Most insurance companies don’t fail because they stop growing.

They fail because they grow in the wrong direction for too long.

On the surface, everything looks like progress:

- More leads coming in

- Higher monthly sales

- Better conversion rates

- Increasing activity across the team

But underneath all of that, something quieter is happening.

Customers are leaving faster than they are being replaced.

And the worst part?

It often goes unnoticed until the damage is already structural.

The uncomfortable reality of “healthy growth”

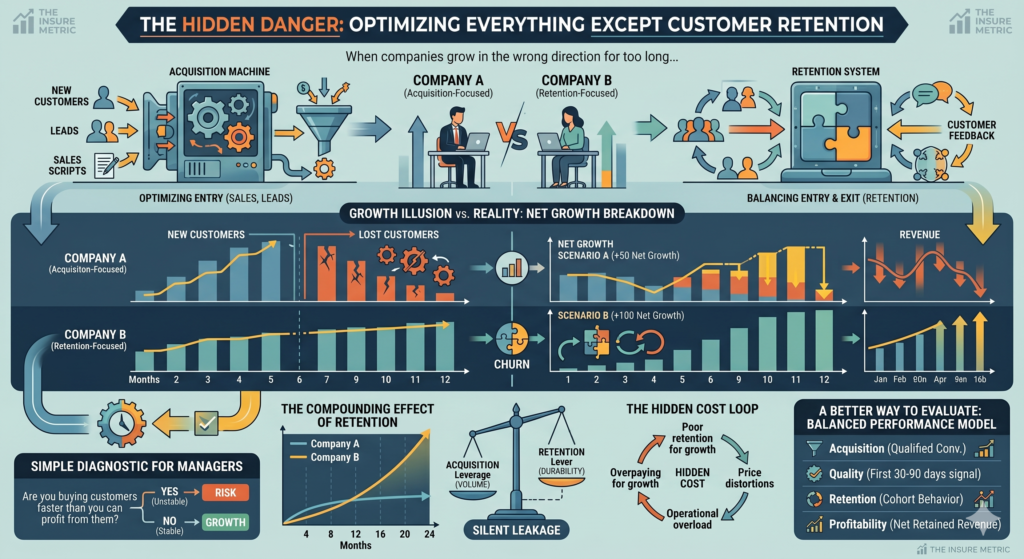

Let’s imagine a simple insurance agency over 12 months.

They are focused on optimization:

- Sales scripts improved

- Lead generation increased

- Conversion funnels optimized

- Response times reduced

Everything that is usually labeled as “growth work”.

Now let’s look at what their performance dashboard shows:

| Month | New Customers | Lost Customers | Net Growth | Revenue Trend |

|---|---|---|---|---|

| 1 | 120 | 60 | +60 | Rising |

| 2 | 130 | 70 | +60 | Rising |

| 3 | 140 | 85 | +55 | Stable |

| 4 | 150 | 100 | +50 | Flat |

| 5 | 160 | 120 | +40 | Slight decline |

| 6 | 170 | 140 | +30 | Declining |

At first glance, this still looks like growth.

New customers are increasing every month.

But there is a hidden curve:

Losses are increasing faster than gains.

This is the early stage of retention failure.

The illusion of success: acquisition dominance

Most insurance dashboards are built around acquisition metrics:

- New policies sold

- Monthly revenue

- Lead conversion rate

- Agent activity levels

These are easy to measure and easy to celebrate.

But they share a critical flaw:

They only measure entry, not exit.

Retention, on the other hand, behaves differently:

- It is delayed

- It is cumulative

- It is less visible in short-term reports

So organizations naturally underinvest in it.

Not because they don’t care.

But because it doesn’t shout as loudly as sales numbers do.

A simple breakdown of what really drives growth

Let’s simplify business growth in insurance:

Real growth = New customers − Lost customers

Now compare two scenarios:

| Scenario | New Customers | Lost Customers | Net Growth |

|---|---|---|---|

| A | 200 | 150 | +50 |

| B | 150 | 50 | +100 |

Scenario A looks busier.

More activity. More pressure. More “success signals”.

Scenario B looks quieter.

But it is actually growing twice as fast.

This is where many teams get misled:

Activity is not the same as progress.

Why retention is harder to notice (but more important)

Retention is not a single metric. It is a system.

It is influenced by:

- Customer expectations

- Claims experience

- Pricing perception

- Communication quality

- Policy fit over time

And unlike acquisition, it doesn’t show immediate feedback.

A bad acquisition strategy fails this month.

A bad retention strategy fails in 6–18 months.

That delay creates a dangerous gap:

You keep optimizing while the system is already weakening.

The “silent leakage” problem

Retention issues rarely appear as dramatic events.

They appear as leakage.

Let’s visualize it:

| Month | Portfolio Size | Monthly Loss Rate | Revenue Stability |

|---|---|---|---|

| 1 | 1,000 | 5% | Stable |

| 3 | 1,200 | 7% | Slight volatility |

| 6 | 1,400 | 10% | Unstable |

| 9 | 1,600 | 13% | Declining |

| 12 | 1,800 | 16% | Contracting base effect |

Even though the portfolio is growing, the quality of that growth is deteriorating.

This is what makes retention problems so dangerous:

They hide inside growth for a long time.

The hidden cost of ignoring retention

When retention is not actively managed, three things happen:

1. You overpay for growth

You need more acquisition just to stay flat.

2. You distort pricing

Discounting increases to replace lost customers.

3. You overload operations

More churn = more support = higher cost per client

Over time, this creates a loop:

- Customers leave

- You spend more to replace them

- Margins shrink

- You push harder on acquisition

- Quality drops further

A real example of metric imbalance

Consider this simplified insurance performance snapshot:

| Metric | Value |

|---|---|

| Monthly new customers | 500 |

| Monthly churn | 450 |

| Net growth | +50 |

| Average acquisition cost | €120 |

| Average lifetime value | €300 |

At first glance:

- The business is growing

- Revenue is increasing

But let’s add perspective:

| Hidden Metric | Value |

|---|---|

| Cost per retained customer | €240 |

| Effective profit per client | Very low |

| Break-even retention threshold | 18 months |

| Actual average retention | 10 months |

This means:

The company is buying customers faster than it can profit from them.

Why teams ignore retention (even when they know it matters)

There are three main reasons:

1. It is harder to measure in real time

Acquisition is immediate. Retention is delayed.

2. It doesn’t feel actionable

Teams feel they can “control sales” more than retention.

3. Incentives are misaligned

Most bonuses are still tied to acquisition metrics.

So even when retention is understood conceptually, it loses priority in execution.

The behavioral trap inside sales teams

When retention is not part of performance evaluation:

- Sales teams prioritize easy-to-close customers

- Discounts increase to accelerate decisions

- Long-term fit is deprioritized

- Quality filtering disappears

This leads to a subtle shift:

The system starts optimizing for conversion speed, not customer durability.

What good retention-focused companies do differently

Companies that avoid this trap usually:

1. Separate revenue types

- New revenue vs retained revenue

2. Track cohort behavior

- Not just monthly totals

3. Measure customer quality early

- First 30–90 days behavior signals

4. Include retention in incentives

- Bonuses tied to long-term value, not just acquisition

A simple mental model shift

Instead of thinking:

“How do we sell more this month?”

Retention-focused organizations ask:

“How do we ensure the customers we acquired 6 months ago are still profitable today?”

This shifts the entire system:

- From short-term output

- To long-term stability

The compounding effect of retention

Retention has a nonlinear impact on growth.

Improving retention by:

- 5% might not feel significant in month 1

- but over 12–24 months, it compounds massively

Because every retained customer:

- reduces acquisition pressure

- increases predictable revenue

- lowers cost per client

In insurance, retention is not just a metric.

It is a multiplier.

Final thought

Most insurance businesses don’t struggle because they fail to grow.

They struggle because they optimize every visible part of the system except the one that determines whether growth actually lasts.

You can improve sales, conversion, and efficiency—and still lose the business slowly if retention is ignored.

Real performance is not defined by how many customers you bring in.

It is defined by how many you can keep long enough for value to actually materialize.