Starting and running a small business in the United States involves opportunity — but also responsibility. Whether you operate a local retail shop, consulting firm, digital agency, construction company, or tech startup, risk exposure is part of daily operations.

Insurance plays a foundational role in managing those risks.

While coverage needs vary depending on industry and size, there are core policies that most small business owners should evaluate. Understanding these policies helps business owners make informed, structured decisions about financial protection.

This article is for informational purposes only and does not constitute legal or financial advice.

Why Insurance Is Critical for Small Businesses

Small businesses often operate with limited financial buffers. A single lawsuit, accident, or unexpected disruption can create significant financial strain.

Insurance helps:

- Protect business assets

- Cover legal defense costs

- Maintain operational continuity

- Meet contractual requirements

- Comply with state regulations

Without appropriate coverage, business owners may face personal financial exposure depending on business structure and liability circumstances.

Insurance is not about eliminating risk — it is about managing it responsibly.

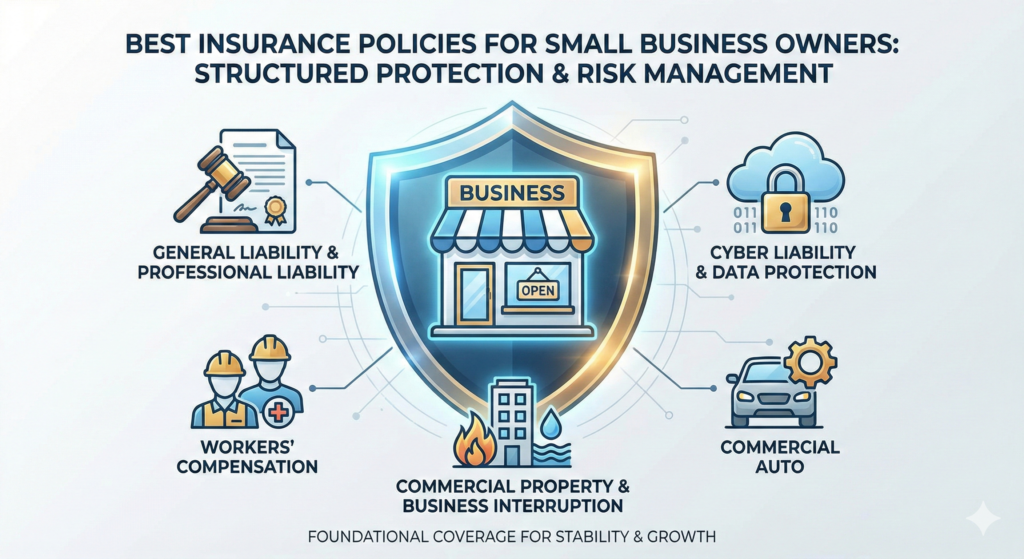

1. General Liability Insurance

General liability insurance is often considered the foundation of business coverage.

What It Typically Covers

- Third-party bodily injury claims

- Property damage caused by business operations

- Legal defense costs

- Advertising injury (such as copyright or trademark claims in marketing)

For example, if a customer slips and falls at your physical location, general liability coverage may respond, subject to policy terms and limits.

Even home-based businesses may need liability protection if clients visit or if operations create third-party risk.

Many commercial leases and client contracts require proof of general liability coverage.

2. Professional Liability Insurance (Errors & Omissions)

Professional liability insurance — also called Errors & Omissions (E&O) insurance — is essential for service-based businesses.

Who Typically Needs It?

- Consultants

- Accountants

- Marketing agencies

- IT service providers

- Financial professionals

- Designers and creative professionals

This policy addresses claims alleging negligence, errors, or failure to deliver professional services as expected.

Even if claims are unfounded, legal defense costs alone can be substantial. Professional liability coverage helps manage those risks.

3. Commercial Property Insurance

Commercial property insurance protects physical assets owned or leased by the business.

Covered Assets May Include:

- Office buildings

- Retail spaces

- Equipment

- Inventory

- Furniture

- Computers and technology

Covered risks may include fire, theft, vandalism, and certain weather-related events (depending on the policy).

Businesses operating from leased spaces often still need property coverage for contents and equipment.

4. Workers’ Compensation Insurance

Workers’ compensation insurance is required in most states for businesses with employees.

It Typically Covers:

- Medical expenses for workplace injuries

- Partial wage replacement

- Rehabilitation costs

Requirements vary by state, but noncompliance can result in penalties.

Even small teams carry workplace risk. Workers’ compensation provides structured support for employees while protecting employers from direct injury-related liability claims.

5. Business Interruption Insurance

Business interruption insurance helps replace lost income if operations are temporarily halted due to a covered event.

For example:

- Fire damage closing a storefront

- Severe weather damage affecting operations

- Certain property-related disruptions

This coverage may help cover:

- Lost revenue

- Ongoing expenses such as rent

- Payroll (depending on policy terms)

For businesses operating on tight margins, temporary shutdowns can be financially destabilizing.

6. Cyber Liability Insurance

As digital operations expand, cyber liability insurance is becoming increasingly important — especially for businesses handling customer data.

It May Cover:

- Data breach response costs

- Legal defense

- Customer notification expenses

- Business interruption due to cyber events

- Regulatory fines where permitted

Even small businesses are targeted by cyber threats. Data protection responsibilities extend beyond large corporations.

Cyber insurance does not eliminate risk but can provide financial support during digital incidents.

7. Commercial Auto Insurance

If a business owns vehicles or employees use vehicles for company operations, commercial auto insurance may be required.

This differs from personal auto insurance and typically covers:

- Liability from accidents

- Vehicle damage

- Medical expenses

- Uninsured motorist incidents

Using personal auto policies for business purposes may create coverage gaps.

8. Directors and Officers (D&O) Insurance

D&O insurance is often relevant for startups, nonprofits, and corporations with investors or boards.

It protects directors and officers from claims alleging:

- Mismanagement

- Breach of fiduciary duty

- Regulatory violations

While not required for every small business, it may be necessary when seeking outside investment or forming structured governance systems.

Business Owner’s Policy (BOP)

Many small businesses qualify for a Business Owner’s Policy (BOP).

A BOP typically bundles:

- General liability

- Commercial property

- Business interruption coverage

This approach may simplify administration and reduce overall cost compared to purchasing policies separately.

Eligibility depends on industry type, revenue size, and risk profile.

Industry-Specific Considerations

Different industries face unique risk exposures.

Examples:

- Construction businesses may need contractor-specific liability coverage.

- Restaurants may require food contamination endorsements.

- Tech startups may need intellectual property and cyber protection.

- Healthcare providers may require malpractice coverage.

Insurance planning should reflect operational realities.

How to Evaluate Coverage Needs

Small business owners should consider:

- Physical asset value

- Number of employees

- Client contract requirements

- Industry regulatory standards

- Digital data exposure

- Revenue stability

- Geographic location

A structured risk assessment helps prioritize coverage appropriately.

Avoid both underinsuring and overinsuring.

Common Insurance Mistakes Small Business Owners Make

- Assuming home insurance covers home-based businesses

- Ignoring professional liability exposure

- Focusing only on premium cost

- Not reviewing coverage annually

- Failing to update policies as the business grows

Insurance needs evolve as businesses scale.

Reviewing Coverage Over Time

Business insurance is not static.

Review policies after:

- Hiring new employees

- Expanding to new states

- Launching new services

- Purchasing significant equipment

- Entering high-value contracts

Periodic review supports alignment between coverage and operations.

Regulatory and Legal Compliance

Insurance in the United States is regulated at the state level.

Compliance may involve:

- Workers’ compensation requirements

- Industry licensing mandates

- Contractual insurance clauses

Business owners should understand local regulations and consult professionals when necessary.

Final Thoughts

There is no single insurance package that fits every small business.

However, most businesses benefit from evaluating:

- General liability insurance

- Professional liability insurance

- Commercial property coverage

- Workers’ compensation

- Cyber liability insurance

- Business interruption protection

Insurance should be viewed as part of structured risk management, not simply an expense.

When aligned properly with operations, insurance supports stability, continuity, and responsible business growth.