embedded Insurance Ecosystems

Insurance distribution is also evolving.

Embedded insurance integrates coverage directly into digital transactions.

Examples may include:

- Travel coverage added during booking

- Device protection integrated at checkout

- Business coverage included in digital service subscriptions

This model reduces friction by offering coverage at the moment of need.

Embedded insurance may become increasingly common as digital ecosystems expand.

Climate and Emerging Risk Adaptation

Climate-related risks and emerging technologies introduce new exposure categories.

Future insurance solutions may address:

- Climate volatility

- Renewable energy systems

- Artificial intelligence liability

- Digital asset protection

As industries evolve, insurance products must adapt accordingly.

Forward-looking risk modeling will be essential.

Insurers will rely heavily on predictive analytics to anticipate emerging exposures.

Building Trust Through Transparency

Trust is foundational to insurance.

The future emphasizes clearer communication regarding:

- How premiums are calculated

- How claims are evaluated

- How data is used

- How coverage decisions are made

Transparency reduces misunderstanding and builds long-term relationships.

Insurance companies that prioritize clarity may strengthen customer loyalty.

The Human-Centered Future

Despite technological advancements, insurance remains a human-centered service.

Customers seek reassurance during uncertain moments.

The future of insurance will likely balance:

- Digital efficiency

- Personalized data insights

- Human advisory support

Technology enhances processes, but empathy and professional expertise remain essential.

Customer-centric design does not eliminate human connection — it enhances it.

Insurance as Financial Infrastructure

Looking ahead, insurance may increasingly be viewed as part of broader financial infrastructure.

Integrated systems could connect:

- Insurance platforms

- Financial planning tools

- Risk management dashboards

- Regulatory reporting systems

This integration supports holistic financial resilience.

Insurance becomes embedded within larger ecosystems of financial services.

Conclusion

The future of insurance is smarter, more transparent, and increasingly customer-centric. Advanced data analytics, artificial intelligence, automation, and digital platforms are reshaping underwriting, claims management, and policy administration.

At the same time, transparency, ethical responsibility, and regulatory compliance remain essential pillars of trust.

Insurance is evolving from a reactive system into a proactive, data-informed, and digitally integrated service.

As innovation continues, the industry’s success will depend on its ability to combine intelligent technology with clear communication and human-centered support.

The future of insurance is not just about speed or automation — it is about building resilient systems that serve customers with clarity, precision, and accountability