Life insurance is one of the most important financial protection tools available in the United States. However, many people find it confusing — especially when deciding between term life insurance and whole life insurance.

Both options provide a death benefit to beneficiaries. But they are structured very differently. Understanding those differences is essential before making any long-term decision.

This guide explains how each type works, what distinguishes them, and how to evaluate which option may align with your personal financial situation.

This article is for informational purposes only and does not constitute financial or legal advice.

What Is Term Life Insurance?

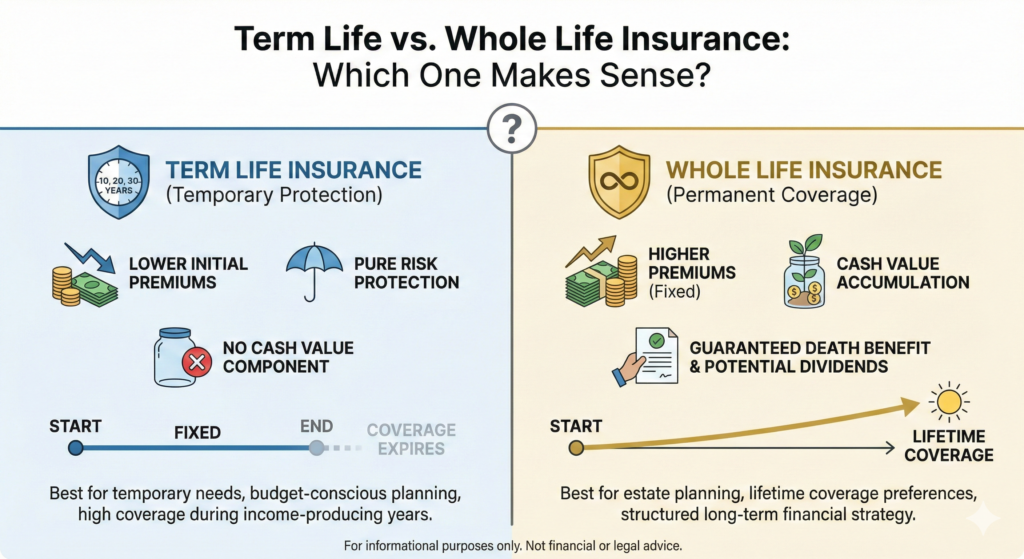

Term life insurance provides coverage for a specific period of time — commonly 10, 20, or 30 years.

If the insured person passes away during the policy term, beneficiaries receive the death benefit. If the policy term ends and the insured is still living, coverage expires unless renewed or converted.

Key Characteristics of Term Life Insurance

- Fixed coverage period

- Typically lower premiums compared to permanent policies

- No cash value component

- Straightforward structure

Because it focuses strictly on risk protection, term life insurance is often more affordable than whole life insurance for the same death benefit amount.

When Is Term Life Insurance Often Considered?

Term life insurance is commonly evaluated when financial responsibilities are temporary or time-specific, such as:

- Raising young children

- Paying off a mortgage

- Covering student loans

- Protecting business loans

- Replacing income during working years

In these cases, coverage is needed during a defined financial risk window.

Once major obligations decrease, some individuals reassess whether coverage remains necessary.

What Is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance. As long as premiums are paid, coverage typically remains in force for the insured’s lifetime.

In addition to the death benefit, whole life policies generally include a cash value component that accumulates over time.

Key Characteristics of Whole Life Insurance

- Lifetime coverage

- Fixed premiums (in most traditional policies)

- Guaranteed death benefit

- Cash value accumulation

- Potential dividend eligibility (depending on insurer and policy type)

Whole life insurance is structured differently than term insurance because it combines protection with a long-term financial component.

Understanding the Cash Value Feature

One of the main distinctions between term and whole life insurance is the presence of cash value.

Cash value is a portion of the premium that builds over time within the policy. The growth rate depends on the policy structure and insurer.

Policyholders may have options such as:

- Borrowing against the cash value

- Surrendering the policy for accumulated value

- Using dividends to reduce premiums (if applicable)

It is important to understand that accessing cash value may affect the death benefit or policy performance. Policy terms vary significantly between insurers.

Cost Comparison: Why Whole Life Costs More

Whole life insurance premiums are typically higher than term life premiums for comparable death benefit amounts.

This is because:

- Coverage lasts a lifetime

- The insurer assumes long-term risk

- Part of the premium contributes to cash value

- There may be guaranteed growth components

Term life, on the other hand, is priced based on temporary risk exposure.

Lower cost does not automatically mean better — it simply reflects a different structure.

Flexibility and Long-Term Planning

When deciding between term and whole life insurance, duration plays a critical role.

Term Life May Align With:

- Temporary financial protection needs

- Budget-conscious planning

- High coverage during income-producing years

Whole Life May Align With:

- Estate planning objectives

- Lifetime coverage preferences

- Structured long-term financial planning

Each option serves a distinct purpose. The appropriate choice depends on financial goals, responsibilities, and risk tolerance.

Common Misunderstandings About Life Insurance

Misconception 1: “Term Life Is Always Better Because It’s Cheaper”

Affordability is important, but price alone should not determine the decision. Coverage duration and financial objectives matter equally.

Misconception 2: “Whole Life Is an Investment Replacement”

Whole life insurance is primarily designed for protection. While it includes a cash value feature, it is not a substitute for diversified investment strategies.

Misconception 3: “You Only Need Life Insurance If You Have Children”

Life insurance may also be considered for:

- Income replacement

- Business continuity

- Estate obligations

- Shared financial responsibilities

Coverage needs vary by individual circumstances.

Risk Assessment and Personal Evaluation

Before choosing between term and whole life insurance, consider:

- Current financial obligations

- Dependents and family structure

- Long-term financial goals

- Liquidity preferences

- Budget flexibility

- Estate planning considerations

Some individuals choose one type exclusively. Others may combine policies depending on needs.

The key is structured evaluation rather than emotional decision-making.

Renewal and Conversion Options

Many term life policies include features such as:

- Renewal options at the end of the term

- Conversion to permanent insurance without new medical underwriting (within certain periods)

These features can provide flexibility, but terms vary by insurer.

Careful review of policy details is essential before purchase.

How Insurers Price Life Insurance

Premium pricing is influenced by several factors:

- Age

- Health status

- Medical history

- Lifestyle factors

- Coverage amount

- Policy duration

Younger applicants typically qualify for lower premiums. Health conditions may impact eligibility or cost.

Transparent underwriting processes help insurers assess risk accurately.

Long-Term Considerations

Life insurance decisions often involve long time horizons.

It is helpful to:

- Review coverage periodically

- Reassess after major life events

- Update beneficiaries when necessary

- Evaluate financial changes

Major events that may trigger review include:

- Marriage

- Birth of a child

- Home purchase

- Starting a business

- Significant income change

Life insurance is not necessarily a one-time decision.

Regulatory and Consumer Protections

Life insurance in the United States is regulated at the state level.

Regulatory frameworks help ensure:

- Financial stability of insurers

- Transparent policy disclosures

- Consumer protection standards

- Fair underwriting practices

Consumers are encouraged to review policy documents carefully and ask questions before committing to coverage.

How to Approach the Decision

Instead of asking, “Which is better?” a more useful question may be:

“What role should life insurance play in my overall financial strategy?”

Term life focuses on affordable, temporary risk protection.

Whole life emphasizes lifetime coverage with an added financial structure.

Both have defined purposes within structured financial planning.

Final Thoughts

Term life and whole life insurance serve different needs. The decision between them depends on duration requirements, financial goals, and long-term planning preferences.

Term life insurance provides straightforward, time-limited coverage that is often more affordable. Whole life insurance offers permanent protection with a built-in cash value component.

There is no universal answer that fits everyone. The most effective approach is informed evaluation based on individual circumstances.

Life insurance works best when it is understood clearly — not chosen based on marketing claims or assumptions.