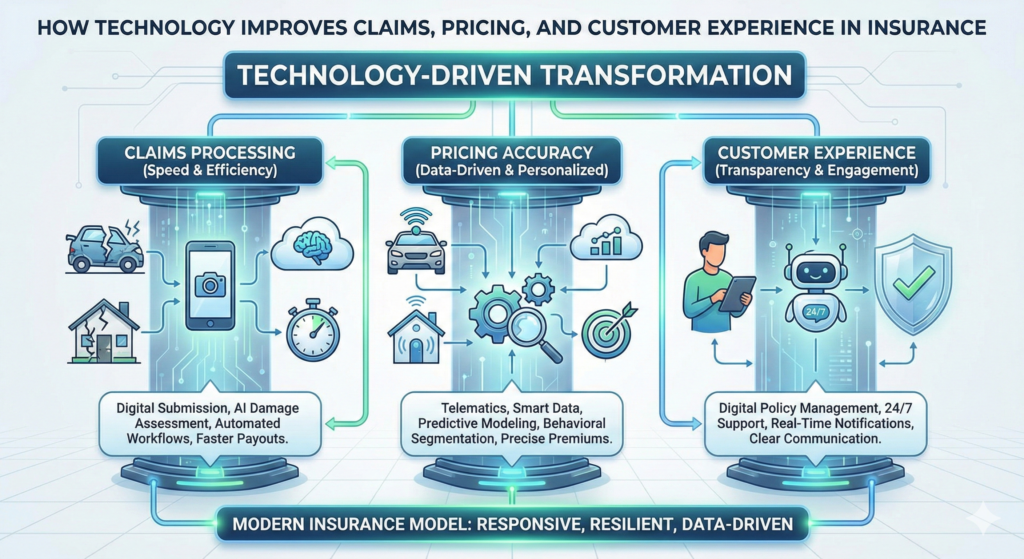

The insurance industry has historically been associated with paperwork, long waiting periods, and complex policy language. However, technological advancements are significantly reshaping how insurers operate and how customers interact with their coverage.

Technology is improving three core pillars of the insurance model:

- Claims processing

- Pricing accuracy

- Customer experience

By integrating data analytics, artificial intelligence (AI), automation, and digital platforms, insurers are enhancing efficiency, transparency, and personalization across the entire insurance lifecycle.

Understanding how technology improves these areas provides insight into the modern evolution of insurance services.

Technology and Claims Processing

Claims management is one of the most critical functions in insurance. It is also where customer expectations are highest. When policyholders experience a loss, they expect clarity, speed, and fairness.

Technology enhances claims processing in several ways.

1. Digital Claims Submission

Mobile apps and online portals allow policyholders to:

- Submit claims instantly

- Upload photos or videos

- Provide digital documentation

- Track claim status in real time

This eliminates the need for paper forms and reduces administrative delays.

Customers gain visibility into the claims process, improving transparency.

2. AI-Powered Damage Assessment

Artificial intelligence can analyze images of property damage and estimate repair costs using machine learning models trained on historical claims data.

For example:

- Auto damage can be evaluated through uploaded photos

- Property damage may be assessed using drone imagery

- AI systems can compare damage patterns against existing databases

This speeds up evaluation for straightforward claims.

Complex cases still require human adjusters, but automation reduces workload and accelerates decision-making.

3. Fraud Detection

Fraud detection systems analyze large volumes of data to identify unusual patterns.

Machine learning algorithms may flag:

- Inconsistent documentation

- Repeated claim patterns

- Suspicious timing indicators

By identifying potential fraud early, insurers protect financial stability and maintain fairness across risk pools.

Technology improves integrity without disrupting legitimate claims.

Technology and Pricing Accuracy

Pricing is central to the insurance model. Accurate pricing ensures that premiums reflect risk appropriately while maintaining financial sustainability.

Technology enhances pricing in several key areas.

1. Data-Driven Risk Segmentation

Traditional pricing relied on broad categories such as age, zip code, and claims history.

Modern data analytics allows insurers to incorporate additional factors, such as:

- Driving behavior via telematics

- Smart home sensor data

- Business cybersecurity posture

- Real-time environmental risk indicators

More granular data improves segmentation.

Instead of pricing risk based solely on demographic averages, insurers can evaluate behavioral patterns and operational practices.

2. Predictive Modeling

Predictive analytics uses historical data and machine learning to forecast potential future claims.

These models estimate:

- Claim frequency

- Claim severity

- Catastrophic event exposure

Improved forecasting enhances pricing precision and reserve allocation.

Accurate pricing supports long-term financial stability for both insurers and policyholders.

3. Usage-Based Insurance

Technology enables usage-based insurance models.

For example:

- Auto insurance premiums may reflect actual driving behavior.

- Commercial fleets may be priced based on operational data.

Usage-based models create pricing structures that are more behavior-oriented rather than static.

This personalization aligns premiums more closely with actual risk exposure.

Technology and Customer Experience

Customer experience has become a major focus in modern insurance.

Technology improves customer interaction across multiple touchpoints.

1. Digital Policy Management

Customers can now:

- Access policies online

- Modify coverage limits

- Update personal information

- Download documentation instantly

Digital dashboards provide clarity and accessibility.

Customers no longer rely solely on phone calls or physical paperwork.

2. 24/7 Support Through Automation

Chatbots and AI-driven customer service tools provide round-the-clock assistance.

These systems can answer:

- Policy questions

- Billing inquiries

- Coverage explanations

While complex issues may require human representatives, automation reduces wait times for routine inquiries.

3. Transparency and Communication

Digital notifications keep customers informed about:

- Renewal dates

- Payment confirmations

- Claim status updates

- Policy changes

Clear communication enhances trust and reduces uncertainty.

Transparency improves overall satisfaction.

Real-Time Risk Monitoring

Technology also enables proactive risk management.

Internet of Things (IoT) devices can monitor:

- Water leaks in commercial buildings

- Temperature fluctuations in storage facilities

- Driving patterns in vehicle fleets

Real-time alerts allow early intervention, potentially reducing loss severity.

Insurance increasingly supports prevention rather than simply responding after losses occur.

Operational Efficiency and Cost Control

Automation improves back-end processes such as:

- Policy issuance

- Document generation

- Compliance monitoring

- Payment processing

Streamlined operations reduce administrative burdens.

Operational efficiency can translate into faster service delivery and improved consistency.

However, insurers must balance automation with regulatory compliance and ethical standards.

Ethical and Regulatory Considerations

As insurers collect more behavioral and operational data, transparency and fairness become critical.

Key considerations include:

- Data privacy protections

- Algorithmic bias prevention

- Clear explanation of pricing factors

- Compliance with federal and state regulations

Technology enhances capability but requires responsible implementation.

Maintaining consumer trust depends on ethical data use.

The Human Element in a Digital System

Despite technological advancements, insurance remains a human-centered service.

Complex claims, legal disputes, and nuanced risk evaluations require professional judgment.

Technology supports decision-making but does not eliminate the need for human expertise.

The most effective systems combine automation with experienced oversight.

The Strategic Impact on the Industry

The integration of technology improves not only efficiency but also competitiveness.

Insurers that adopt digital tools effectively can:

- Reduce processing delays

- Enhance pricing precision

- Strengthen customer retention

- Improve risk forecasting

Technology transforms insurance from a reactive administrative system into a data-driven service model.

Conclusion

Technology is reshaping insurance by improving claims processing speed, enhancing pricing accuracy, and elevating customer experience.

Through AI, predictive analytics, automation, and digital platforms, insurers can provide more personalized, transparent, and efficient services.

At the same time, regulatory compliance, data ethics, and human oversight remain essential components of responsible innovation.

Modern insurance is increasingly defined by its ability to combine structured risk management with intelligent technological systems — creating a more responsive and resilient industry.