Most insurance companies think their biggest challenge is speed.

- How do we sell faster?

- How do we close more deals?

- How do we improve conversion rates?

- How do we scale acquisition?

But in reality, speed is rarely the root problem.

The deeper issue is far more structural:

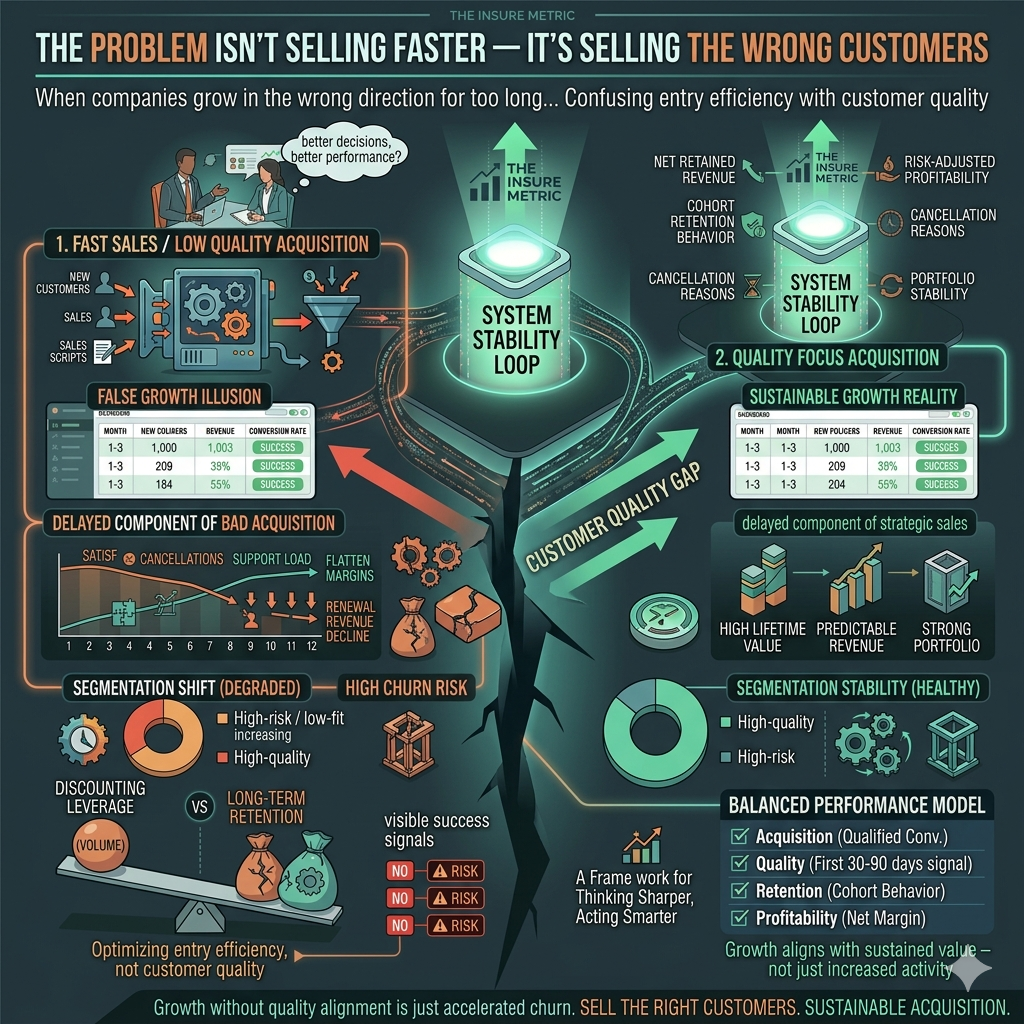

Many insurance businesses are not struggling to sell more—they are struggling to sell to the right customers.

And once you start acquiring the wrong customers at scale, everything else begins to look like a performance problem when it is actually a portfolio problem.

The illusion of “good acquisition performance”

Let’s start with a simple scenario.

An insurance agency reviews its monthly performance:

| Month | New Customers | Revenue | Conversion Rate |

|---|---|---|---|

| 1 | 900 | €380,000 | 17% |

| 2 | 1,100 | €440,000 | 19% |

| 3 | 1,300 | €510,000 | 21% |

Everything looks healthy:

- more customers

- higher revenue

- improving conversion

Leadership interpretation:

“Our acquisition strategy is working.”

But this is only the surface.

Because acquisition tells you nothing about who is being acquired.

The missing variable: customer quality

When insurance companies optimize for volume, they often ignore a critical dimension:

Not all customers contribute equally to long-term value.

Let’s introduce a second layer:

| Customer Type | Risk Level | Retention | Profitability |

|---|---|---|---|

| Type A | Low | High | Strong |

| Type B | Medium | Medium | Stable |

| Type C | High | Low | Weak |

Now let’s see what happens when acquisition accelerates:

| Month | Type A | Type B | Type C |

|---|---|---|---|

| 1 | 60% | 30% | 10% |

| 3 | 40% | 35% | 25% |

Even though total sales increased, the portfolio composition shifted:

- fewer stable customers

- more high-risk customers

- lower long-term predictability

This is where the problem starts.

Why “wrong customers” feel like success at first

The dangerous part is timing.

Bad customer acquisition does not fail immediately.

In fact, in the early months, it often looks better:

- higher conversion rates

- faster sales cycles

- easier onboarding

- stronger short-term revenue

Why?

Because low-quality customers are often:

- easier to convince

- more price-sensitive

- more reactive to discounts

So they convert quickly.

But they also:

- churn faster

- generate more support cost

- produce lower lifetime value

This delay creates a false sense of success.

The hidden cost structure of bad customers

Let’s compare two acquisition strategies:

| Metric | Strategy A (Quality Focus) | Strategy B (Volume Focus) |

|---|---|---|

| Conversion rate | 16% | 22% |

| Average premium | €450 | €380 |

| 12-month retention | 82% | 61% |

| Support cost per client | €12 | €24 |

| Lifetime value | €320 | €210 |

At first glance:

- Strategy B looks better in acquisition metrics

But in reality:

- Strategy A produces more sustainable profit

This is the core misunderstanding:

Conversion rate does not measure customer value. It only measures entry efficiency.

Why insurance systems drift toward bad customers

This drift does not happen randomly.

It is usually the result of structural pressure:

1. Sales targets prioritize volume

Agents are rewarded for:

- number of policies

- monthly revenue

- short-term performance

2. Marketing optimizes for cost per lead

Cheaper leads often mean:

- lower intent

- weaker fit

- higher churn risk

3. Dashboards highlight acquisition, not lifecycle

Most systems emphasize:

- new customers

- not retained value

Together, these incentives push the system toward:

maximizing acquisition efficiency, not customer quality.

The compounding effect of bad acquisition

Once the wrong customers enter the system, effects compound over time:

Month 1–3:

- revenue increases

- conversion improves

- leadership is satisfied

Month 4–8:

- cancellations rise

- support workload increases

- margins start shrinking

Month 9–12:

- churn offsets new sales

- acquisition pressure increases

- pricing becomes more aggressive

Eventually:

the business is no longer growing—it is replacing itself.

Why selling faster makes the problem worse

Speed amplifies existing incentives.

When companies push for faster sales:

- qualification time decreases

- decision quality decreases

- discount usage increases

- customer fit worsens

This creates a paradox:

The faster you sell, the less stable your customer base becomes.

So speed does not solve the problem.

It accelerates it.

The segmentation problem nobody fixes

One of the most important missing capabilities in insurance organizations is proper segmentation.

Many companies segment customers by:

- product type

- price tier

- channel

But very few segment by:

- retention probability

- claims behavior

- lifetime value trajectory

- risk stability

Without this, all customers are treated as equal at acquisition stage.

Which leads to:

identical effort applied to completely different long-term outcomes.

A simple but powerful diagnostic

Ask this question:

If we stopped discounting tomorrow, which customers would still buy from us?

The answer reveals a lot.

Because:

- high-quality customers are less price-sensitive

- low-quality customers depend heavily on incentives

If most of your current acquisition depends on discounts:

you are likely over-acquiring low-quality customers.

The portfolio effect: why it scales silently

Insurance is not a collection of independent sales.

It is a portfolio.

And portfolios have a structural property:

Small changes in acquisition quality create large long-term effects.

For example:

| Year | Portfolio Quality | Profitability |

|---|---|---|

| 1 | Balanced | Stable |

| 2 | Slightly degraded | Slight decline |

| 3 | Highly skewed | Volatile |

| 4 | Unstable | Declining |

This is why problems often appear late.

Not because they are small.

But because they accumulate quietly.

The false solution: “just sell more”

When performance declines, the instinct is usually:

- increase lead volume

- push agents harder

- raise conversion targets

- accelerate acquisition

But this assumes the problem is insufficient volume.

When in many cases:

the problem is insufficient quality control at the point of acquisition.

What better insurance organizations do instead

High-performing insurance companies tend to:

1. Define customer quality early

Before acquisition, not after.

2. Weight acquisition by lifetime value

Not all customers are treated equally in KPIs.

3. Track cohort performance

Not just monthly totals.

4. Penalize high-churn acquisition channels

Even if they are high-converting.

5. Align incentives with retention

Not just acquisition volume.

The mindset shift that changes everything

Weak systems ask:

“How do we sell more?”

Strong systems ask:

“What kind of customers are we scaling?”

Because in insurance:

Growth without quality alignment is just accelerated churn.

Final thought

The real problem in most insurance organizations is not that they cannot sell faster.

It is that they have optimized acquisition without fully understanding what they are acquiring.

And once that happens, every improvement in speed simply increases the rate at which the wrong customers enter the system.

In insurance, success is not defined by how quickly you grow, but by how sustainably your customer base can hold that growth over time.

Selling more is easy.

Selling the right customers—and keeping them—is what actually defines a healthy business.