When evaluating any insurance policy — whether auto, home, health, or business — two of the most important financial components are the premium and the deductible.

Many policyholders focus primarily on the monthly cost. However, understanding how premiums and deductibles interact is essential for making informed decisions that align with your financial capacity and risk tolerance.

This guide explains what premiums and deductibles are, how they affect each other, and how to approach the balance strategically.

This article is for informational purposes only and does not constitute financial or legal advice.

What Is an Insurance Premium?

A premium is the amount paid to maintain an active insurance policy. It can be paid monthly, quarterly, semi-annually, or annually depending on the insurer and policy structure.

Premiums are calculated based on risk factors, which may include:

- Age

- Location

- Claims history

- Type of coverage

- Coverage limits

- Industry risk (for business policies)

- Vehicle type (for auto insurance)

- Property value (for homeowners insurance)

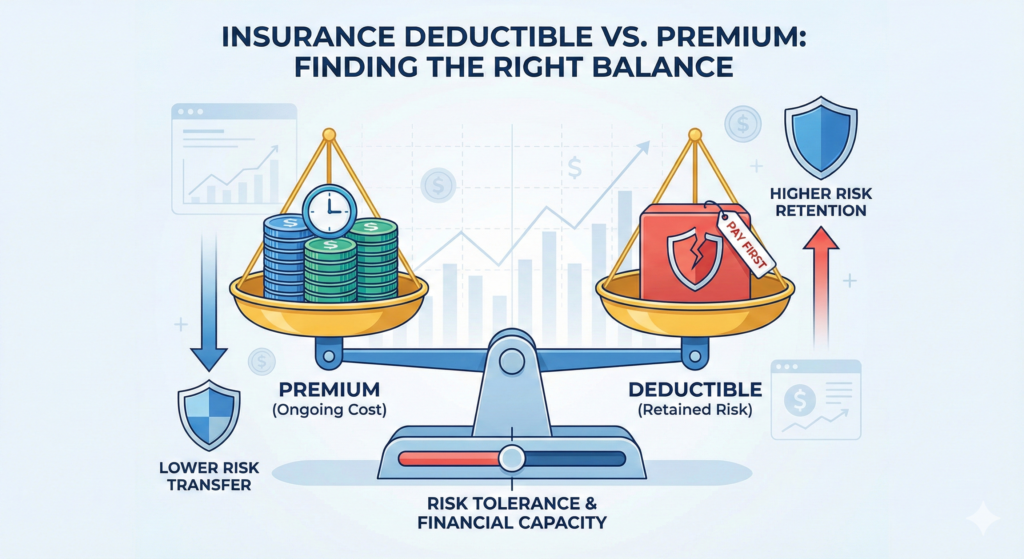

In simple terms, the premium is the cost of transferring certain financial risks to the insurance company.

Lower risk typically results in lower premiums, while higher perceived risk may increase cost.

What Is a Deductible?

A deductible is the amount the policyholder must pay out of pocket before insurance coverage begins to apply to a covered claim.

For example:

If you have a $1,000 deductible and experience a $5,000 covered loss, you may pay the first $1,000. The insurer may then pay the remaining $4,000, subject to policy terms and limits.

Deductibles can vary widely depending on policy type:

- Auto insurance deductibles commonly range from $250 to $2,000

- Homeowners insurance deductibles may be fixed amounts or percentage-based

- Health insurance deductibles can range from hundreds to several thousand dollars

- Business policies may have per-claim or aggregate deductibles

The deductible represents the portion of risk you retain.

The Core Trade-Off: Risk Sharing

Premiums and deductibles are directly connected.

In general:

- Higher deductibles often result in lower premiums

- Lower deductibles typically lead to higher premiums

This relationship exists because insurers adjust pricing based on how much risk the policyholder is willing to assume.

When you choose a higher deductible, you agree to absorb more financial responsibility before insurance responds. In return, the insurer reduces your premium.

When you choose a lower deductible, the insurer takes on more immediate financial responsibility, which increases the premium.

Understanding this balance is central to effective insurance planning.

How to Evaluate the Right Balance

Choosing between higher or lower deductibles should not be based solely on minimizing monthly cost.

Instead, consider the following factors.

1. Emergency Savings and Liquidity

If you choose a high deductible, you should be financially prepared to pay that amount at any time.

Ask yourself:

- Could I comfortably cover this deductible if a claim occurs tomorrow?

- Would paying this amount create financial strain?

If the deductible exceeds your accessible emergency funds, you may be exposing yourself to short-term financial stress.

2. Frequency of Claims

Some types of insurance have a higher likelihood of claims than others.

For example:

- Minor auto accidents are relatively common.

- Large home losses are less frequent but more severe.

If you expect low-frequency claims, a higher deductible may reduce long-term premium costs.

If claims are more likely, a lower deductible may provide greater predictability.

3. Risk Tolerance

Personal comfort with risk varies.

Some individuals prefer predictable monthly costs and minimal out-of-pocket surprises.

Others are comfortable retaining more risk in exchange for lower recurring premiums.

Neither approach is inherently correct — it depends on financial behavior and risk tolerance.

4. Coverage Limits Matter Too

Focusing only on deductibles can be misleading.

Coverage limits determine the maximum the insurer will pay for a covered claim.

A low deductible with insufficient coverage limits may not provide meaningful protection in major loss scenarios.

Balancing deductible, premium, and coverage limits together creates a more effective structure.

Common Mistakes to Avoid

Mistake 1: Choosing the Lowest Premium Without Reviewing the Deductible

Lower premiums often come with higher deductibles.

Without reviewing the full structure, policyholders may underestimate potential out-of-pocket exposure.

Mistake 2: Selecting a Deductible Higher Than Available Cash

A deductible is not theoretical. It must be paid before coverage applies.

If a deductible is set too high relative to available funds, claims become financially stressful.

Mistake 3: Ignoring Long-Term Cost

Over time, premium differences accumulate.

For example, choosing a lower premium by increasing your deductible may save hundreds or thousands of dollars across several years — provided claims are infrequent.

Long-term evaluation is essential.

Example Scenario: Auto Insurance

Consider two auto insurance options:

Option A:

- $500 deductible

- Higher monthly premium

Option B:

- $1,500 deductible

- Lower monthly premium

If no accidents occur for several years, Option B may result in overall cost savings.

However, if a claim occurs early, the higher deductible must be paid out of pocket.

There is no universal answer — only a balance between probability and financial capacity.

Example Scenario: Health Insurance

In health insurance, high-deductible health plans (HDHPs) often have lower monthly premiums but higher upfront costs before coverage activates.

These plans may be paired with Health Savings Accounts (HSAs), depending on eligibility.

However, policyholders must understand:

- When coverage begins

- What services are subject to the deductible

- Out-of-pocket maximum limits

Healthcare cost unpredictability makes deductible planning particularly important.

Business Insurance Considerations

For small business owners, deductibles may apply per claim or in aggregate.

Business owners should evaluate:

- Cash reserves

- Operational continuity

- Contractual obligations

- Industry risk exposure

A deductible that seems manageable in theory may become disruptive during operational downtime.

Long-Term Strategic Perspective

Insurance is not designed to eliminate cost — it is designed to distribute risk.

A balanced approach involves:

- Reviewing financial reserves

- Evaluating exposure realistically

- Avoiding emotional decision-making

- Reassessing coverage annually

Major life or business events may justify revisiting deductible choices.

Examples include:

- Purchasing a new home

- Starting a business

- Significant income changes

- Relocation

- Expansion of operations

Insurance decisions evolve over time.

Regulatory and Policy Variations

Insurance regulations vary by state and by policy type.

Some policies include:

- Separate deductibles for specific perils

- Percentage-based deductibles (common in homeowners insurance)

- Tiered deductibles

Policy documents should be reviewed carefully before selection.

Final Thoughts

Understanding the relationship between premiums and deductibles is fundamental to responsible insurance planning.

Premiums represent ongoing cost. Deductibles represent retained risk.

The right balance depends on:

- Financial stability

- Risk tolerance

- Claim probability

- Coverage limits

- Long-term strategy

Insurance works best when it is structured intentionally — not selected solely based on the lowest price.

By evaluating both premium and deductible together, individuals and businesses can build more resilient financial protection.